🚨 Trade Alert 17: Trimming One Position, Opening Two New Positions

Trimming one position to buy another stock in the same sector, and also buying a fast-growing European small-cap.

When you look at the market crashes of the past, the popular narrative is that they were sudden and unexpected. This narrative is spread because it’s useful for the market actors. It helps them claim no-fault.

The reality is different.

Warning signs emerge before all the great market collapses, but people just choose to ignore them. We just choose to believe it’s not yet time for the music to stop.

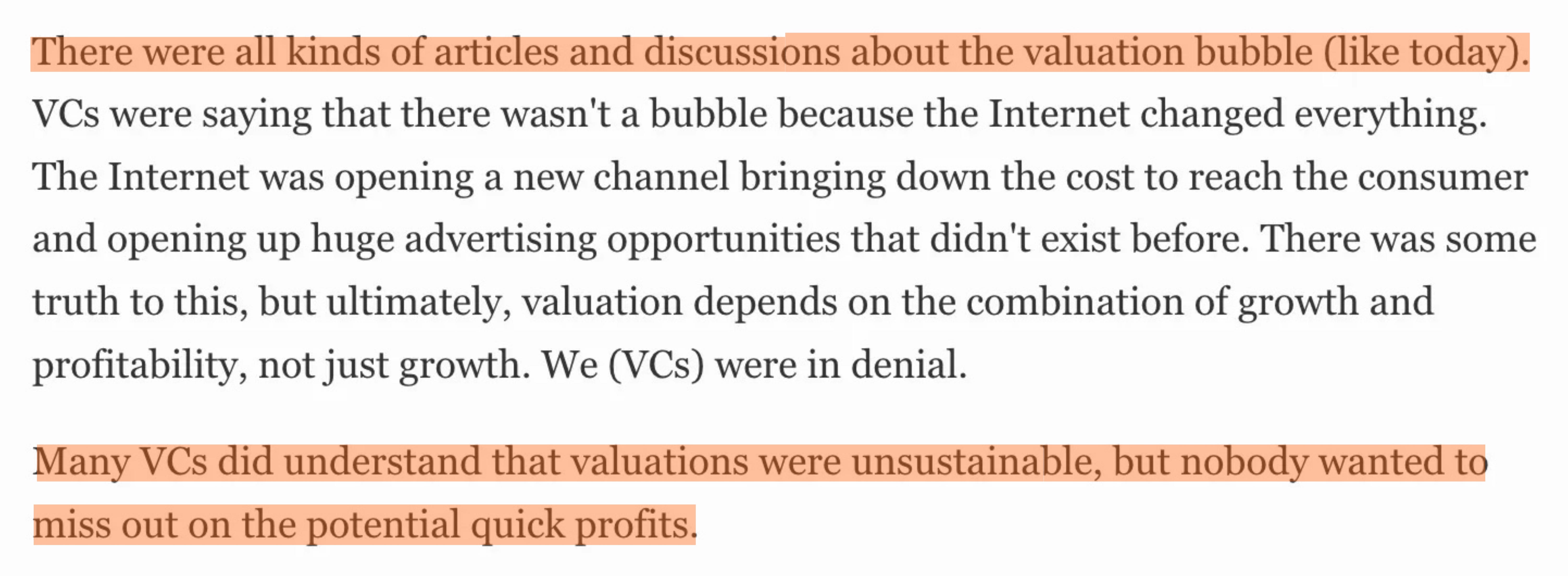

Paul Cohn is a partner in Agility Equity Partners, and he was a VC in Silicon Valley during the dotcom boom. This is what he wrote about the environment in the Valley at the time:

As you see, unlike the popular narrative, signs were there, and nobody was blind. Everybody understood what was going on, but just chose to ignore the signs to pursue quick profits.

Similar warning signs are flashing today.

It’s forgotten that what matters is growth + profitability, not just growth.

Valuations have already hit unsustainable levels.

People ignore valuations to chase quick profits.

It’s arguably even worse today as the market has never been more expensive, not in the dotcom bubble, not in the 1929 bubble, never.

Yet, one thing history has taught us is that high valuations themselves are not a sufficient condition for a correction. Something needs to stop the money flow. As Ray Dalio says, “something needs to prick the bubble.”

