PayPal: A Cannibal In Making

Everything is going at the right direction for PayPal, except for the stock price.

Multi-baggers—this is the name of the game if you want to make some worthwhile money in the market.

If you have a multi-bagger in the portfolio, it makes up for many losing positions; if you have two multi-baggers in the portfolio, you hardly lose money even if the rest of your portfolio is red.

This is how our portfolio has been outperforming the market in the last three years.

We have been generally successful in our picks, but we have had some losers, too. What made the difference is that the several picks we made a few years before have become multi-baggers, driving the portfolio to a 50% gain in the last twelve months.

So, the question is simple—how to find multi-baggers?

Once you ask this question, you start hearing many rules of thumb:

It must be a disruptor.

It should be diversified.

It should be founder-led.

It should be a family business.

These are all cliches modeled after the multi-baggers we have seen in the last decades. They don’t make multi-baggers; they are yardsticks to measure the likelihood of one simple thing: Long-term earnings growth at an above-average rate.

This is what makes a multi-bagger.

Disruptors may experience a sudden rise in earnings, shrinking a few years of growth into a short time. Diversified businesses tend to create synergies and benefit from economies of scale and scope, driving long-term growth; founder and family-led businesses thrive because alignment results in better decisions that create long-term value, etc..

We are all fixated on finding such businesses because it clearly works.

Amazon, Google, Microsoft, Apple, Walmart, and Costco are the ultimate multi-baggers of the last 5 decades, and they are still growing earnings faster than the market.

Stocks like Sofi, RobinHood, Cava, Hims & Hers have become multi-baggers in the last few years because they have grown earnings so much, so fast.

The problem is that everybody is now looking for the next fast-growing stock, but the opportunities have dried up as the market is at all-time highs.

Here is the thing—fast and long growth isn’t the only way to become a multi-bagger.

Companies with stable cash flows, solid market position, and not poised to be disrupted can also become multi-baggers by consistently buying back shares.

Mohnish Pabrai calls them “uber cannibals.”

It’s simple, the business doesn’t need to deliver real growth to create value for shareholders, it’s enough if it can earn pretty much the same inflation-adjusted rate for a long time.

Imagine a business is trading at $1 billion, which is 10 times its free-cash-flow. It generates the same cash flow for 10 years, piling up the cash.

Assuming the same multiple, the market cap will have doubled by the end of the 10th year, as the enterprise value (EV) will stay flat at $1 billion, and cash will add $1 billion more. The stock will double, too, naturally.

Now, what if the business used the cash for buybacks?

Assume 100 million shares outstanding, giving us an initial price of $10. The business uses 80% of its free cash flow every year, $80 million, to buy back shares.

Keeping the multiple constant, here is how the stock price would change:

It more than doubles in the same period.

Here is the caveat—most businesses don’t have this level of stable cash flow for a long time.

Most of them get disrupted, decline, their profits are competed away, or they need to reinvest more to stay in the game. However, there are some businesses that stay strong in their market, but their growth opportunities are very limited.

These are the candidates to become uber cannibals. NVR is the textbook example:

NVR is a homebuilder that doesn’t have the opportunity to grow vertically unless it ventures out of its core business. Yet, the stock returned 236 times in the last 30 years as it bought back over 82% of outstanding shares since then.

They reduced the share count by 25% just in the last 5 years.

If you can support buybacks with a modicum of real growth, the result will be spectacular in the long term, just like NVR.

PayPal is going exactly at this direction.

It has reduced the share count by 18% in the last 4 years and is committed to continuing to do so to boost the shareholder return.

What’s better is that this is still a growing business with double-digit long-term earnings growth expectations, yet it’s trading below 15 times earnings.

Even if it can grow earnings in high single digits from here while keeping the buybacks, it’ll be a multi-bagger from the current levels.

Can it do this?

This is what we are going to try answering.

