SOFI Stock: Buy For Your Financial Freedom

SOFI Stock: Buy For Your Financial Freedom

We don't know whether the business can help people achieve financial freedom, though, its stock is well positioned to do this. This is an opportunity you don't want to miss!

“Helping people achieve financial freedom” has long been Sofi’s motto. They created a whole business around this. This is a bold mission.

There is no way, as an investor, I can predict how successful it’s going to be in this mission, though, I know investing in SOFI 0.00%↑ can help you do it!

I will explain how and why investing in SOFI is a big opportunity now and how it can help you make so much money.

I warn you, you will want to scrape money off your bank account and put in this opportunity!

🔑🔑Key Takeaways:

🎯 SOFi makes money in three ways: Lending, selling its tech stack and other providing traditional financial services.

🎯 SOFi provides all the financial services an individual can need through its platform and in a social setting, creating internal and external network effects.

🎯 All-in one platform and network effects provide SOFi with a strong moat. Even if it is possible to replicate the business model, it will take years to match the network effect.

🎯 The business is growing fast and it’s on strong financial settings. There is no existential threat to the business.

🎯 The company trades at attractive valuation. If you account for 2026 guidance, you are now paying only 11 times of earnings that management expects to keep growing at 20% CAGR even beyond 2026. If you attach a PEG ratio of 1, you are looking at a $14 stock in 2026.

👇🏼👇🏼If you are interested in the stock, let’s dive deeper👇🏼👇🏼

🎬Before we start…

I think all the readers deserve what they are going to get even before they read.

My Approach: In 1983, Warren Buffett walked into the biggest furniture store in Nebraska, and asked everybody for the owner. People directed him to Rose Blumkin, a Russian immigrant with a heavy accent. She was a tough woman, but she was famous for her honesty and for always offering the best price to her customers. Among workers and customers, she was known as “Mrs. B”.

She asked Buffett: “What do you want?” Buffett said “I want to buy your business.”

She said “I will sell it to you for $60 million and not a penny less.” Buffett said “deal.”

This was it. This is how Warren Buffett bought one of the most successful furniture stores in the entire US.

He says it takes 10 minutes to spot an exceptional opportunity. If you can’t understand what the business does, whether it’s a good deal in 10 minutes, you have to walk away. This is my approach.

If you can’t understand and explain what the business does and why it’s a great opportunity, you have to say bye bye.

🧱Structure

1️⃣ Understanding the business.

2️⃣ Does it have a “moat” i.e durable competitive advantage?

3️⃣ Fundamental Analysis

4️⃣ Valuation

5️⃣ Conclusion

💩No bullshit.

📊No complex graphs and charts to convince you this is smart.

You are going to find whether Sofi is an investment worthy company that has a durable competitive advantage and whether it is attractively priced.

Let’s get started!

🤔 What Does SOFI Do?

Few people understand what SOFI is.

Some see it as a tech company, some think it’s a bank, some people think its not much different than RobinHood… There is so much confusion. Actually, it’s not that complicated.

In 2011, SoFi began with a simple yet revolutionary idea: to provide more affordable loan refinancing options for students. It was simply bringing students together with individual investors who were willing to refinance their student loans. In simple terms it was skipping banks and connecting borrowers directly with lenders.

As the business grew, they created a digital platform where this peer-to-peer interaction could take place, making it easier, smoother and scalable. From there, the business scaled quickly. From there, the business grew quickly, now offering personal loans, home loans, investment platforms, and even insurance.

To better serve the lenders and borrowers, assess risks, and automate the transactions they upgraded their tech infrastructure by acquiring Galileo, a financial services API and payments platform, and then they moved to traditional banking by acquiring a bank charter to offer debit and credit card services. Finally, they also started to offer their tech infrastructure to other financial institutions to automate their loan origination and risk assessment processes.

In short SOFI makes money in three ways:

by lending.

by selling its tech infrastructure.

by traditional banking i.e earning interest on deposits.

