The Mega-Cap Opportunity: Meta & Microsoft!

The market unduly discounts Meta and Microsoft. Time to buy.

Investing is all about buying exceptional businesses at attractive prices.

At least, this is the type of investing we practice here, and it’s worked exceptionally for us so far.

The definition clearly states the two critical elements—an attractive price and an exceptional business.

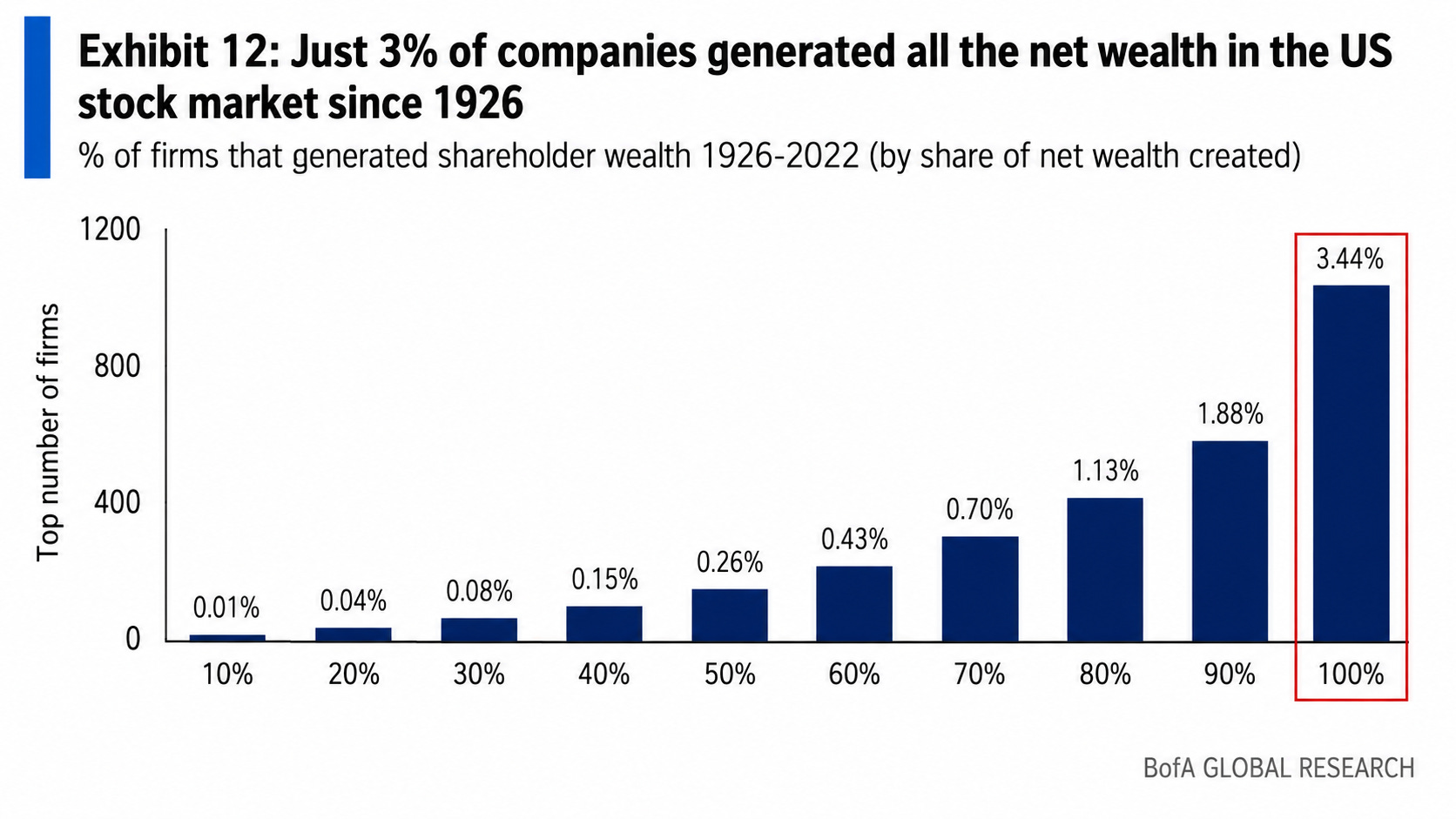

The importance of the “exceptional” part can’t be overstated. For reference, 3% of the firms generated all the wealth in the US stock market since 1926. Buying and holding exceptional companies is the key.

The problem is that it’s hard to practice this simple strategy as “undervalued” and “exceptional” are two properties that rarely come together. This is by its nature.

Exceptional companies are rare; thus, they tend to be very well known. Especially those that are above a certain size. Since they are well known, their stocks usually trade at a significant premiums to the market.

This changes rarely.

Looking at the market history, there are three cases where exceptional businesses can be categorically undervalued:

General crash in the market.

Industry-specific recession.

Emergence of a new revolutionary technology.

The first two are self-explanatory, but the third is more nuanced.

Since the Industrial Revolution, firms at the frontiers of technology tended to be bigger than others, as higher technology often means higher value-add. Thus, at times of technological changes, the market questions how incumbents will fare.

Will they be the winners, or losers?

This often leads to fluctuations in their valuations, and more importantly, makes their valuations increasingly driven by sentiment. The more the market believes they’ll be winners, the more optimistically they are valued; if the market believes the opposite, their valuations get depressed.

This is exactly what we are going through right now.

The so-called “Magnificent 7”, as a group, is now trading at its lowest relative valuation premium to the rest of the index:

When you see a situation like this, by default, it should be where you look to see if there is an opportunity here before embarking on a treasure hunt.

The reason is simple—exceptional companies tend to stay exceptional.

Thus, when you find those stocks at a discount, by default, they are more likely to be buying opportunities than not. Naturally, you are closer to making money on them than you would be buying lesser-known stocks, as they expose you to obscure risks.

This doesn’t mean you shouldn’t look elsewhere. It just means that when something obvious comes up, you should first determine whether it’s really an opportunity. If yes, you have to prioritize them rather than setting sail for lesser-known waters.

This is what we’ll discuss in this write-up—does the declining mega-cap premium really create a buying opportunity in mega-caps?

To understand whether there is an opportunity or not, we have to:

Establish whether some of them are really discounted, and not just cheap compared to their own historical metrics.

If yes, we have to understand the reasons and see if they are justified.

This is what we’ll do.

Do any of the mega-caps trade at a discount?

To understand whether the declining mega-cap premium has actually led to a real discount in some of those names, we need to understand the pricing mechanism of the market.

At any given time, any stock’s valuation is made up of two parts:

Value of the current earnings.

Present value of the future growth expectations.

Michael Mauboussin and Dan Callahan recently published a paper titled “Opportunities and Expectations” explaining how current earnings and growth expectations shape the current value of stocks. If you haven’t read it, I highly recommend you read it as soon as possible. We’ll draw on this paper here.

The core idea is simple.

We can estimate the steady-state value of a company’s current operating earnings by assuming that those earnings continue indefinitely with no growth. Under that assumption, the earnings stream can be valued as a perpetuity by capitalizing them using their cost of capital.

Why?

A business is an economic asset that generates cash flows for its capital providers, including both lenders and shareholders. Those cash flows should therefore be discounted at the minimum return required by all providers of capital, the company’s weighted average cost of capital, or WACC.