So, let’s cut the intro and dive deep into why PayPal might be one of the most attractive opportunities in the market now:

What are you going to read:

1. Understanding The Business

2. Competitive Analysis

3. Investment Thesis

4. Fundamental Analysis

5. Valuation

6. Conclusion

🏭 Understanding the Business

Every now and then, people ask me to manage their accounts and hand over their portfolios to me.

Here is the striking thing I observe—most people fail because they don’t understand the businesses in their portfolios.

Understand the business? Isn’t this literally the first thing every well-known investment book says? One Up On Wall Street, The Intelligent Investor, Common Stocks and Uncommon Profits, etc, all set out this golden rule.

So, why do people still invest in businesses they don’t understand?

I don’t think people are too stupid that they fail to understand the business or to ignore the first advice of some of the most successful investors of our time.

I think the problem is that none of these books explain what it really means to understand the business.

Is it understanding the product?

Is it solving the business model?

Is it understanding the operation?

We don’t know.

This is why most people don’t really understand the business, even if they try to stick with this advice.

What most people do is understand the product, not the business.

I was like that too when I first started working in an investment firm, then I came across Clayton Christensen’s book—Competing Against Luck.

If you haven’t read it, I recommend you do. It’ll drastically improve your understanding of businesses.

In the book, Christensen explains that businesses are there to do a specific job, not to create a specific product or service.

Products and services are just means to do the job for the customers. Bad businesses don’t understand this, and they think they just need to copy the successful products or services, and some people will pick them.

Well, those businesses fail most of the time.

Successful businesses, on the other hand, understand the “job to be done” and try to do that job. It can be a product today and a service tomorrow. The important thing is that they understand the function.

Similarly, successful investors understand the real job of the business; they don’t get stuck at the product level.

How do you do that?

Well, you have to disentangle the business into its pieces. Every business has a commodity part and a real value engine. That value engine is the real business. Once you understand that, you understand the business.

Here is an example—do you remember what was Eli Lilly’s blockbuster drug 50 years ago?

I don’t either.

Today, we all know they are Mounjaro and Zepbound, but 50 years from now, no one will remember, and Eli Lilly will be making new blockbuster drugs everybody will then know.

Because the real business in pharma is R&D and distribution.

You have to keep the pipeline coming, new drugs, new trials, and new patents, etc. You create your distribution among physicians and feed it with your drugs as they come out of the pipeline. You exploit your patent, and once it expires, you repeat with a new drug.

This is the value engine.

Nobody will remember Mounjaro 50 years from now, but Lilly will likely be in the business, making new drugs thanks to its R&D and distribution.

Take Starbucks. When you think about Starbucks through this lens, you understand that the business is hospitality, not selling a coffee. People buy Starbucks coffee because they like to hang out in Starbucks, and the association that comes with hanging out in Starbucks.

Once Starbucks thought it was selling coffee and started to remove tables from stores, its decline started. It is still trying to undo this.

Similarly, most people erroneously think PayPal’s business is sending and receiving money. No, this is just the product.

PayPal’s real value engine is its network. It’s one of the largest multi-sided networks in the world.

The development of the product proves this.

Founders spent 3 months and just a few hundred thousand dollars to create the technology, but they burned $70 million and three years to create the network.

It was so hard that they were offering $20 reward for referrals to attract users. As they created the network, this first dropped to $10 and then to $5:

Then, they completely removed it.

Why?

“The value of joining the network had exceeded everything we could offer,” says Elon Musk.

Over time, they leveraged their network to grow other products they built and acquired, evolving into a full payment ecosystem.

Today, they have a network of more than 430 million active accounts, with over 35 million merchants, and they support a wide portfolio of payment solutions:

Their core products are:

PayPal App: Their branded digital wallet that enables both peer-to-peer and merchant transactions globally.

Venmo: A lightweight digital wallet that is focused on US payments.

PayPal Payments: PayPal’s branded online payment processor.

Braintree: Developer-friendly payment gateway API, much like Stripe.

Pay Later: PayPal’s branded Buy Now Pay Later (BNPL) product.

Paidy: BNPL service is only active in Japan.

