The Inevitable AI Bubble

AI bubble is inevitable, losing money is not.

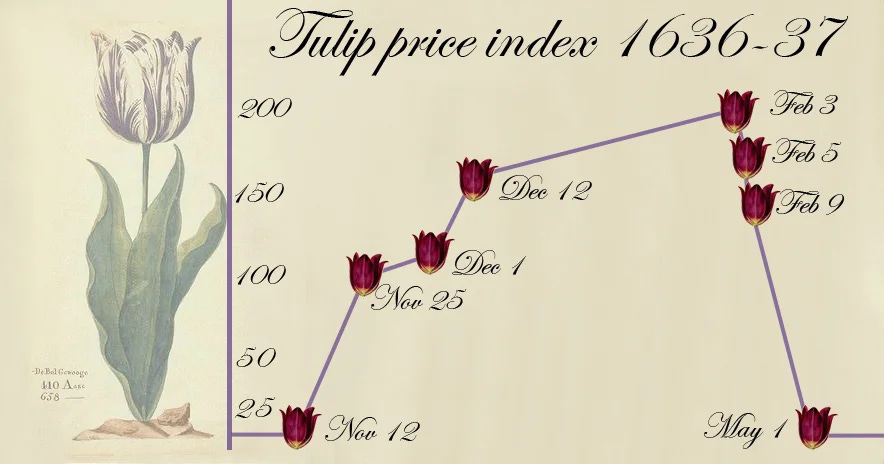

In the 1600s, there was the Tulip Bubble.

People were paying the equivalent of a house price to buy a bunch of Tulips.

Anybody who hears this today will ask the same question—how f.cking stupid were they?

But, if you went back in time and asked those people, they would say: No, no, the demand is off the roof.

You go fast forward 330 years, to the late 1990…