Thus, we can estimate the economic value of $1 of sustainable net operating profit after tax, or NOPAT, received every year indefinitely by dividing $1 by the WACC.

If we assume that the WACC is 10%, the present value of $1 of annual NOPAT received in perpetuity is $10, as (1)/(10%)=10.

This represents the steady-state enterprise value generated by each $1 of sustainable NOPAT. To determine the portion of that value attributable to shareholders, we then subtract net debt.

The result is the estimated equity value of the company’s current earnings power. If the equity is priced at a premium to this value, it means the market is assigning some additional value to future growth.

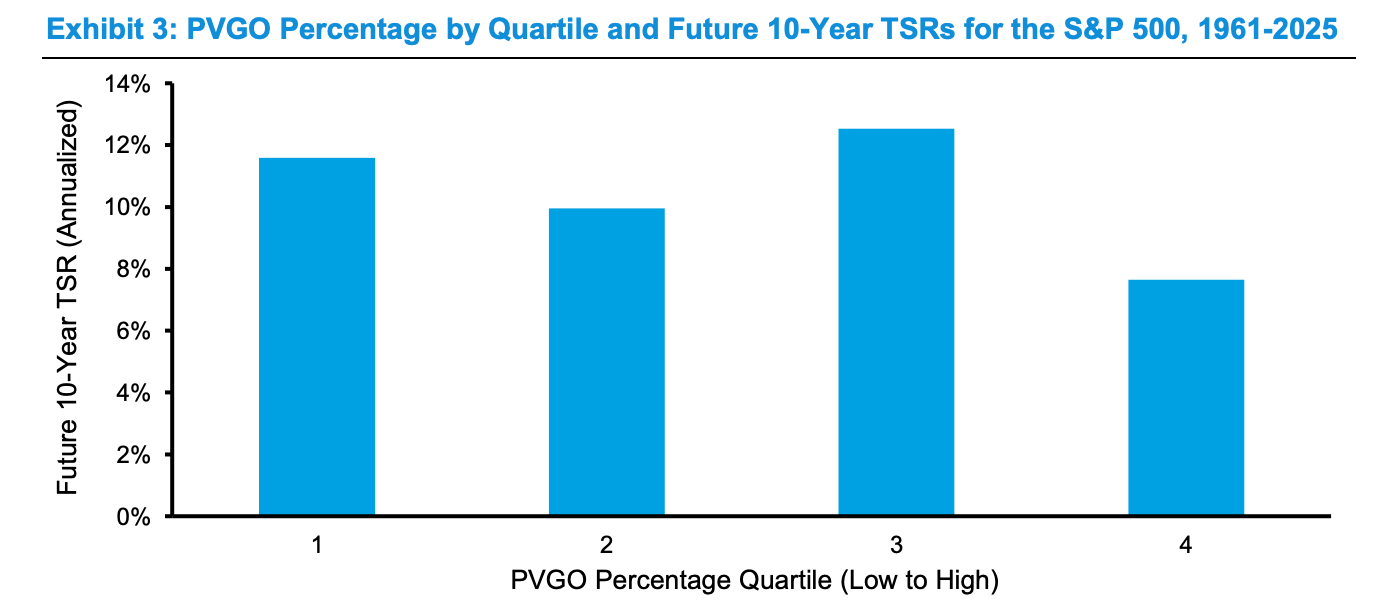

Important conclusion that follows from this is that a higher share of future growth in the current market implies higher expectations. Naturally, when expectations are high, it’s harder to deliver for companies. Mauboussin and Callahan clearly establish this in their paper.

Their research found that while the connection between the share of present value of growth opportunities (PVGO) in stock price and future performance is largely sporadic, the returns in the highest quartile are substantially lower. This means the inverse correlation strongly manifests itself at the extremes.

This is consistent with the general market behavior.

At 19x P/E, you can’t say much about the future direction of the market. It can go to 22x or 16x. Both are equally likely. However, at 25x, the mid-term direction of the market has always been downward.

According to JPM Research, every time the market traded around 23x earnings, annualized returns for the next 10 years have always been between -2 and 2%. No exceptions.

So, it’s extremely helpful to see how much of the current market cap is from future growth opportunities to understand where the expectations are for the mega-caps we are looking at today.

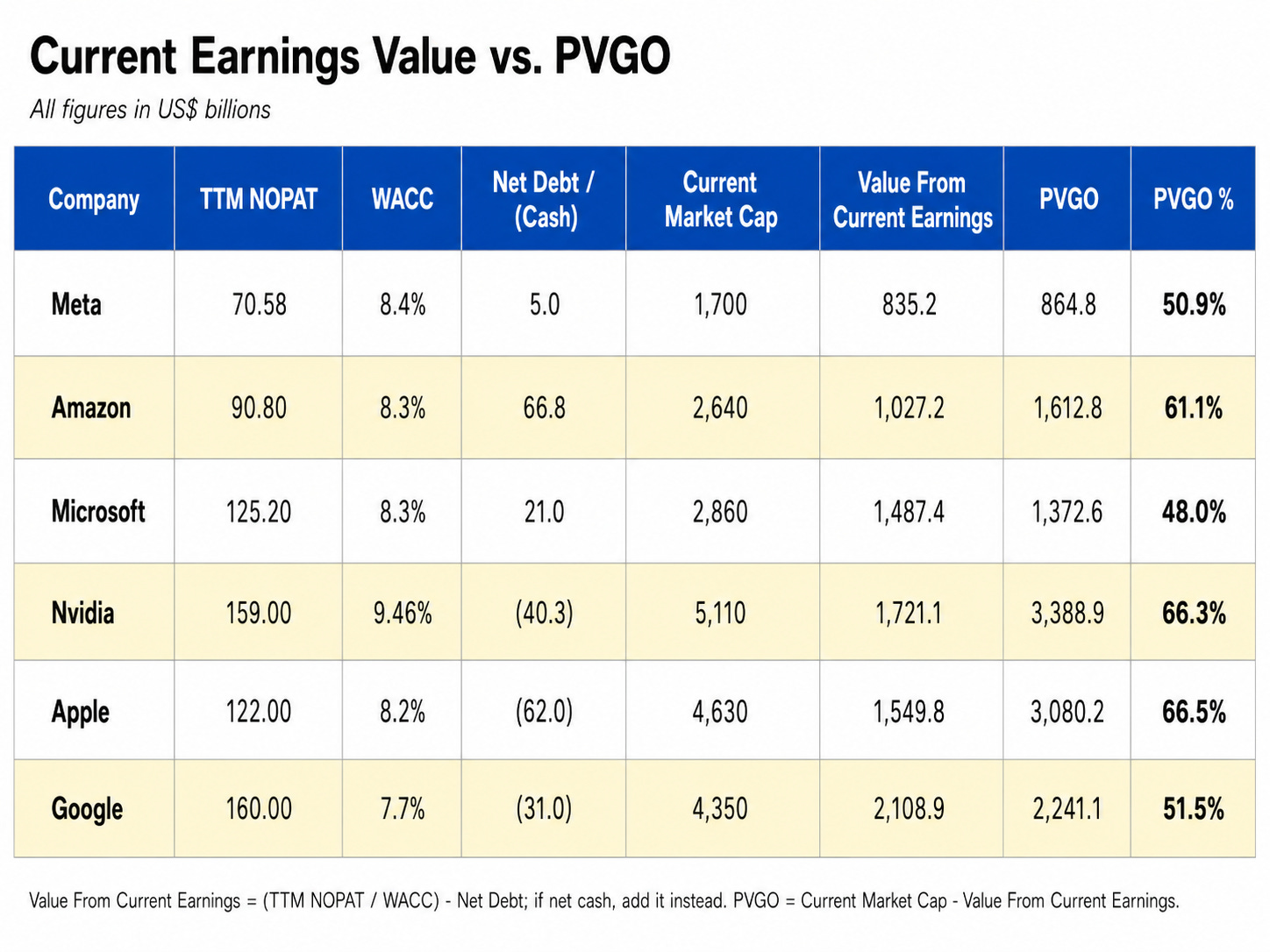

I have taken their TTM NOPATS, capitalized by cost of capital, subtracted debt, and calculated the ratio of value from current earnings and forward growth to market caps. I excluded Tesla from this practice as it’s obviously overvalued.