Zettle: PayPal’s point-of-sale (POS) solution is designed for in-person payments, similar to Square (Block).

Once you create an ecosystem of complementary businesses like this and convince users to adopt not just one but multiple products, very strong lock-in effects are in motion.

Products become a habit, not just a utility, and customer inertia kicks in, as long as the product does the job, they don’t want to change it just to get a bit better performance or a bit cheaper price.

This is PayPal’s real business —creating and offering value, leveraging its massive network.

Just like drugs to pharma, these products are a means of value creation to PayPal.

Just like the real business in pharma is keeping the pipeline up and coming, the real business of PayPal is preserving and exploiting its network at the same time through various interconnected products.

As long as the network is robust, the customer inertia will protect the business.

A new company entered the market with a superior technology? It’s okay, until they scale, you can match their tech as your network and customer inertia protect you.

As long as the network doesn’t decay, it’s nearly impossible for these businesses to lose in the long term.

Thus, what’s important for the cannibal thesis is how durable this network is.

It’s as durable as it gets.

Let’s dig.

🏰 Competitive Analysis

Let’s get back to the core idea in the introduction—you don’t need stellar growth to become a multi-bagger, durability will do it too.

And some of the most durable businesses in the world are networks—Amazon, Google, Meta, Booking, Airbnb, Uber, MasterCard, Visa, American Express etc..

This is not a coincidence; this is due to an economic phenomenon known as network effects.

Well, on the surface, everyone knows what this is: The more users you have, the more users you attract.

It’s true, and it’s called direct network effects, but there is another type of network effect that is even stronger—the indirect network effect.

Let’s take Facebook as an example.

More people join Facebook, and more people they attract as the utility of the platform for users grows with the user size. You have more friends on the platform, more people to engage with, a more dynamic feed, etc. Direct network effects.

On the other hand, as more people join Facebook, more advertisers are attracted to the platform. Indirect network effects.

While some platforms, like EV charging networks, only benefit from one type of network effect, some platforms benefit from both, like Booking, Airbnb, Uber, Amazon, Facebook, Google, etc.

As you can guess, those that benefit from both come to be drastically stronger networks than others.

PayPal is one of those rare businesses that benefit from both direct and indirect network effects.

A large user base attracts even more users as new users instantly gain access to the ability to send money to and receive it from over 400 million users across the world.

More users also attract more merchants as it allows them to benefit from the confidence that PayPal’s brand evokes and enables them to tap into PayPal features like one-click checkout for logged-in users, BNPL, Venmo, and crypto payments etc..

This is the first pillar of durability.

Second pillar? It’s about the scale.

Not all the platform businesses with network effects were created equal.

Actually, it’s extremely hard to create a platform business with network effects. Most networks die before they reach a minimum efficient scale to sustain themselves.

But those that reach the so-called ‘tipping point’ are extremely durable.

What the hell is a tipping point?

Look at the curve below, which shows a hypothetical network size and consumers’ willingness to pay (WTP).

Now, imagine the company is operating at the upward sloping side of the curve, the left side.

Imagine that it has reached 3 million users and aggressively introduced ads, which would have corresponded to an A+ level of WTP on the Y axis. As you see, the A+ level is higher than consumers’ WTP when the network size is 3 million. This would trigger a negative feedback cycle, and the users would start to churn, ultimately leading to the collapse of the network because no network size below 4 million supports that level of WTP.

Now, let’s assume that the business operates on the downward sloping side of the curve, the right side. At 9 million members, it introduced ads at the B+ level. That is again above the WTP that a network of 9 million members can support. People would churn, but the network would reach an equilibrium at 8 million people.

As you see, the cost of a business mistake isn’t the same on the different sides of the curve. On the left side, the network collapses, but on the right side, the network loses some members but ultimately reaches an equilibrium.

This is the illustration of the so-called ‘tipping effect.’

The highest point on the inverted U is the tipping point. Beyond that, the risk of losing and a total collapse reduces dramatically.

