Microsoft: Undervalued & Undisruptable!

Sometimes the best opportunities hide in plain sight. Microsoft is one of them.

Chris Hohn once said: “Good companies are likely to remain good, and bad companies are just bad.”

Look at other successful investors, and you’ll see they have said similar things.

Terry Smith: “Good businesses tend to stay good, bad businesses tend to stay bad.”

Warren Buffett: “Time is a friend to a good business and an enemy to a bad one.”

Pulak Purasad: “Great businesses remain great. Bad businesses remain bad.”

It’s a recurring theme because it’s true. Look at all the legends, and you can probably name one defining investment that’s done amazingly well over decades, not years.

Buffett bought American Express for Berkshire back in the 1990s, and it’s still holding it; Chuck Akre held American Tower for over two decades; Philip Fisher bought Motorola in 1955 and held it until his death nearly 50 years later, etc.

All these businesses were subject to a lot of talk about disruption and about why they wouldn’t perform well over the next decade while these investors held them.

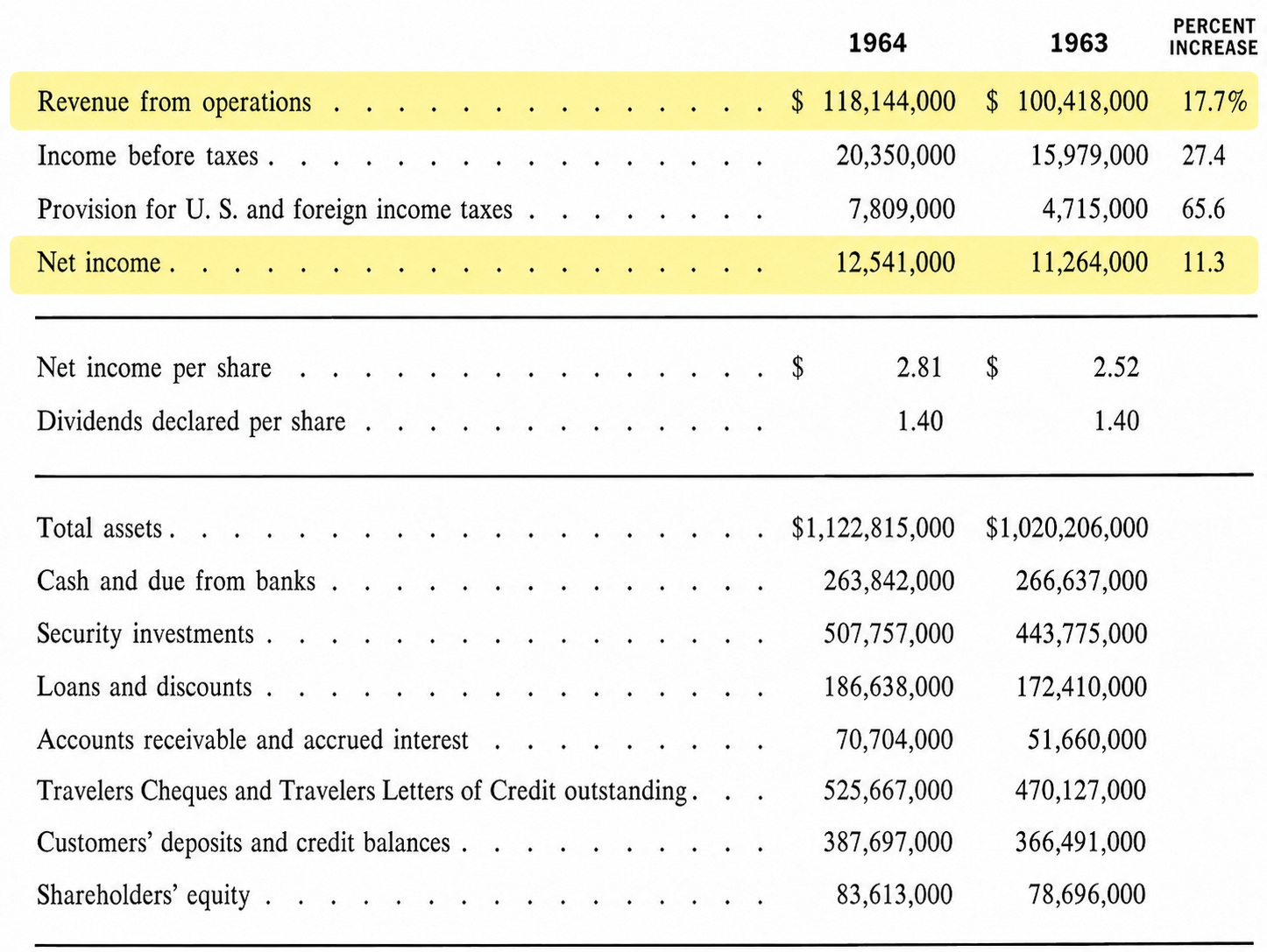

Look at American Express financials in 1964 when Buffett bought it, and you’ll see:

Its revenues grew by 17% and net income by 11%.

