TSMC: Undisruptable And Undervalued!

It's hard to find an undisruptable company trading at a discount, yet TSMC is offering that opportunity now. Given the outlook, the stock can easily double in the next 5 years!

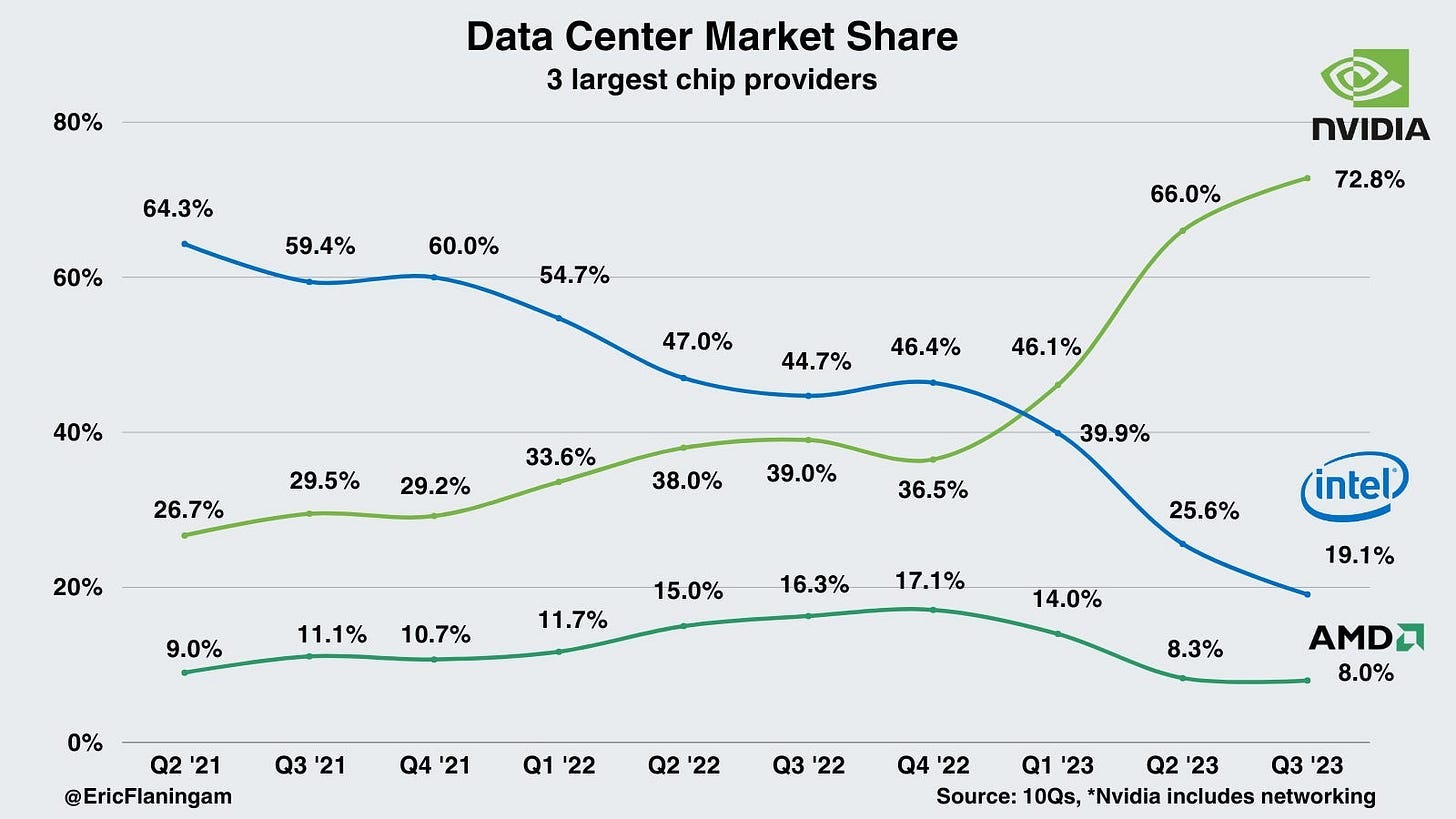

Who will make the best chips 5 years from now? I don’t know. I think nobody knows.

Just look at the chart below and you’ll see why:

In July 2021, Intel had 64% market share in all data center chips while Nvidia had 26% and AMD had 8%.

Two years later, Nvidia’s share jumped to over 66% while Intel plummeted to 25%.

Nobody could see this coming.

What’ll happen…