As you see, nearly half of the current market values of Meta, Google, and Microsoft come from future growth opportunities, while this is way higher for the others.

Now, these figures don’t mean much by themselves. Even if we look at historical figures for these businesses and compare them to where they stand today, it’s hardly indicative, as they are at much larger sizes right now. So, we have to compare it to some benchmark.

That benchmark is, of course, the S&P 500.

However, as the S&P 500 is an index directly based on market caps of the components, we don’t need to use NOPAT and subtract debt. We can just use TTM earnings and the current cost of equity, which is estimated as the equity risk premium + risk-free rate.

TTM earnings for the S&P 500 are around $293. Equity risk premium is around 4.23% as per Aswath Damodaran, and the 10-year Treasury yield is 4.55%, giving us an average index cost of equity of 8.78%.

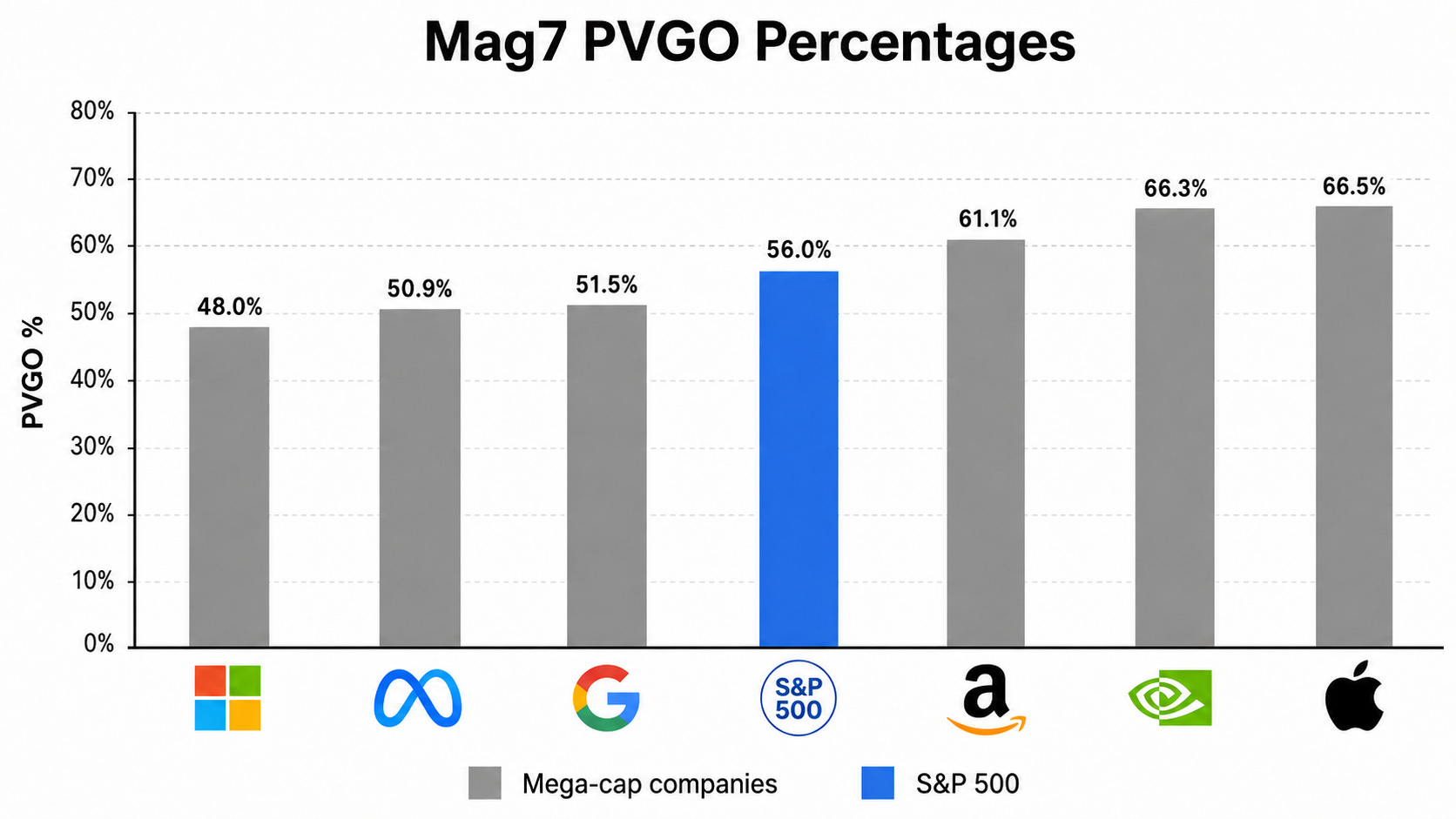

So, capitalizing earnings with cost of equity gives us 3,337. Given that S&P is currently at 7,575 points, this means only 44% of the current market cap of the S&P 500 is from current earnings power of the index components. According to Mauboussin, the historical average has been 65%.

This means the market is extremely optimistic about the future. Though remember that the future returns of the index when PVGO on the 4th quartile have been substantially lower.

However, what’s even more interesting than this extreme confidence in the future doesn’t reflect on three companies—Google, Meta, and Microsoft, as they are the only ones for which a lesser portion of current value is PVGO compared to the S&P 500.

At first look, it’s easy to make sense for a few names.

Apple is not a capex spender, and it’s now valued like a consumer staple, so it’s natural that the market thinks most value lies in the future. Nvidia rides the capex wave, so it’s understandable as well. Amazon is a big capex spender, but its core e-commerce business is valued like a durable consumer staple, like Walmart, so it offsets the capex-heavy tech business.

Among the names whose future potential is discounted relative to the market, Google is easy to make sense of, as its search business is seriously threatened. Personally, I don’t remember the last time I did a deep Google search on a topic as I would back in the 2010s.

Some people could make the same argument for Microsoft software as well, but it’s obviously not correct. We are ditching search gradually, but I haven’t met any single person or a business entity that has ditched Microsoft software.

So, we are clearly looking at a special situation with Microsoft and Meta.

These are known as way above average quality assets with above average growth expectations. For reference, Meta is expected to grow its top line by 20% annually over the next three years while Microsoft is expected to average 17% annual growth in this period. In the meantime, the S&P 500 is expected to deliver 8.5% annual sales growth.