Over the next 6 decades, many times people thought American Express would be disrupted. When credit cards started killing travel checks, when Visa pioneered open-loop card networks, when PayPal spearheaded mobile payments, when Apple launched Apple Card, etc.

Yet, fast-forward 6 decades, American Express grew revenue by 10% last year and is projected to grow by 15% this year.

Exceptional companies tend to stay exceptional.

You may object and say, “But many companies thought to be exceptional have been disrupted like Kodak, Blockbuster, Blackberry, etc.”

What distinguishes exceptional companies from simply the strong ones is their adaptability. Exceptional companies are often defined by a timeless function rather than a particular product. This gives them adaptability and durability.

Again, take American Express. It fills a timeless function—facilitating commerce.

It used to do it with travel checks; now it does it with credit cards and mobile payments. Times have changed, and it adapted because what defines it is a function.

Of course, everything can eventually be disrupted. But thanks to being function-driven and the adaptability that comes with it, 9 out of 10 cases where the market suspects disruption prove to be a great buying opportunity for long-term compounding.

If you can analyze the circumstances objectively and assess the company’s position, you can tell an opportunity from a threat and capitalize on it.

Google is a recent example.

The market thought it could be a potential AI loser and hammered the stock in early 2025. Yet, if you scratched the surface a bit, it was obvious that Google was perhaps the best-positioned company to win AI. The stock is up 2.5x since then.

Now the same thing is happening with Microsoft:

The stock recorded its steepest quarterly decline since the 2008 Financial Crisis as the market is worried about AI’s impact on software and its returns on AI capex.

The question is simple—is Microsoft an exceptional company that occupies a critical function with adaptability just like American Express, or is it simply a strong company that’s still receptive to disruption like Kodak, Nokia, Blackberry, etc?

If it’s the former, we are looking at one of the best buying opportunities in the market; if it’s the latter, there is no low enough price to justify taking the risk.

So, let’s cut the BS and dive deeper into Microsoft to answer this question.

What are you going to read:

1. 🏭 Understanding The Business

2. 🏰 Competitive Analysis

3. 📝 Investment Thesis

4. 📊 Fundamental Analysis

5. 📈 Valuation

6. 🏁 Conclusion

🔑 Key Takeaways

🎯 Microsoft is one of the strongest businesses with the ability to spawn new businesses over different cycles of technological change.

🎯 The market currently sees the software business as the weak link and is questioning ROI on capex. This has sent the stock spiraling down.

🎯 Its software business isn’t threatened by AI, as it’s the default medium of exchange for knowledge work and will remain so. AI capex is also closer to generating positive ROI than the market thinks.

🎯 There are ample growth opportunities ahead thanks to the AI boom and changing pricing model of software.

🎯 The current price implies around a 13% discount to fair value even based on conservative assumptions.

🏭Understanding the Business

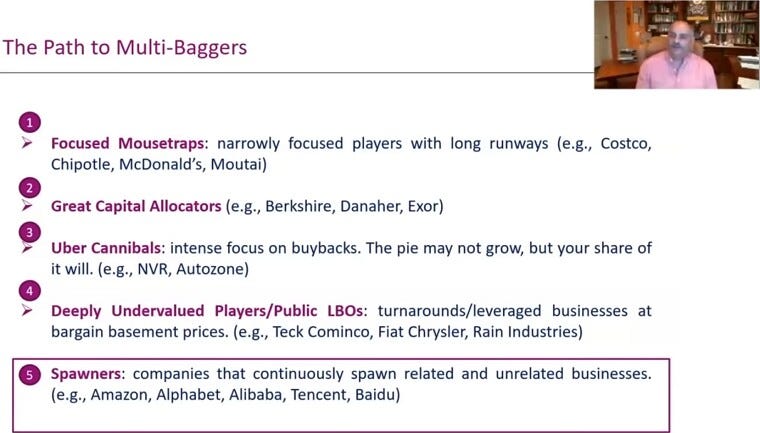

“Spawners.”

What the hell is a spawner, you may be asking. I heard this word for the first time from Mohnish Pabrai. Up until I heard it, I was using “anomalies” to describe the same phenomenon, but I think spawner is a much better fit.