Even when the consumers’ WTP declines, the network will shrink a bit and settle on a new equilibrium.

This is why large networks like Meta, Google, Booking, and Uber may make big business mistakes, but they still keep thriving in the long term.

With a network size of over 430 million active users, PayPal is way beyond the tipping point.

What’s even better is that its network is still growing.

It finished last year with 435 million active users, which climbed to 438 million last quarter.

This means that PayPal’s business enjoys extreme durability.

It can make many experiments and mistakes, it can leverage the network to expand into new products, and it can even lose a few million active users.

The business will likely endure because its network is way ahead of the tipping point.

This, in turn, enables it to generate consistent cash flows necessary to become a cannibal, even if the growth completely halts in the future.

It’s an extremely entrenched business that is very, very hard to disrupt.

In the nearly thirty-year history of digital multi-sided platforms, I don’t remember any single instance where a network beyond a tipping point has been disrupted.

I don’t think PayPal will be the first one soon.

📝 Investment Thesis

My PayPal investment thesis is simple—it’s going to become a cannibal, a growing one.

I don’t think PayPal will grow skyrockets from here, all of its markets look saturated.

It’s dominating the digital wallet space in the US, and this will likely continue in the near future. Yet, outside of the US, PayPal wallet is largely a way to transact globally with peers and checkout online without exposing your credit card or bank account to sellers in third countries.

Most regions have their own digital wallet applications that dominate the domestic transactions:

PayPal is the leading player in the US, Central Europe, and Australia, and it’s trailing the local methods in most other regions.

Let’s be realistic—It’s unlikely that PayPal will take on the local applications. It had a chance to do so when these markets were new and uncontested. It couldn’t do it back then, and now it’s even more unlikely to do so, as converting users from one app to another is harder than landing them when they aren’t using any applications.

The good news is that it works both ways—PayPal is also unlikely to lose its core users to other apps.

The online payment gateway & processing software market is no different.

PayPal is leading this market globally with 41.87% market share:

This is also a pretty much-saturated market, especially when it comes to PayPal’s core regions, i.e, the developed markets.

As we have discussed above, this is a market where direct and indirect network effects are at play.

Customers who got used to clicking “Checkout with PayPal” are unlikely to opt in for other payment methods as long as the merchants don’t change their processor. Merchants don’t generally do this as it means spending a developer's time and assuming an operational risk. Plus, they don’t need to override PayPal to add other checkout options.

Result? PayPal's network and brand recognition provide it with a strong competitive advantage that enables it to generate consistent cash flows.

What’s even better is that its network is well-positioned to generate modest real growth even without much business effort.

It’s essentially a tool-bridge between the sellers and merchants, making money through percentage-based commissions.

Thus, it benefits from three natural growth drivers:

Inflation.

Population growth.

Global economic growth.

As merchants try to price their products ahead of inflation, PayPal’s transaction dollars are also automatically poised to generate real growth long term.

Second, as the population grows, the PayPal network will likely experience organic growth, which will also drive transaction volume growth.

Third, PayPal will benefit from the rapid economic growth in emerging markets. Currently, it has the widest global availability among all payment apps:

Its global coverage allows it to benefit from the rapid economic growth in emerging markets, which are poised to grow at around 4.5% annually in the next decade versus 2% in developed markets, according to the IMF. PayPal isn’t dominating these markets, but it still has considerable exposure, which is an additional tailwind.

On top of these structural factors, PayPal is still innovating to drive growth.

One such initiative is PayPal's off-site ads.

PayPal has accumulated an incredibly useful dataset as to the shopping behaviors of its users spanning over two decades. It knows who is interested in what products, what the average basket size of any user is, what time of the day they are more likely to shop, etc..

It has introduced off-site ads that leverage this data. Once a customer sees this app online, they can check out with PayPal pretty easily, smoothing out the process and driving conversions:

Mark Grether is running this division, which makes me incredibly bullish about the future of this product, as he previously scaled Uber Ads to a billion-dollar business.

