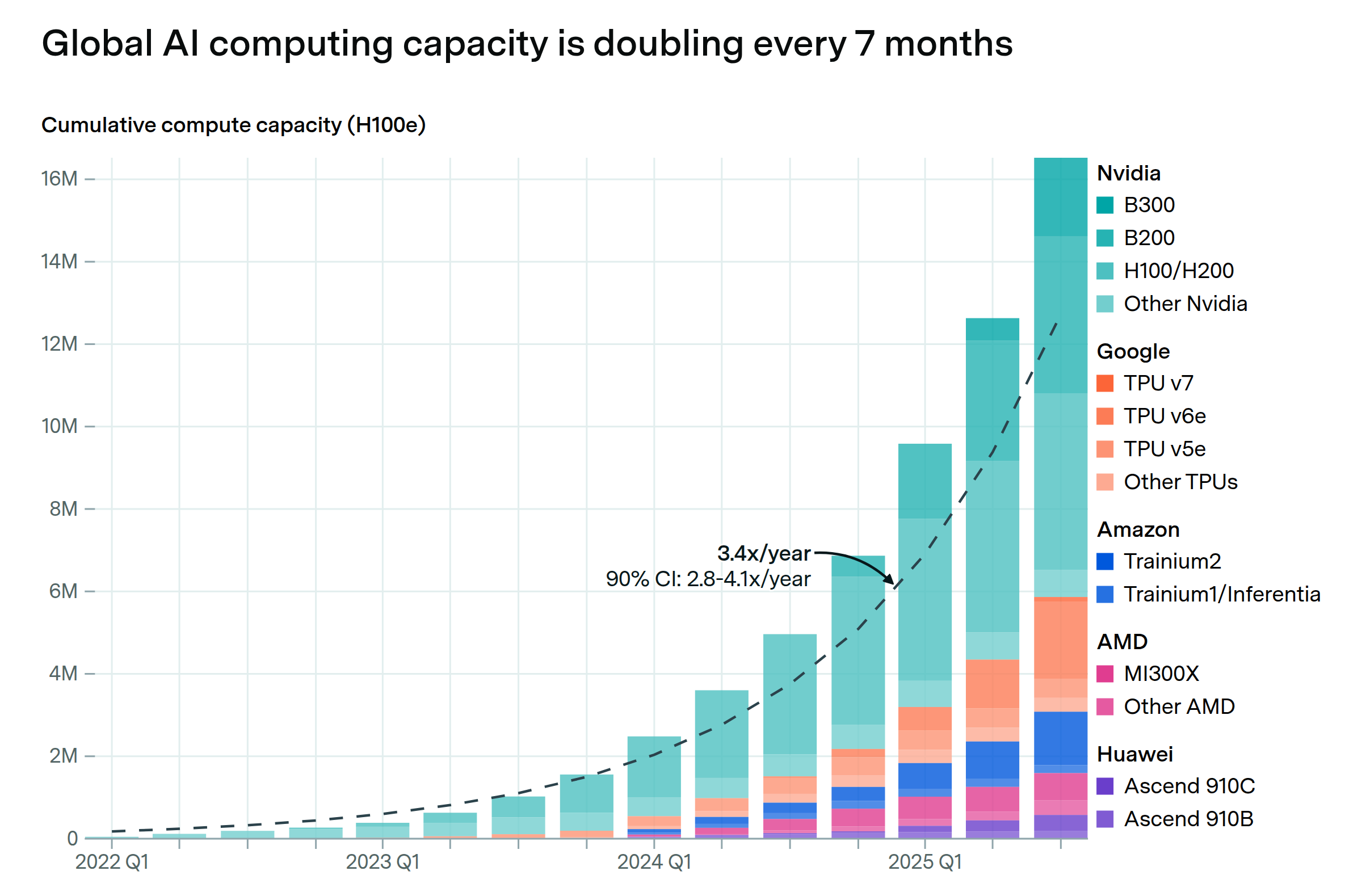

More Compute, Please.

Even the most optimistic estimates underplayed the compute we need.

“As fast as we put the capacity in, it's being consumed.” — Andy Jassy, Amazon CEO, said this in Amazon’s Q1 earnings call last year.

Almost a year later, after he said the words above, we read in his annual letter earlier this week that:

Tarinium 2 capacity was sold out.

Trainium 3 is almost fully subscribed.

A part of Trainium 4 is already reserved.

Not ju…