It simply refers to a group of companies that manage to successfully expand out from their core markets and dominate several other markets as well, related or unrelated.

What makes them different from conglomerates is that spawners create or buy assets that are substantial growth drivers in their own capacity, while conglomerates usually deal with more mature assets. Thanks to this relentless focus on growth and domination, successful spawners also tend to be the best-performing assets.

Look at Amazon, for instance. It currently has 4 businesses each making more than $50 billion a year—online stores, third-party seller services, cloud, and advertising.

Spawners existed for a long time, but at no point in history have they become as big as the spawners we see in the digital markets. This is for two reasons:

Digital markets removed physical boundaries on growth.

No physical boundaries among product markets made it easier to leverage dominant position across different products.

Microsoft is arguably the first company that discovered the potential of spawning in digital markets, and thus can be considered the original spawner of tech.

Its 50-year history is defined by expanding into markets adjacent to its core products, dominating those markets as well, and then using them as a stepping stone for expanding into even more markets.

When it first started in 1975, it had nothing.

Bill Gates and Paul Allen were friends from Lakeside High School. Both were obsessed with coding, which was the basis of their friendship. They were a part of the small group that colonized the Teletype room in Lakeside. It was called the Lakeside Programmers Group, and other members included Ric Weiland and Kent Evans.

They had one common belief that glued them to the Teletype room—computers would change the world.

They parted ways as Allen headed to Washington State University and Gates to Harvard. In 1974, Allen dropped out of Washington State University and moved to Boston, largely to be closer to Gates and pursue entrepreneurial projects together. They had nothing in mind.

One day, Allen saw that January 1975 issue of Popular Electronics magazine was featuring a device called Altair 8800, a $397 hobbyist computer with no keyboard, no screen, and no software:

He bought the issue and rushed to Gates’s dorm room at Currier House and said they were about to miss the revolution they had been waiting for.

They called the manufacturer, MITS, and claimed they had a BASIC interpreter ready for the machine. They didn’t. They hadn’t even seen a real Altair. They wrote the code in eight weeks on a Harvard mainframe simulating a chip they had never touched, and when Allen flew to Albuquerque in early 1975, the code ran on the first try.

Suddenly, they had a company.

They named it micro-soft because this was what they were doing—software for small computers.

It looks coincidental now, but they actually had the spawning thesis early on, though in different words. Their original mission statement was “a computer on every desk and in every home.” This meant a massive TAM expansion which would unlock larger opportunities, and Microsoft would capture these opportunities as they emerge.

This is exactly what happened since then.

They spent the early years selling their catalogue of programming languages to microcomputer makers like Commodore, Tandy, etc. This elevated them in the market as the one platform-agnostic provider that everybody already knew. So, when IBM rushed into the personal computer market in the early 1980s, Microsoft was already a perfect fit to supply an operating system.

At the time, Microsoft didn’t have any operating system, and they had neither time nor R&D to make one. Gates made one of the most famous opportunistic moves in the history of technology entrepreneurship. He bought an operating system called 86-DOS from a small outfit named Seattle Computer Products for roughly $75,000, renamed it MS-DOS, and licensed it to IBM. So, the first IBM PC shipped with MS-DOS in 1981.

The crucial thing for Microsoft was that IBM didn’t ask for exclusivity.

So, when other box makers reverse-engineered the IBM PC, they flooded the market with IBM clones that also had Microsoft as the operating system, thereby making it the dominant company in operating systems.

This is not the only spawning Microsoft did in the 1980s. As they were making inroads in the operating system market, they were also building another business with giant potential—productivity software for computers with graphical interfaces.

As mentioned above, by the 1980s, it was already well-known among the box makers as a platform-agnostic provider of software. This led to Steve Jobs hiring Microsoft to create software for its upcoming computer with a graphical interface, the Macintosh.

Most of Microsoft’s productivity software was developed for Macintosh. They became very useful when IBM clone box makers that were shipping with Microsoft's operating system also upgraded to graphical interfaces, and Apple refused to license macOS to them. Microsoft developed the OS and bundled it with its productivity software.

Suddenly, both its operating system and productivity software businesses were booming as box makers flooded the market and Apple declined following Steve Jobs’ departure. Thus, just within two decades of its founding, Microsoft had spawned two giant businesses—operating systems and productivity software.

Spawning is self-perpetuating in the sense that the more businesses you spawn, the more adjacent and complementary markets you have, so the more opportunities you see.

By the early 2000s, Microsoft was the dominant company in productivity software and operating systems. Thus, when the internet got popular in the late 1990s, hundreds of millions of people were relying on Windows machines as their gateway to the internet.