Despite their superior prospects, Meta and Microsoft are actually and substantially discounted relative to the market.

Thus, the question is whether this discount is justified or not.

Let’s dig.

Why are Meta and Microsoft discounted?

There are three common reasons we can observe for the discount they get. We have to look at each one of them and explore whether they are justified.

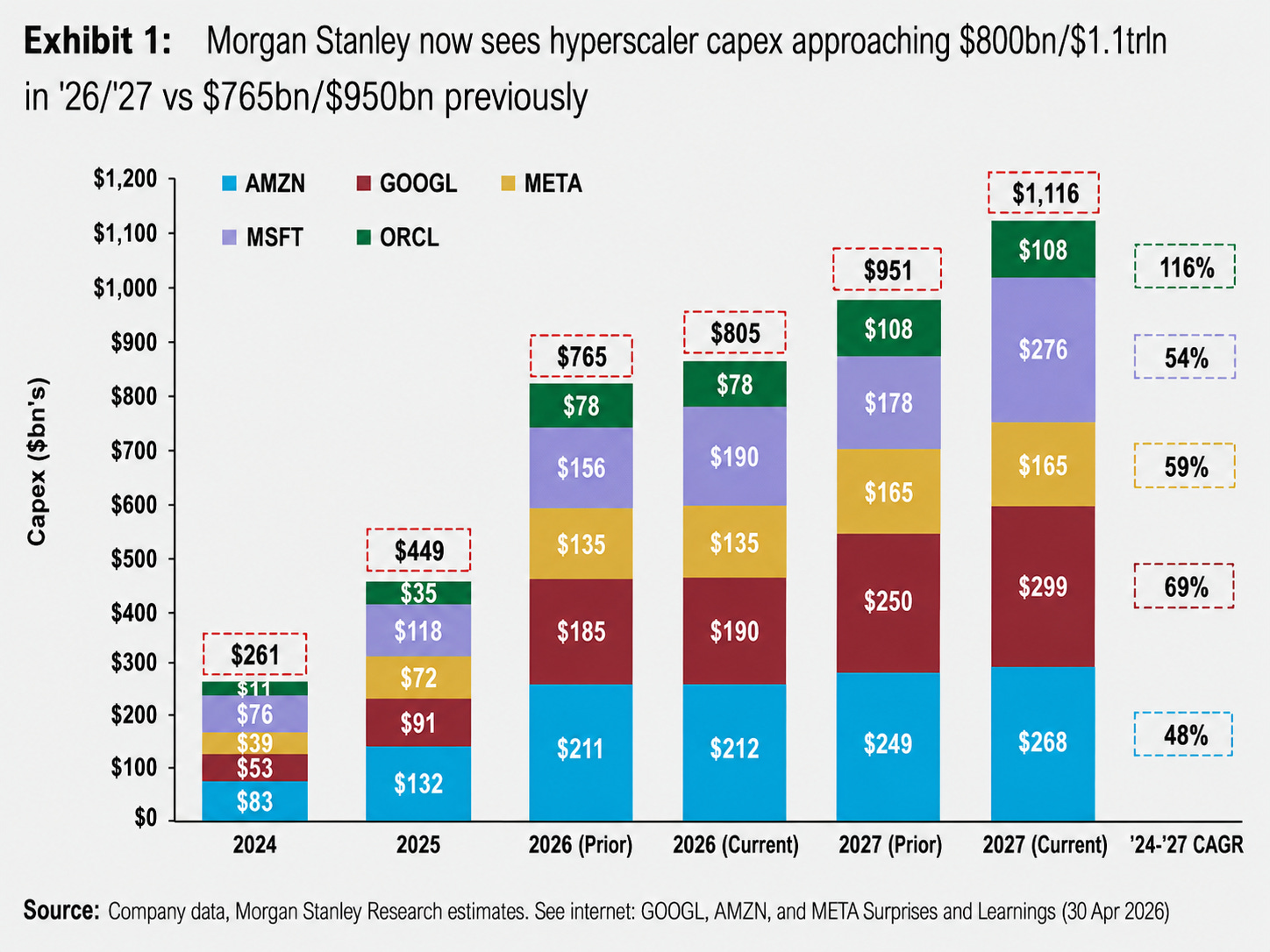

1️⃣ Concerns About ROI on AI Capex

The common problem for Meta and Microsoft is that they are both big capex spenders. These companies’ combined capex is projected to reach $325 billion this year, while total capex for hyperscalers will surpass $800 billion:

Now, if this is the case, why are Google and Amazon more optimistically valued than Meta and Microsoft? What makes them different?

The difference is having a cutting-edge AI lab.

Google is competitive in the AI model race, and the market thinks it’ll be one of the winners. This translates to higher confidence to generate positive ROI on AI capex.

Microsoft has a strong AI unit, but they aren’t very competitive in the model race right now, while Meta’s Superintelligence Labs is just getting traction.

But Amazon also isn’t competitive in the race, right?

Yes, and it’s punished for that. When you look at the headline numbers, you may think Amazon is optimistically priced, but most of the premium is due to the durability attributed to its retail business. The market sees it as a Walmart-like consumer staples business.

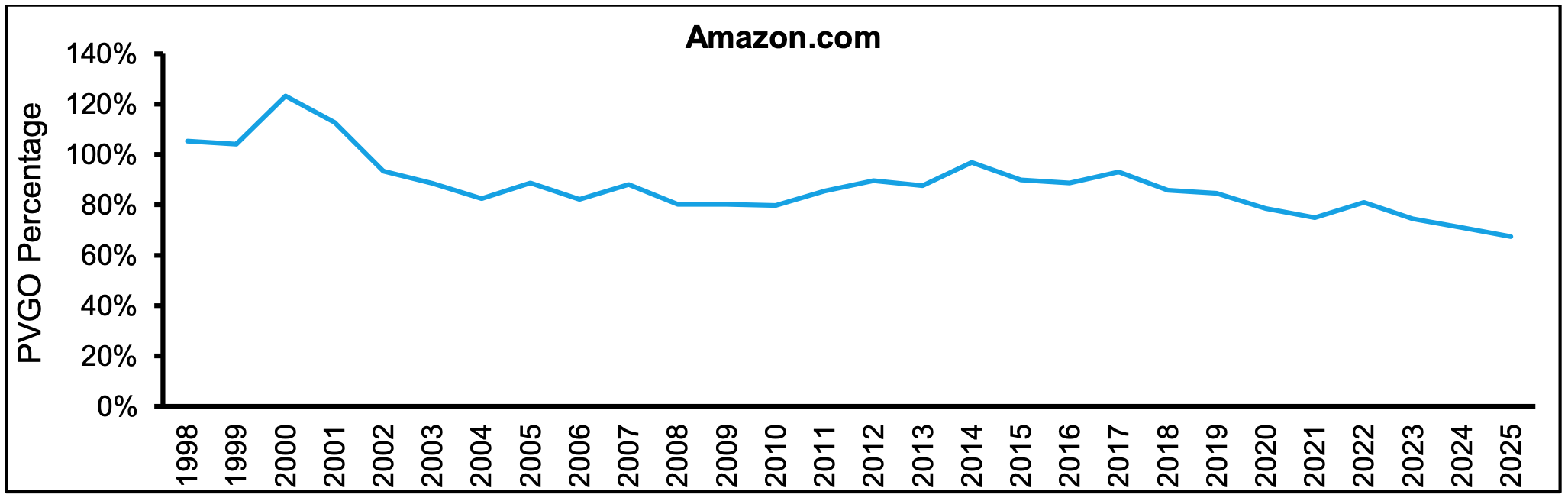

Michael Mauboussin’s historical PVGO numbers for Amazon validate this. Despite seemingly high PVGO relative to Meta and Microsoft, it’s at its lowest level since it became public. This illustrates that the market doesn’t attach much premium to Amazon’s AI infrastructure business.