Will this double the size of the business? Of course not. However, these efforts, when combined, can generate real incremental growth, which will be incredibly valuable for PayPal going into its maturity.

What’s the takeaway? PayPal is well-positioned to generate consistent cash flow that can even grow modestly every year in the foreseeable future.

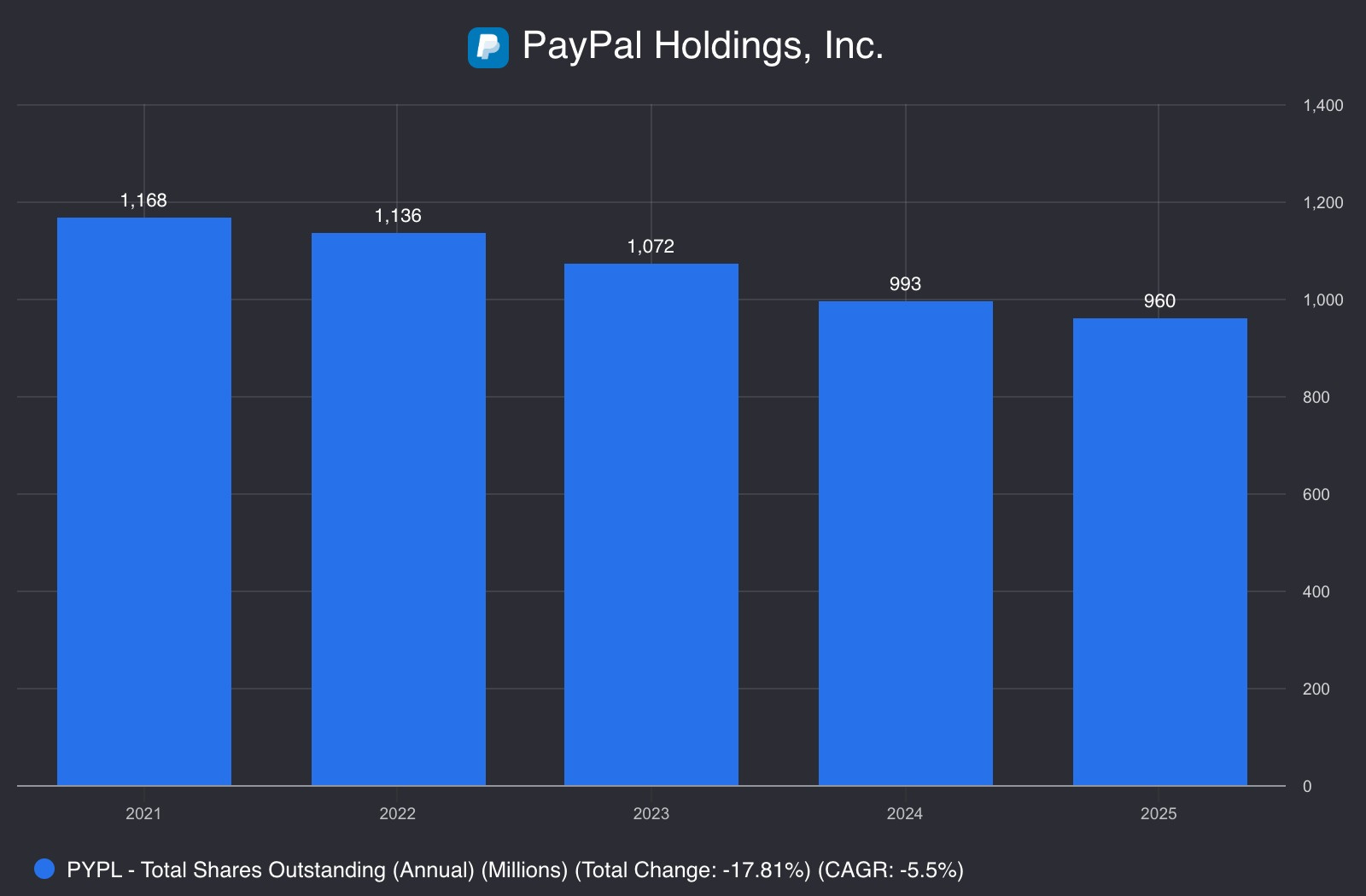

This will allow PayPal to buy back shares pretty aggressively as it has done in the last 4 years:

Aggressive buybacks, combined with organic growth, will drive significant long-term EPS growth, potentially turning PayPal into a long-term compounder in the same fashion as NVR.