Microsoft thought it could leverage its dominant position in operating systems to spawn another giant business—consumer services hosted online, like MSN, Hotmail, Bing, etc. Yet, this was a very different business from packaged software because it required running hyperscale data centers to host millions of global users.

They knew that it would take a lot of capex and would be loss-making, as they would have to offer them mostly for free. It indeed played out exactly as expected.

Microsoft spent a lot of money in creating its data-center infrastructure, but ended up losing these markets anyway. However, thanks to these efforts, it was one of the few companies on earth that knew how to build and operate a hyperscale infrastructure.

When cloud computing started to take off in 2007, Microsoft was already ready to capitalize on it, so they entered cloud in 2008.

The first years of it were a disaster.

Its first commercial cloud was a platform-as-a-service. You would write an application in a specific format, and they would run it for you.

It was architecturally elegant but commercially wrong because IT departments were used to running applications on physical servers in the company basements. Microsoft was asking them to rewrite applications in a specific format. What customers wanted was Amazon’s cruder offer—give me the virtual machine and leave me alone.

Naturally, it failed to take meaningful market share from AWS initially.

They renamed the platform to Azure in 2010 and appointed Satya Nadella as its CEO in 20211.

Nadella rebuilt Azure as an infrastructure-as-a-service, a direct AWS competitor. That was the right architecture and the right offer for the demand. So Azure took off and started to take market share from Amazon. This turnaround won him the CEO role post-Ballmer.

Now Azure is at $100 billion annual run-rate with 21% market share in enterprise cloud infrastructure. It’s another giant business Microsoft has spawned over 5 decades.

And this is exactly how you should see Microsoft.

If you see it just as a big technology company with several businesses, you’ll miss the essence. Microsoft is a spawner.

It generates insane amounts of cash flows thanks to its dominant position in existing markets.

Then, when it sees an opportunity in an adjacent or a complementary market, it leverages both cash flows and customer base to expand into that market.

It turns the new business into its new growth engines and cash cows for the future and repeats the whole process. Self-perpetuating cycle.

At this stage, Microsoft is one of the most successful spawners in history that’s spawned dozens of businesses, and generates over $318 billion in revenue, $125 billion in net income, and $72 billion in cash flows over the last twelve months.

As you could guess from the process above, two things are crucial for Microsoft’s spawning:

Viable adjacent/complementary market for expansion.

Cash flows that enable it to capitalize on the opportunities.

It has both now.

AI cloud is an exciting new market adjacent to the traditional compute cloud, and it has all the cash flows to capitalize on it thanks to two businesses it previously spawned—productivity software and OS.

Looking at its spawning track record, the market should have been extremely excited, and the stock should have been trading at a substantial premium.

Yet, it’s posted its worst ytd performance since 2022.

Why is it?

Is it justified?

These are the two questions all the alpha will be derived from when it comes to Microsoft.

Let’s dig.

🏰 Competitive Analysis

I received the single best investment advice when I was in law school. It belongs to one of the top Business & Tax Law Professors in the US, Steven Bank.

It reads exactly as follows— “if you can find a company that’ll be around 20 years from now, you’ll likely make a lot of money.”

That stuck with me.

It feels mind-numbingly simple, but if you think about it, you see that it captures all the essentials of value creation.

If it’ll be around 20 years from now, it’ll capture natural growth from inflation.

It’ll also benefit from increasing population, as it’ll drive volume growth.

Even if you overpay, 20 years is long enough to offset most overvaluation.

All that suggests the single most important thing you should decide is the durability of the business, and everything else is secondary.

What provides durability is the competitive strength of the businesses, or the so-called concept of “moat.” If you read competitiveness as durability and not as the narrow fight for market share in the Porterian sense, you easily understand it has two aspects:

Durability against alternatives that emerge over time thanks to technology.

Durability against the existing alternatives.

So, if you decide that durability exists, the only thing left to be decided is valuation.

You can assume base growth will be given due to inflation and population growth, but you can’t be so sure about potential growth from innovation. So, what you should do is make conservative assumptions based on inflation+volume growth and buy when valuation looks low enough.

You basically have two core decisions to make. That’s it.

For decades, the durability part has been taken for granted for Microsoft due to its dominance in operating systems and productivity software. Most computers shipped were Windows, and they carried Microsoft Office as their default productivity software, which made Office the standard among individuals and enterprises.

This gave Microsoft immense pricing power, which led to an explosion of cash flows as its marginal cost per additional product was nearly 0:

Now this is changing as the market thinks AI is a software killer and Microsoft is software. So, suddenly its cash flows from software don’t command the same premium they used to. It further worries the market that Microsoft is spending its software cash flows on AI compute, which is yet to generate a solid return on investment.