Back in 2000, these valuations were sustained by VC money flowing to dotcom startups, which then went public, so the public market capital flowed back into VCs, allowing them to repeat this until public market capital stopped flowing as those IPOs started to go bankrupt and the Fed raised interest rates.

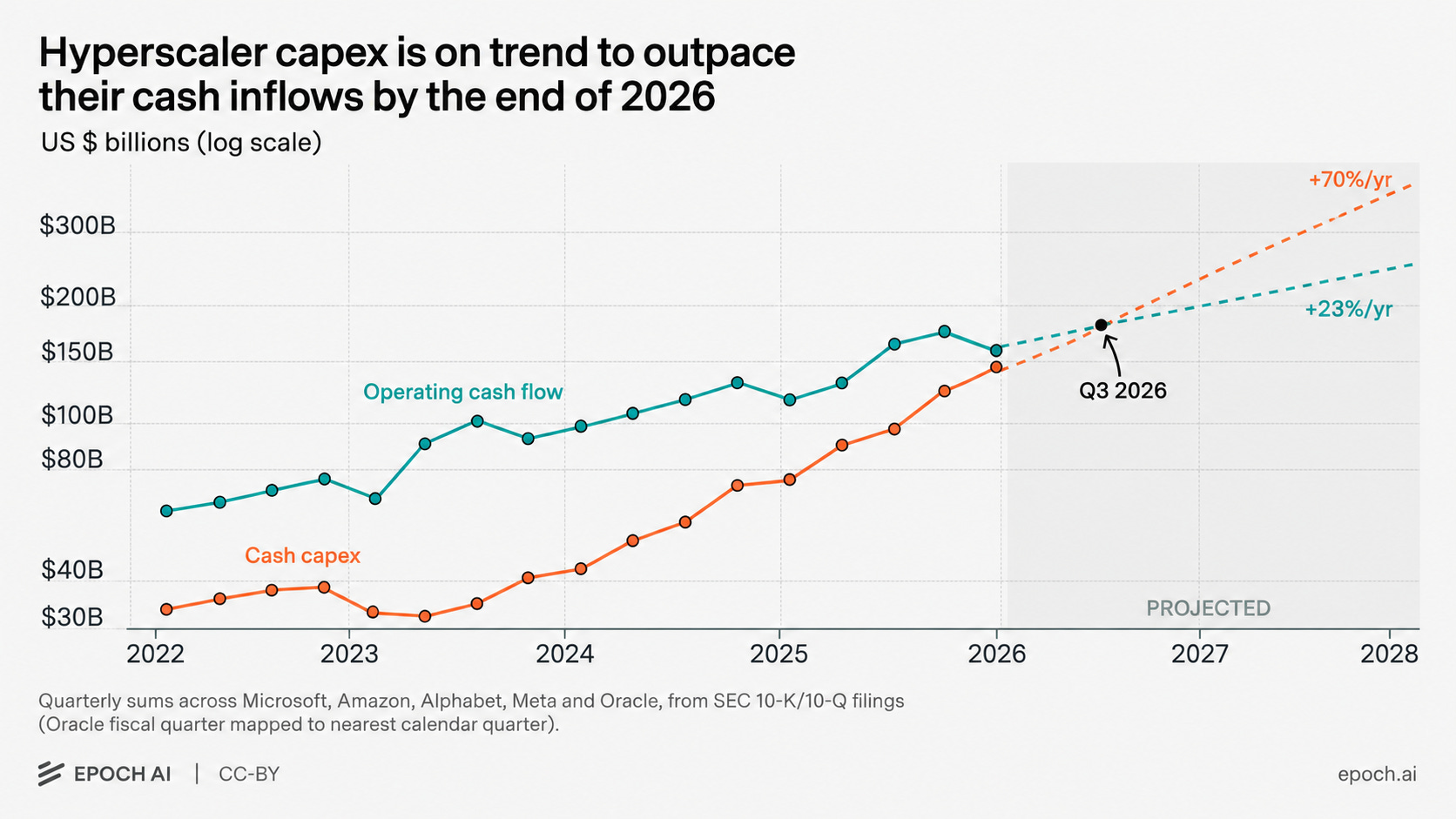

Today, high valuations are sustained by hyperscaler cash flows.

They are the ones funding the AI buildout. When the earnings go up across the AI value chain, it’s because hyperscalers are buying. The problem is, we are nearing the limits of their funding ability.