This is where PayPal is, and should be, heading.

📊 Fundamental Analysis

➡️ Business Performance

Consistency—this is what summarizes PayPal’s performance in the last 5 years.

It grew the top line consistently at an annualized rate of 9.5%, while earnings and free-cash-flow remained largely stable:

Wait a minute? Why did the earnings remain stable while the top line grew pretty consistently?

Earnings were heavily affected by gains from its strategic investment portfolio, which led to overstatement of earnings, especially in 2020:

This has largely stabilized in the last two years, so nearly all the profit in 2024 came from operations.

If you take out the non-operating income, we see that it has grown operating income at an annualized rate of 13.7% in the last 5 years:

This is a phenomenal performance in my opinion, especially when you consider that this is a 27-year-old business with the largest online payment gateway in the world, and operations in over 200 countries.

It simply has very few options to drive growth in its core business, yet it has achieved this.

These figures, in no way, signal a dying business.

If anything, I think they signal a business that is entrenched in its industry and entering its maturity phase, where it’ll enjoy moderate but consistent growth, above-average ROIC, and high shareholder yield.

If you adjust your expectations, give up the idea that it’s a growth company and think of it as a stalwart, much like Apple today, I think you’ll see a potential compounder.

I definitely do.

➡️ Financial Health

Simply rock solid.

There is not much to discuss about its balance sheet:

It has $20 billion of equity against $12 billion of debt. What’s even better is that its EBITDA can pay off all the debt in the balance sheet in just two years.

What I like is that the management has insisted on conservative management of the balance sheet over the years. Its Debt/EBITDA ratio has never gone beyond 2.5 in the last five years.

Overall, I don’t think its balance sheet deserves much commenting—it’s rock solid.

➡️ Profitability & Capital Allocation

Take Rates

Think about Costco and Walmart.

They are essentially massive retailers that mark up products and resell them to make money. Their massive scale and economies of scope allow them to drastically reduce fixed costs per product. They pass this as cost savings to customers, minimizing their mark-up, which in turn attracts more customers and drives growth.

Amazon does the same.

We are all in love with this model. Customers celebrate these companies for doing that, and investors think of this as a giant moat. And it is.

Recently, I started to see many people celebrating Wise on Twitter (X) for adopting this model in finance:

Scale economies shared? People are basically praising a company for cutting its take rate because this resembles the Costco model, as it comes with increasing transaction volume.

Let me tell you something—this is PayPal all along:

It’s incredible how narrative drives the discussion.

When a fast-growing company has declining take rates and increasing volume, people see it as the Costco model in finance, and investors go crazy about it; when they see PayPal’s declining take rate, they think it’s a dying company.

Here is what I think—I don’t think PayPal is dying or declining.

Despite the declining take-rate, PayPal has grown its top line and operating profits considerably in the last 5 years.

Yes, it’s probably feeling competitive pressure, but it’s been able to respond to this pressure pretty successfully.

Quarterly volume more than doubled while the take rate shrank just 26%. As long as this trend continues, I don’t see any problem.

You can just shift the narrative and say PayPal is the Costco of payment companies.

Return on Capital Employed (ROCE)

PayPal’s median ROCE in the last 5 years was 13.4%.

Though not amazing, this is a bit above average for the mature American companies, which is 12%.

The good news is that it’s been increasing since Alex Chriss took over as the CEO in 2023. I believe this trend will continue since the reinvestment requirement will decline as the company transitions to maturity.