So, the main problem is ROI concerns rather than purely high capex. If you have a competitive AI lab, the market thinks you have a better shot at generating ROI; if not the market doesn’t think path to ROI is easy by just selling compute.

Is this really the case? I don’t think so.

Economics of the recent deals are illustrative. SpaceX reportedly generates ROI between 70%-120% from its deals with Anthropic and Google.

Yes, SpaceX compute business is designed to address acute demand. It’s called the short-term & large-scale market for compute where prices are 3x-4x the long-term contract prices of neo-clouds.

However, if this is the case, hyperscalers should also be generating above 20% ROI on the compute they sell. This has been hard to track due to the lag between capex outflows and revenues, but we can see we are in the right direction.

According to the latest Bloomberg figures, global AI revenues excluding China have reached 1.2x of D&A.

Assuming 8% cost of capital, 30% operating margins, and 5 years of depreciation, hyperscaler capex turns positive at roughly 1.7x revenue/D&A. Note that this is a very conservative assumption and the actual value is likely lower as D&A is longer than 5 years in practice. Nvidia A100 chips released in 2020 are still being used.

This means that hyperscalers can generate significant ROI in their AI infrastructure businesses even without making cutting-edge AI models.

Microsoft is currently not pushing hard on the model race; however, Meta has been pursuing this market relentlessly, and they have released pretty satisfactory image and language models lately. The market reacted positively.

If this strategy of Meta holds, its compute business will largely operate in short-term/large-scale market since bulk of the compute will be used internally, and it’ll only monetize what it doesn’t “currently” need. In this market, prices and ROI are way higher.

However, even if its attempts to be a competitive player in the models market fail and it has to monetize bulk of its compute through a cloud business more like that of Microsoft’s and Amazon’s, there is a clear path to ROI as illustrated by the figures above. Bloomberg itself also saw the numbers as a clear path to ROI:

In short, both Microsoft and Meta have a path to ROI on AI capex even without competitive model businesses. This is validated by both ROI numbers on SpaceX deals and the general ramp of the global AI revenue ahead of D&A.

2️⃣ Possible Capacity Overbuild

This is the second reason the market is skeptical about huge AI capex.

In a stabilized market, ROI is a function of capacity, so they are closely connected. But the main worry here is not an imbalancing oversupply in an otherwise stabilized market, but a massive capacity overbuild where most of the capacity won’t be utilized.

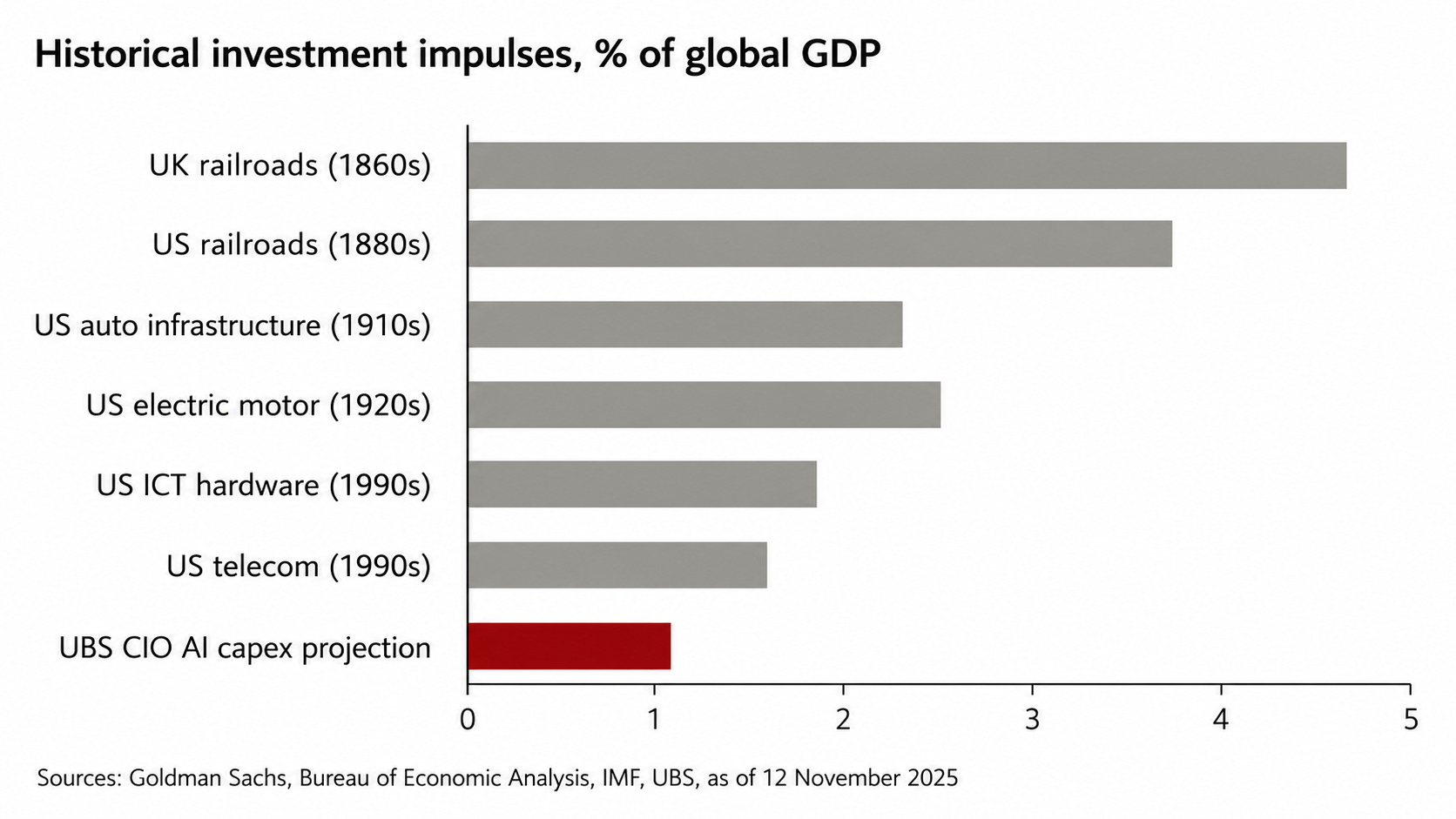

Those who are afraid of this frequently share the chart below:

As you see, we are just a couple of years into this investment supercycle, but AI capex is already around 1.5% of the US GDP. Given that annual AI capex is projected to at least double by 2030, we’ll likely see this number peak around 2.5% of GDP, which is largely in line with the previous investment booms.

When people see this, the logical conclusion that follows is that there will be a big bust, as all the major investment cycles were followed by a bust.

This is correct, but I think there is also a different perspective here.