So, suddenly, in the market’s eyes, Microsoft is using less durable cash flows to fund low-quality investments. And the stock naturally got hammered.

The key thing to focus here and decide is the former part—whether software cash flows are really less durable.

Because if cash flows are durable, the worst-case scenario is Microsoft wasted a few years of cash flows, which doesn’t detract much from terminal value, and the stock would recover when Microsoft stops wasting cash flows.

This is exactly what happened with Meta in 2022-2023. The stock dipped because it burned billions of dollars in the Metaverse, which didn’t generate any ROI, but the stock recovered when Meta committed to efficiency.

Given the current reaction, the market is afraid that they are not as durable as they used to be. I don’t agree.

What the market is doing now is confusing low replacement cost with the ease of replacement.

Before AI, producing software was costly, especially new software. Developer/hour was already high, and the products would generally require a few rounds of iteration before they achieve product-market-fit. For this reason, software used to come with pretty high sunk costs.

AI basically collapsed the cost of development.

The market thinks that now the cost of development is converging to zero; the cost of replacement will also drop drastically. As a result, the overall software industry has been going down, dragging Microsoft alongside it.

It’s wrong to see Microsoft software through this lens.

Most of Microsoft's software was developed in the 1980s and 1990s.

Microsoft Office bundle was launched in 1988 and came to Windows in 1990. So, it’s actually pretty primitive software that we know how to replicate for decades. Development cost or hardship was never the reason Microsoft has proved durable all these years. Thus, AI can’t remove a barrier that didn’t exist in the first place.

You should think of Microsoft software in the same way as WhatsApp.

Development hardship or costs were never the reason WhatsApp hasn’t been disrupted. There have been thousands of messaging apps launched after WhatsApp, proving that replicability was always there.

And objectively, there have been better productivity software than Microsoft Office and better messaging apps than WhatsApp, but both Microsoft Office and WhatsApp still dominate; why?

Two reasons; one is obvious, the other one is less obvious.

The obvious one is that both WhatsApp and Microsoft Office software are networks. This is less obvious for Microsoft software because it creates externalized network effects, unlike WhatsApp, which creates internalized network effects.

The difference is simple. In internalized network effects, value is captured by the network operator; this is why they are generally in the form of platforms where it’s easy to capture value for the operator. In externalized network effects, value flows outward to users by empowering them.

Microsoft software creates substantial externalized network effects as it’s the default medium for the exchange of knowledge work. The value added increases with every exchange, every revision, and this is captured by the transacting parties themselves, not by Microsoft.