Capex guidance for this year is already well above 2025 operating cash flows for all of them. And cash flows are not catching up anytime soon, as projections by Epoch AI show:

This doesn’t mean capex numbers will suddenly collapse, but we likely won’t see aggressive upward capex revisions from now on, unlike what we have seen over the last three years.

What does this mean? Should we cut all the AI/semiconductor/hardware exposure?

Of course, no. Let me articulate once again where I stand:

I am a huge AI bull. As I explained in one of my previous articles, I think AI is a general-purpose technology that will pervade almost every electronics and digital processes we are using today. Over time, that will lead to a productivity boom, which will further increase demand for AI. Thus, I think computing demand will secularly grow to infinity, just like we saw with electricity demand and the internet bandwidth.

But this doesn’t mean all this buildout should happen fast over the next 3-4 years. We’ll likely see some stalls and reacceleration once the ROI catches up. This is why I believe we should remain bullish on AI while not ignoring valuations.

The straightforward implication of the potential slowdown in AI buildout due to draining hyperscaler capex is this: If you are buying stocks valued at 25-30x sales based on the assumption of upward capex revisions, you may get disappointed. Capex numbers may not grow fast enough to create the assumed sales boom for those stocks.

In this environment, what makes more sense is prioritizing the companies with contracted revenue, as these are already included in the current capex projections.

This is what underlies one of the transactions I’ll be making today. I’ll be opening a position in an AI enabler trading at a substantial discount to its contracted revenue.

Second, we should also be aware of the systematic risk we are facing today.

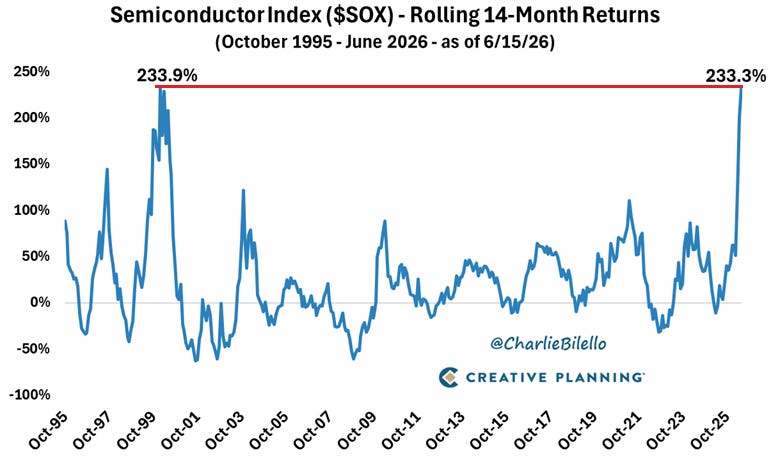

As I said above, the market is currently the most overvalued as it’s ever been. What makes this worse is that this overvaluation has mostly been led by one sector—semiconductors.

We also have a lot of money in this sector as we bought AMD in early 2025 and exited with a 5x return just two weeks ago. However, we shouldn’t be blinded by the amazing performance of the sector. It’s not normal. In the history of the market, the semiconductor index delivered over 230% in the rolling 14 months only twice:

This is alarming because capex growth hitting a wall may create a domino effect. It could lead to a correction in valuations across semis and hardware, which will trigger a market-wide correction as 49% of the S&P 500 market cap is made up by AI-enablers.

Given this systemic risk, it’s prudent to diversify away from the US whenever an attractive opportunity presents itself. Indeed, one of our best performers this year is Tasmea, which is an Australian consolidator of the skilled service businesses:

I have recently found a similar opportunity in the European market, and I’ll be buying my first shares today, as it’s already attractive in and of itself and allows us to diversify away from the increasing systemic risk of the US market.

To summarize, I’ll be making three transactions today:

I’ll trim a position in an overvalued AI enabler and shift it to an undervalued AI enabler with contracted revenue.

Open a position in a fast-growing European small-cap.

This way, we’ll keep our exposure to the AI trade without exposing ourselves to the risks related to a potential slowdown in capex growth, and also diversify away from the systemic risk of the US market while not sacrificing performance.

I’ll explain the trades below and add the link to the portfolio spreadsheet at the end of the write-up. I’ll be updating it after I execute the trades.

So, let’s get started.

Here are the exact trades I am making:

This is one of the most obvious valuation disconnects I currently see in the market.