Look at all these booms, and you’ll see that, despite the busts, we always ended up with less than we needed over the long-term.

Think about railroads. Despite the railroad bust of the 1870s, we currently need much more railroads than we have. And it’s harder to build railroads now, so the industry will likely stay supply constrained for a very long time.

Look at the telecom boom. Despite the bust, we are still expanding the infrastructure today as the internet bandwidth we need keeps growing.

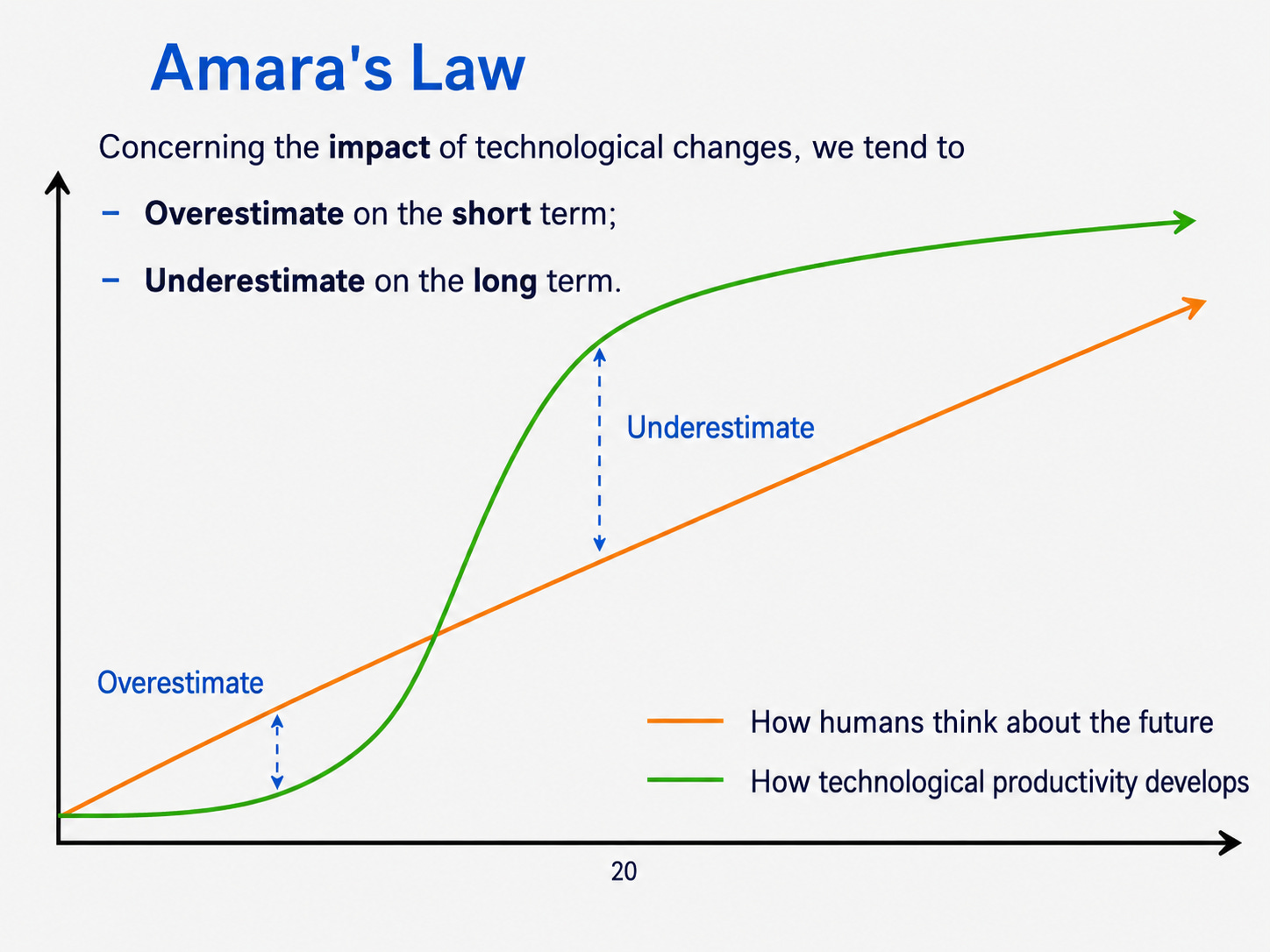

This is basic Amara’s Law, which suggests that we overestimate the potential of a new technology in the short-term and underestimate it in the long-term.

As a result, we tend to overestimate the investment needed in the short-term, but underestimate it in the long-term. Continuing investments in telecoms, railroads, and hardware illustrate this.

So, why does this happen?

The answer is simple—diffusion.

Up until now, diffusion of new technologies has been slower than we can mobilize the investment.

Again, think about computers and phones. It took a long time to do the required investments, but also there was an adoption curve involved as these were the technologies that people didn’t have a clue about before their productization. This extended the learning curve, and diffusion has been slower.

As there were no global networks, news and know-how about new technologies took time to spread in the US, let alone the globe. And when they did, it again took time for other countries to take steps and adopt the tech.

Public data networks emerged in the late 1970s, commercial internet service providers emerged in the US in 1989, yet most of the world didn’t connect to the internet before 1993.

This lag between investments and diffusion led to busts as the owners of the investments couldn’t extract the benefit they expected from their spending.

This changed with the internet. As it’s a global technology now, every new technology provided on the web diffuses at an unprecedented pace.