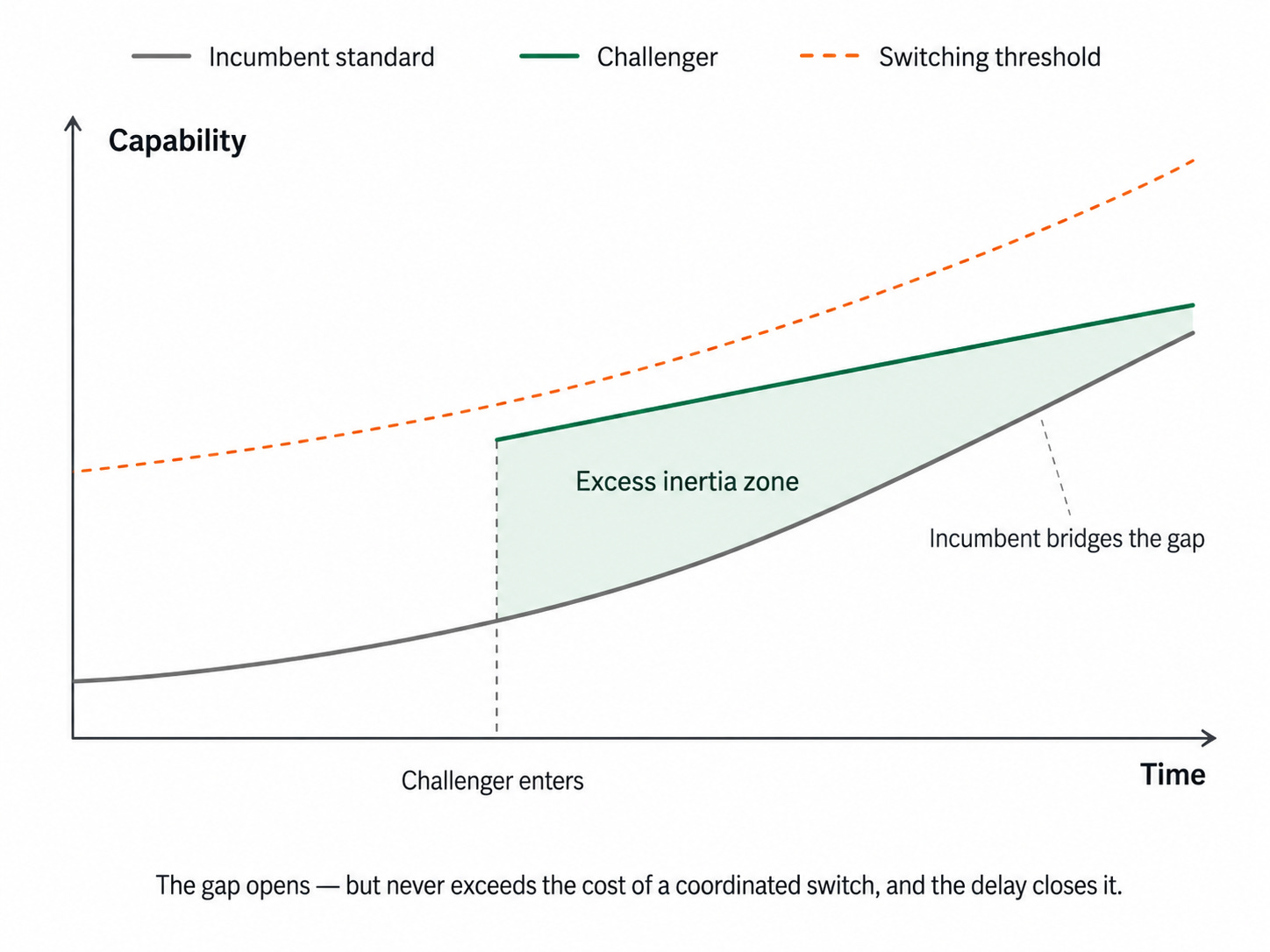

The less obvious one is that this external value capture by the users of the network leads to what economists Joseph Farrell and Garth Saloner describe as “excess inertia” in their influential paper titled “Standardization, Compatibility, and Innovation”.

The setup is simple: Two firms sit on an old technology standard, and a better one appears. Each firm prefers the new standard if the other also moves, as compatibility is more important than the upgrade itself. As no firms want to take the risk of incompatibility, a comprehensive switch happens only rarely.

This effect is elevated when the capability ceiling of the standard is not that high, meaning switching to a new standard doesn’t offer much capability expansion. When this is the case, excess inertia is stronger.

This mechanism almost always leads to continuity of the incumbent dominance, as delay gives opportunity to the incumbent standard to bridge the capability gap. Once the capability gap is closed, there is no incentive to switch at all.

This means a displacement is most likely when there is:

High capability ceiling

Wide capability gap between incumbents and the newcomers.

In the case of Microsoft software, the capability ceiling is pretty low. According to surveys, 90% of customers use less than 10% of Microsoft Word functions. For Excel, it’s less than 5%. As a result, excess inertia is very strong. This will likely give Microsoft the opportunity to bridge any gap that could emerge with competing products or AI models directly.

The fact that people still transfer their AI-generated work to Microsoft software before sharing it validates this excess inertia stemming from compatibility. They don’t want to leave Microsoft software; they want AI to use Microsoft software for them. Leaving Microsoft software doesn’t obviate the need for a common standard, and why leave an existing standard if novelties don’t promise much excess value?

This is why WhatsApp has remained the standard, not because of lack of competition or better alternatives. This is exactly why Microsoft software will remain the standard medium of exchange for knowledge work as long as computers remain the main device where knowledge work is generated. This is the critical function of Microsoft software, just like facilitating commerce is for American Express, ensuring adaptability which leads to durability.

This reverses the script that software cash flow is no longer S-Tier.

They are, and they’ll remain S-Tier. So, durability is still there. Change of perspective from “no longer durable” to “still durable” changes how AI capex should be seen as well. In the worst-case scenario, Microsoft is spending money on a low-ROI investment, which doesn’t detract much from the terminal value, provided the durability.

We saw this with Meta’s investment in the metaverse. That proved to be a literal negative-ROI spending, yet once Meta was done with it, the stock recovered in no time.

I believe this makes the case that Microsoft is as durable as ever.

We should emphasize here that this durability of cash flows also reinforces its position in the cloud computing market and ensures durability there.