It offers these services by positioning itself a partner in people’s journey to financial freedom. They see their customers as “members” and offer them all the financial services they need in one platform which has enhanced capabilities for financial education and audience building, allowing them to create a tightly knit community on the platform.

In short, SOFi is a fintech company that has a bank charter and makes money by lending, selling its tech services and by traditional banking. They provide all these services in one platform which has tools to facilitate network effects.

🏰 Does It Have a Moat?

As a lender, SOFi doesn’t have a moat. There are many lenders.

As a tech service provider, Sofi doesn’t have a moat. There are many providers.

As a bank, SOFi doesn’t have a moat. There are many banks.

As an investing platform, SOFi doesn’t have a moat, there are many online brokers.

As a social app, SOFi doesn’t have a moat. It offers just a few social features.

Do you see where this is going? SOFi doesn’t have a moat in any of these services, but SOFi is all of these services. This is SOFi’s moat.

The question is simple: Can you replicate what SOFi has achieved by investing a few billion dollars? It is very unlikely.

It’s not about the services anymore, it’s about the culture, ecosystem, habits. Those who bank with SOFi love it and there are rapidly growing network effects. Even if you match every service that SOFi provides, it will still take years to acquire a customer base like SOFi and replicate the network effect.

📈Fundamental Analysis

💰Performance

At the first look, SOFi’s diversified business structure may make it look hard to evaluate its performance. After all, it’s making money in three different ways which make it hard to evaluate the performance.

No need to worry. It’s not that complicated.

SOFi makes money in three ways and thus we have to look at what’s the key performance metric in each of these ways.

Lending: You borrow money and you lend it. You pay interest on the amount you borrow, you receive an interest on the amount you lend. Difference between interest income and interest expense is the lender’s net interest income. You want this to be positive and growing.

Tech Stack: It’s simple. revenue. You want the number of customers using your tech stack and overall revenue in this segment to grow.

Financial Services: These services are primarily provided by SOFi Bank. These services include SOFi Money, Credit Card and SOFi investment services. In this segment critical metrics are number of new accounts, and amount of new deposits as these two lead to overall revenue growth in this segment.

Let’s look each of them:

➡️ Lending

SOFi’s net interest income reached $262 million, up from $183 million from the previous quarter, increasing 43% from the last quarter.

For the full year 2023, net interest income reached $960 million, marking 81% increase from the previous year.

SOFi’s lending segment shows mouth watering growth both on quarterly and yearly basis.

➡️ Tech Stack

The Technology Platform segment achieved a record net revenue of $96.9 million in Q4 2023 and $352.3 million for the full year, marking a 13% and 12% increase from the comparable prior year periods and an 8% sequential growth.

What is better for the tech stack revenue is that its contribution to profit for Q4 2023 reached $30.6 million, reaching $94.8 million for the full year, indicating an 81% and 24% increase from the comparable prior year periods.

The growth for the tech business is impressive, indicating SOFi’s strong position as the fintech service provider.