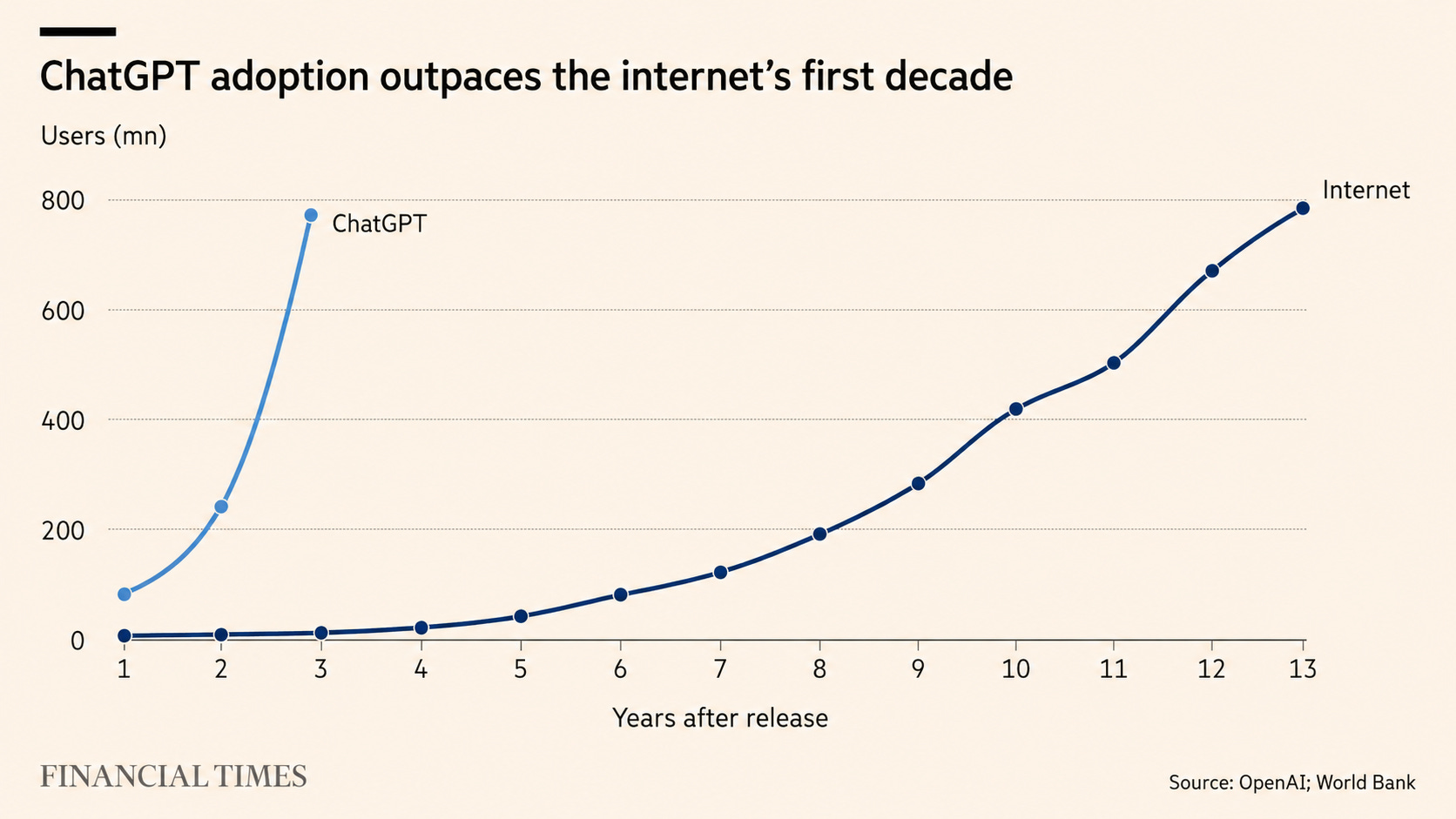

This is exactly what we have seen with AI.

ChatGPT has a 3x to 4x faster diffusion rate compared to the internet itself:

The result of this faster diffusion is that the lag between capacity investment and utilization shortens. This increases the foreseeability for the capex spenders.

In the early 1800s, a railroad investor was acting with a lot of assumptions about 5-10 years ahead. Today, an AI capex spender sees how fast the incremental capacity it brings online is consumed in days, not months. Thus, they have a far better sense of short- and mid-term demand.

This is why we may not get the short/mid-term overcapacity that we saw with the previous cycles. The fact that we have a market for short-term & large-scale demand proves this.

Therefore, I don’t expect a post-investment bust at a scale because of this speed of diffusion.

What’s more interesting, the argument could be this: As the capacity ramps and technology diffuses, AI infrastructure will be like utility and can thus have utility margins even without a major capacity oversupply.

Let’s discuss this.

3️⃣ Margin Collapse in AI Infrastructure Business

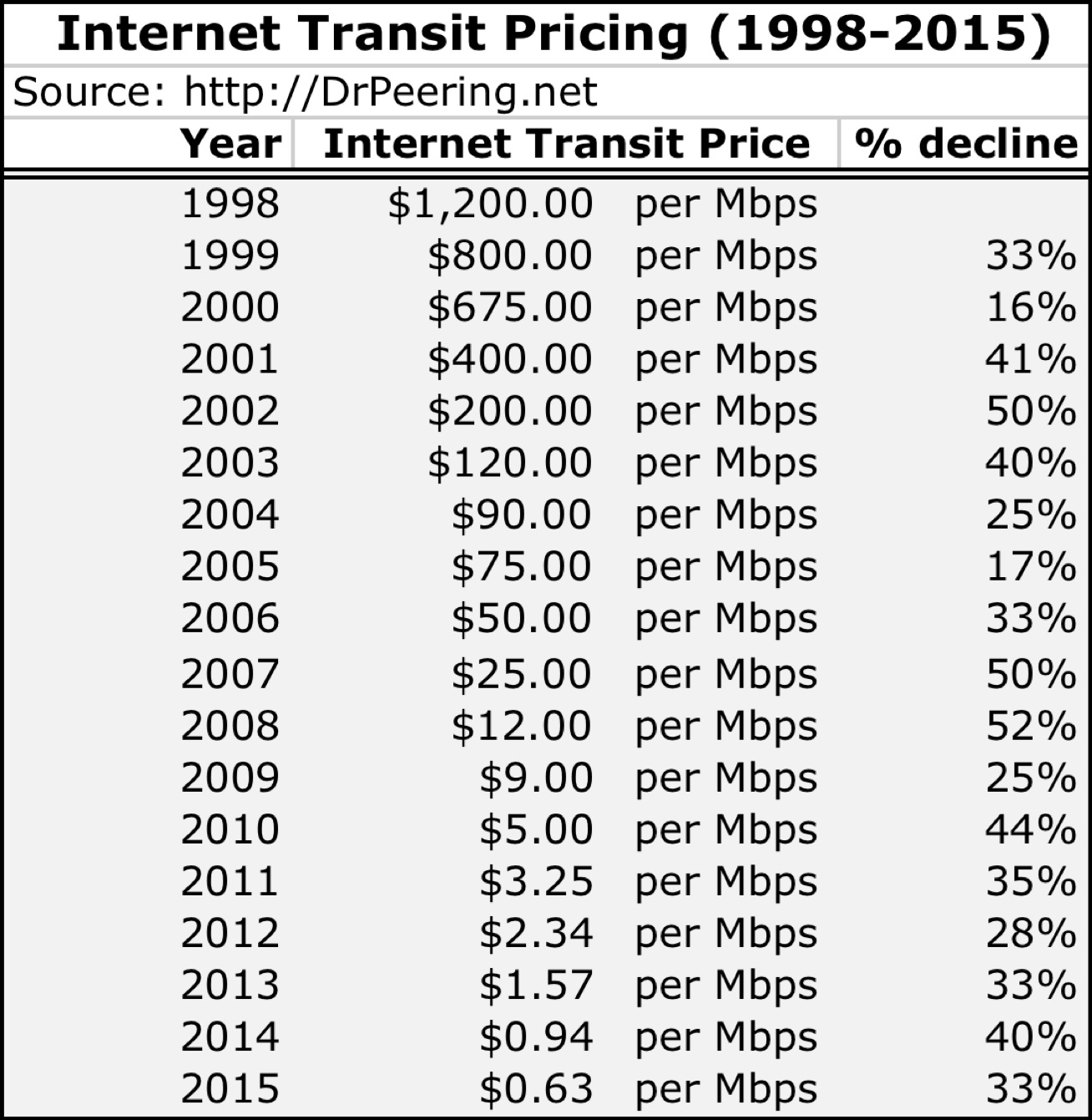

The most relevant comparison here is probably the change in wholesale internet prices. As infrastructure expanded, the prices collapsed:

It’s even cheaper now, with some sources reporting as low as $0.08 per Mbps in key American and European cities with fully developed infrastructure.

This is basically utility-level pricing.

As a result of this, major telecom companies haven’t become mega-caps like Microsoft and Meta. They are basically like utilities.