It’s because cloud computing is basically a scale business, as you are making margins on compute. Larger scale means more bargaining power and priority with suppliers, which means faster build times and more attractive offers to customers, which brings even more demand and leads to an even larger scale.

As a result, the market is dominated by companies that could scale faster and further by reinvesting gargantuan cash flows generated by their other businesses. Look at all the cloud giants- Amazon, Microsoft, Google, Alibaba, Oracle- and you see that they are the companies that generate enormous cash flows in their other core businesses.

This creates a vicious cycle where those that already have the scale end up with even larger cash flows they should allocate, which leads to even larger scale, keeping the market as an oligopoly.

So, in short, Microsoft has no problem of durability. Software cash flows are as durable as ever, and it also contributes to the durability of the cloud business, which also self-perpetuates itself thanks to the oligopolistic market structure.

As the durability is established, the investment decision turns to valuation, which is closely related to growth prospects.

So, to determine whether the valuation is right, we have to understand what optionality we have on the table so we can price it accordingly.

🏰 Investment Thesis

My Microsoft investment thesis relies on three pillars. These are the key optionalities I see for Microsoft going forward.

1️⃣ Cloud computing will grow secularly.

To understand the growth potential of cloud, you have to see that AI will be a General Purpose Technology (GPT).

What the hell is a GPT?

GPTs are the technologies that are critical inputs to other innovations. This is why demand for GPTs grows secularly for long periods of time.

Take electricity as an example.

It’s a GPT, as it enabled the industrial revolution and computer revolution. Today we are still making new gadgets and developing technologies that consume electricity. So, electricity demand keeps growing secularly even though it’s been two centuries since it was discovered.

The internet is another GPT, and it follows the same trend. It’s enabled the invention of many other technologies like social media, streaming, e-commerce, etc. So, demand for internet bandwidth has grown secularly as illustrated by the internet traffic over time.

AI is also a GPT as it’s an input to many other technologies that we currently use and the ones to be invented. Take search. It’s now AI-powered. AI does the web search instead of humans and fetches the information. It can use the computer for you to do everything you do on a computer and more.

Many gadgets and devices we are currently using will be AI-pilled and made smarter this way. Cars are the classic example. Then of course we’ll produce new and more capable types of robots running on AI. Even home appliances will likely be made smarter by AI integration.

All this AI demand will flow through data centers, so the cloud computing market will grow secularly, just like demand for electricity and the internet have grown secularly since the day we first used them.