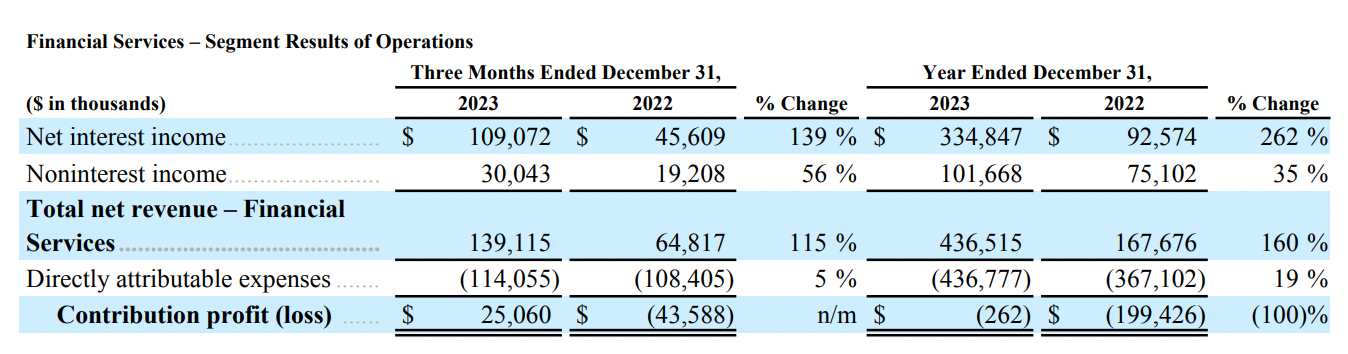

➡️ Financial Services

It added 600,000 accounts and $2.9 billion in deposits. Both amazing numbers.

Growth in accounts and deposit base drove the strong revenue growth for this segment. Overall financial services revenue grew 115% on a quarterly basis and 160% for the full year.

Long story short, SOFi is writing an amazing growth story and consistently delivers strong earnings performance. Passing this phase of the test.

🫀Financial Health

Understanding SOFi’s business is easy, but evaluating the financial health is not.

This is simply because of the fact that it has just delivered its first profitable quarter (Q4 2023) and yet to see a profitable full year. Moreover, its tangible book value is also less than its debt. Though, I don’t think these are huge problems for SOFi.

It has $5.3 billion debt and $3.1 billion in cash. It’s $2.1 billion short but it has positive interest income and all the remaining services are also profitable and growing.

It also has a strong equity basis of $5.2 billion versus $5.3 billion of debt.

However, you shouldn’t forget that the equity base is not the single best metric to measure financial health of the company because no matter how much equity base the company has, it should only reach the equity base to pay debt in case of a bankruptcy. In all other situations, it should be able to service its debt from its cash-flow. SOFi has adequate ability to do this.

Also below will decrease SOFi’s cost of capital and increase its margins in lending:

Deposits increasing on average 20% YoY.

It’s using less warehouse capacity to lend: It’s using about $3.3 billion of its $9 billion in warehouse capacity vs. $4 billion Q/Q.

Loans held for sale are decreasing fast. In the last quarter only, they decreased around $6 billion.

All these factors will positively contribute to SOFi’s financial health and strengthen its already strong ability to service its debt from its cash-flow.

🔢 Valuation

As Aswath Damodaran says, for small companies that are yet to have a full profitable year, valuation is all about the story.

As value oriented, reasonable investors, we don’t normally invest in companies without earning. However, SOFi has delivered its first profitable quarter, this doesn’t just mean it’s making money now, it’s a proof of concept. SOFi proved that it is executing what it has promised, allowing us to play the scenario and value the company.

For 2024, the company expects a full year EPS of $0.08 which means that the company is now trading around 90-100 PE.

However…

For the period beyond 2024 and until 2026, the company expects 20-25% compound annual revenue growth. This is expected to drive between $0.55 and $0.80 in GAAP earnings per share in 2026.

If we stay moderate and say that the company will deliver $0.70 in earnings, we find that the current price is just 11 times of 2026 earnings. It’s quite normal by now. However, the management forecasts sustained 20% growth beyond 2026. Now this is interesting. If you buy this scenario this means you are paying 11 times of 2026 earnings for a company that will be growing 20% beyond 2026. This gives it a PEG ratio of 0.55 which I find I find irresistibly attractive. Plus, also remember that this management has a record of underpromise and over-delivery.

🏁Conclusion

I love SOFi.

It’s one of my largest positions.

I understand the company, I know it has a moat, I know its financial health is intact and I know it’s growing fast.

🚨🚨Valuation is also attractive. Give it a PEG ratio of 1 and you are looking at a $14 stock in 2026.🚨🚨

I am extremely optimistic about the future of the company and I can see no reason why I shouldn’t be!

People got the convertible note offering so wrong. Great article man...as always!