I expect it to stabilize around 15% in the long term, which is a satisfactory return on capital for a company at the size and age of PayPal.

In sum, despite all the “dying company” narrative around PayPal, everything is going in the right direction. Business is performing satisfactorily, generating nice returns on capital, and the balance sheet is strong enough to weather any financial storm.

There is one last question remaining—is the valuation right?

📈 Valuation

This is where the rubber meets the road.

All the things we do in analyzing businesses, we do it to forecast what it’s worth.

We figure that out, and we buy the stock if the price is under what we think it’s worth and avoid it if it’s above.

Thus, the central question of the whole equity analysis is whether we can predict the earnings. If we can’t, there is no way to know what it’s worth.

Thanks to its giant network, ecosystem lock-in, and customer inertia, PayPal’s earnings are extremely predictable, and there is nothing that’ll disrupt it in the short to medium term.

Once this is established, the job is pretty easy:

Make some conservative assumptions, consistent with the thesis.

Run the numbers.

So, let’s be very conservative and assume that the business will grow earnings by just 10% annually in the next 5 years.

It can easily do this as the management is guiding for high-single digit/low double digit long-term annual revenue growth.

This will give us $7.5 billion in net income in 2030.

Now, let’s get to the buybacks.

The business shrank its shares outstanding 16% in the last 5 years. Let’s assume that it’ll hold this trend and decrease the shares outstanding by a total of 15% until the end of 2030, giving us 850 million shares at the end of 2030.

Dividing the net income by shares outstanding gives us $8.90 EPS.

Give it a conservative 15 times exit multiple, and we are looking at $133.5 stock per share, double of today’s price.

In other words, the stock is offering a 14.8% annualized return in the next 5 years.

This is the effect of becoming a share cannibal.

Can it keep doing this long-term?

I don’t see any other path for meaningful shareholder return.

It’s an entrenched company in its market, but the real growth opportunities are limited.

The best option to generate shareholder return for this business is to combine moderate organic growth with aggressive buybacks. In this case, it can generate around a 14-15% annual return in the long term, effectively becoming a cannibal compounder.

If you are looking to deploy capital in an all-time high market where opportunities have largely dried up, I think PayPal offers favorable risk/return from this level.

🏁 Conclusion

If you want outsized returns in the market, multi-baggers are the name of the game.

Most people know this, but most people mistakenly think that they need to find very small businesses with explosive potential to get there. While that is a path, more often than not, it drives people to make speculative bets, and they end up making money.

Yet, if you can find a business that will be around 20 years from now and it can grow earnings in low-double-digit percentages every year while returning the capital to shareholders, you may end up with a hell of a result.

Where do you find those businesses?

They come in all shapes and colors, but if history taught us one thing, multi-sided networks are prime candidates.

Take American Express.

At the beginning of 1995, it was already a very large corporation, having been a member of the S&P 500 since 1976. It was trading at $8 per share split split-adjusted price back then.

Fast forward 30 years to 2025, and the stock is trading at $297 per share, 37x in just 30 years, while the S&P 500 made just 10x in the same period.

American Express compounded at 12.8% annually since then, while the S&P 500 appreciated 8.15%. The difference? 37x against just 10x.

PayPal carries the fundamental characteristics of American-Express.

It’s one of the largest and strongest payment networks in the world, it has a very low reinvestment requirement, and it benefits from natural drivers of growth like inflation, population growth, and global economic development.

Can it make 5x in the next 5 years? Unlikely.

Can it generate a 12.8% annual return like American Express in the next 30 years?

It has everything to achieve this.

So, if you are looking for something to park capital and collect above-average annual returns, PayPal is for you.

But if you buy it with an expectation for accelerating growth and get disappointed when it doesn’t happen, you should avoid it.

The thesis for PayPal isn’t about fast growth.

It’s consistent cash flows, aggressive buyback, and long-term value creation.

To add to the thesis, also is one of the first company to adapt crypto payments. I think that is gonna give a big jump

Great read. I think JD.com also falls into this category.