The argument here is as follows, and I used to think this way as well: If AI will change the world, it has to diffuse like the internet and electricity first, and to reach that level, prices should collapse so margins of the companies in this business will be utility-like.

However, I changed my mind on this as I thought further on the subject.

Two important points led to this change.

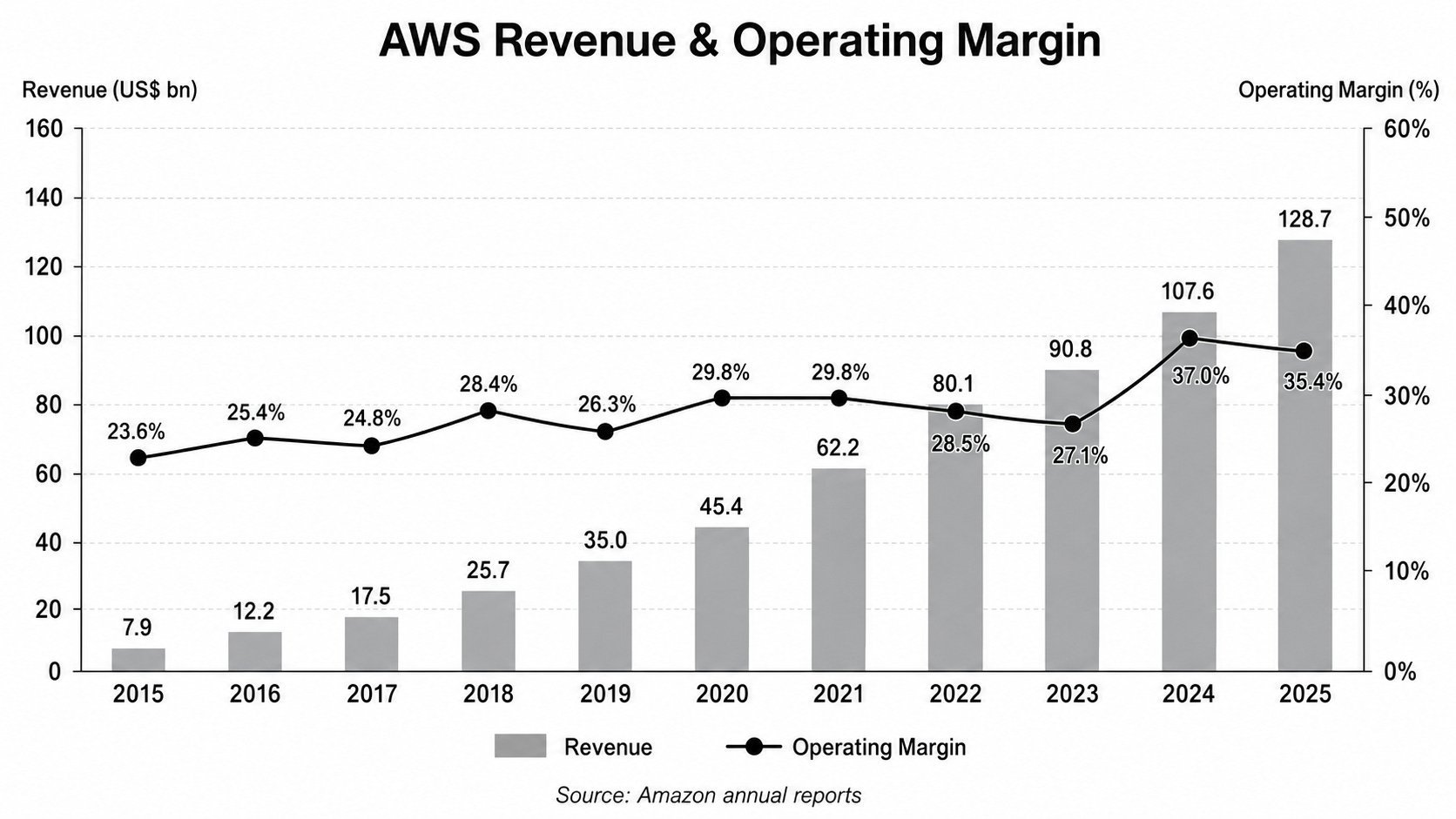

First, look at the margins in the traditional cloud business.

Utility margins argument could have been made for the traditional cloud business, but Amazon unveiled +20% operating margins in 2015, and that climbed to over 35% since then. Instead of shrinking margins, we got expanding margins.

Why? Because of the difference in asset lives.

Telecom infrastructure, for instance, is composed of long-lived assets. Useful lives of the telecom assets are above 30 years. However, they are amortized in shorter periods. This leads to collapsing prices as price competition intensifies post-D&A period.

Server chips, on the other hand, have a depreciation period of 5 years on average, and can produce returns above cost for around 7 years. So, when you are operating with assets that you need to replace in 5-7 years, and every new generation of chips costs more than the older ones, you can’t expect utility-level pricing.

Second reason why margins may not collapse is that we are looking at an oligopolistic market where cost of ownership declines for incumbents with every new generation of hardware.

Due to the insane capital expenditures needed, the entry barriers are already high. Potential entrants can’t cover the cost of new equipment at scale. Incumbents, however, can do this. As a result, their cost of ownership declines over time; however, they don’t feel that much pricing pressure due to the oligopolistic market structure.

There are only a handful of companies that can provide compute at large scale and the highest level of reliability. Plus, most customers don’t switch for a few pennies of discount as it exposes them to a business risk. Customers also seldom cut prices on their existing models, so they are fine with paying the ask anyway.

This is a bit like retail.

Everybody can open a mini-market, but it’s almost impossible to reach the scale of Walmart and Costco.

The difference is that a bottle of water bought from a mini-market and Costco has the same value to the customer. In the AI compute business, 1 MW has 0 value for the customers that matter. But if you have +10 GW, they are literally dependent on you, allowing you to have satisfactory margins.

Because of shorter replacement cycles and an oligopolistic market with dropping total cost of ownership, I think the margins will stay at satisfactory levels and possibly even at higher levels than the traditional cloud.

🏁 Conclusion

Whenever you see exceptional companies at a discount, buy them. Don’t be distracted by thinking about what else you can add to your portfolio. It exposes you to higher risks and dilutes returns.

Currently, we have so much discussion about the mega-cap discount, as their huge premiums over the index have eroded lately. However, when we analyze it in more detail, we see that only three companies are really trading at a relative discount to the market—Google, Meta, and Microsoft.

Among them, I eliminate Google because of the search business. That leaves us with Meta and Microsoft.

Both of these businesses have a lower share of their current market cap come from future growth than the broader index. Yet, both have higher mid- and long-term growth expectations than the market average.

So, here the discount stems from the lower likelihood the market attributes to that growth, and possibly lower value of growth due to lower ROIC.

I don’t agree with this for the reasons I explained above.

If you buy the arguments, this means the market attaches lower future potential to two companies of which there are no questions about their superior quality.

This is why I see a buying opportunity in Microsoft and Meta, especially Microsoft, as Meta was bumped up by ~20% last week.

I have owned Meta for a long time but entered Microsoft last week. I’ll be looking to grow my Microsoft position going ahead and consider opportunistic purchases in Meta if it drops again due to sentiment change.

That’s all friends!

Thanks for reading Capitalist-Letters!

Please share your thoughts in the comments below.

👋🏽👋🏽See you in the next issue!