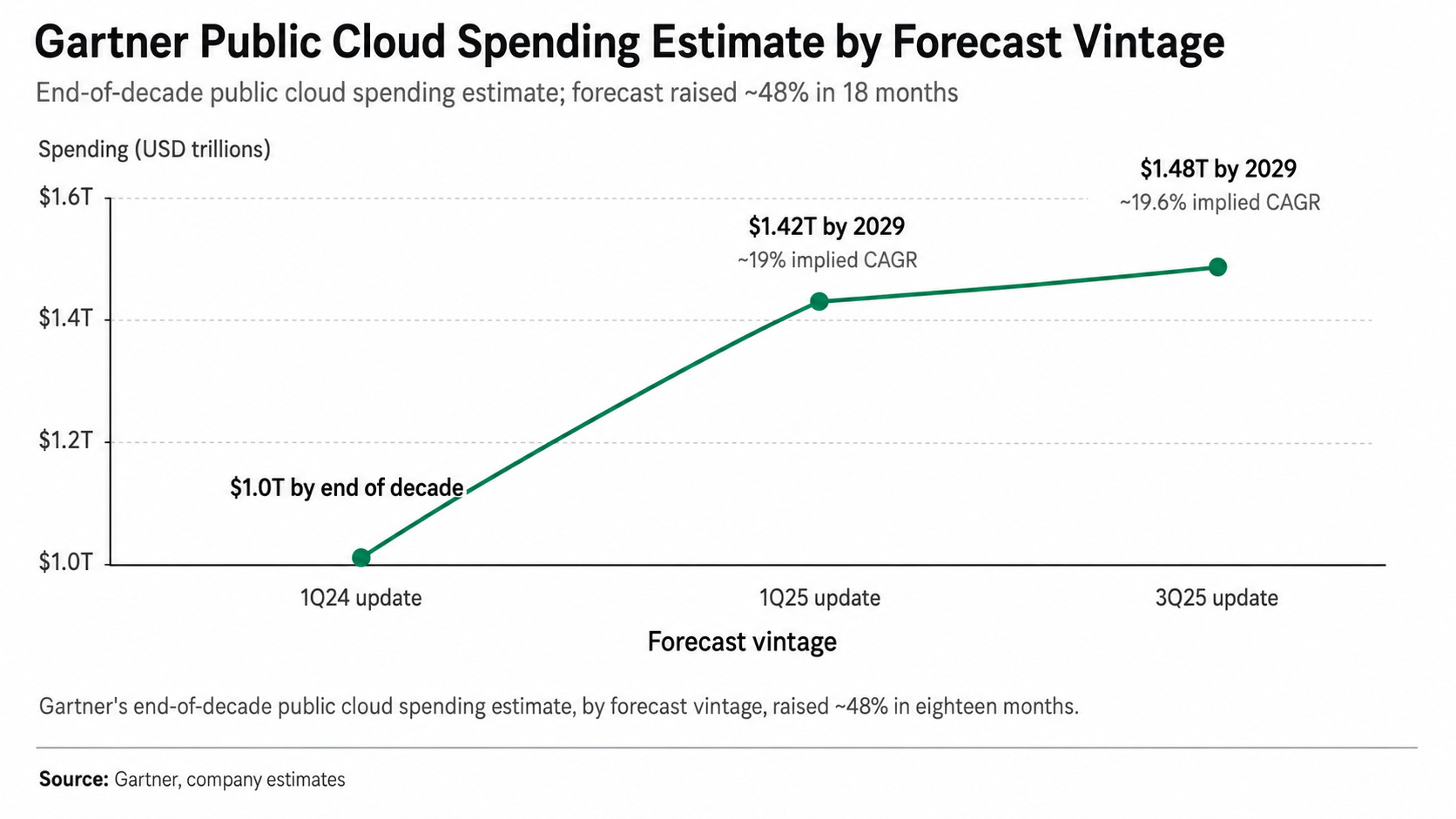

Gartner’s revising their 2029 market size estimates by 48% in 18 months proves that demand growth outpaces even the most optimistic assumptions. This is indeed what we see in GPTs.

Microsoft reportedly holds 21% market share in this market currently, according to Statista. So, based on Gartner’s model and assuming no increase in market share, Microsoft can generate around $310 billion cloud revenue in 2029. This is more than 2x its total cloud revenue over the last twelve months.

And this is the base case. As explained, GPTs drive secular demand. So, these figures will likely be revised upward, as they were twice in the last 18 months.

2️⃣ AI Capex Will Turn ROI Positive Faster Than Expected

One of the main concerns surrounding AI capex is the worries about positive return on investment. Initially, the market didn’t think much about it and assumed all compute capex would turn out to be wildly profitable as traditional cloud has been.

Then, as capex exploded and reports came out to suggest that enterprises were struggling to generate positive ROI on spending, the market became more skeptical of hyperscaler ROI.

However, the latest revenue ramp of the top AI labs led to a revision in models. Anthropic and OpenAI together reportedly reached a $100 billion ARR run rate. This is way ahead of their internal projections published later last year. Total AI revenue excluding China has surpassed capex depreciation decisively:

Let’s do some rough math to understand where AI capex turns ROI positive, shall we?

Assuming 8% cost of capital, 30% operating margin and 5 years of depreciation, hyperscaler capex turns positive roughly at 1.7-1.8x revenue/D&A.

According to the data above, we are currently around 1.2x. This is pretty promising given that only around 3-4% of the world population are currently paying for AI. If this number reaches just 7-8% over the next few years, it’ll be more than revenues to justify capex.

Latest Bloomberg reporting also corroborates this:

Consensus analyst estimates also imply that AI revenues will start generating net ROI from 2028 on, as hyperscaler FCF is estimated to explode post-2027 even though capex will also keep climbing:

In short, one of the primary reasons that depressed the stock was the uncertainty over the ROI on AI capex. We now see a clear path to positive ROI as AI revenue growth has decisively outpaced the D&A growth for the first time since the beginning of this investment cycle.

Once AI investments start being accretive to earnings, we’ll likely see a substantial multiple expansion for all hyperscalers. When will the market do this pricing? Nobody can know. Could be three months from now or could be next year. But given the growth rate of AI revenues, it looks inevitable.

3️⃣ Software Pricing Model Will Change

The software pricing model has changed a few times since the invention of computers. Earlier, in the 1950s and 1960s, software came free with a mainframe, which is why a “software company” was an oxymoron.

In the 1970s and 1980s, enterprise software was priced per computer as computers were wildly different in power. Mainframe software came to be priced in MIPS, literally millions of instructions per second.

From the 1980s, pricing has shifted to per seat. And per-seat pricing shifted from perpetual licenses that led to bumpy sales to a subscription model in the cloud era, which made the model like annuities and sent the operating margins above 40%.

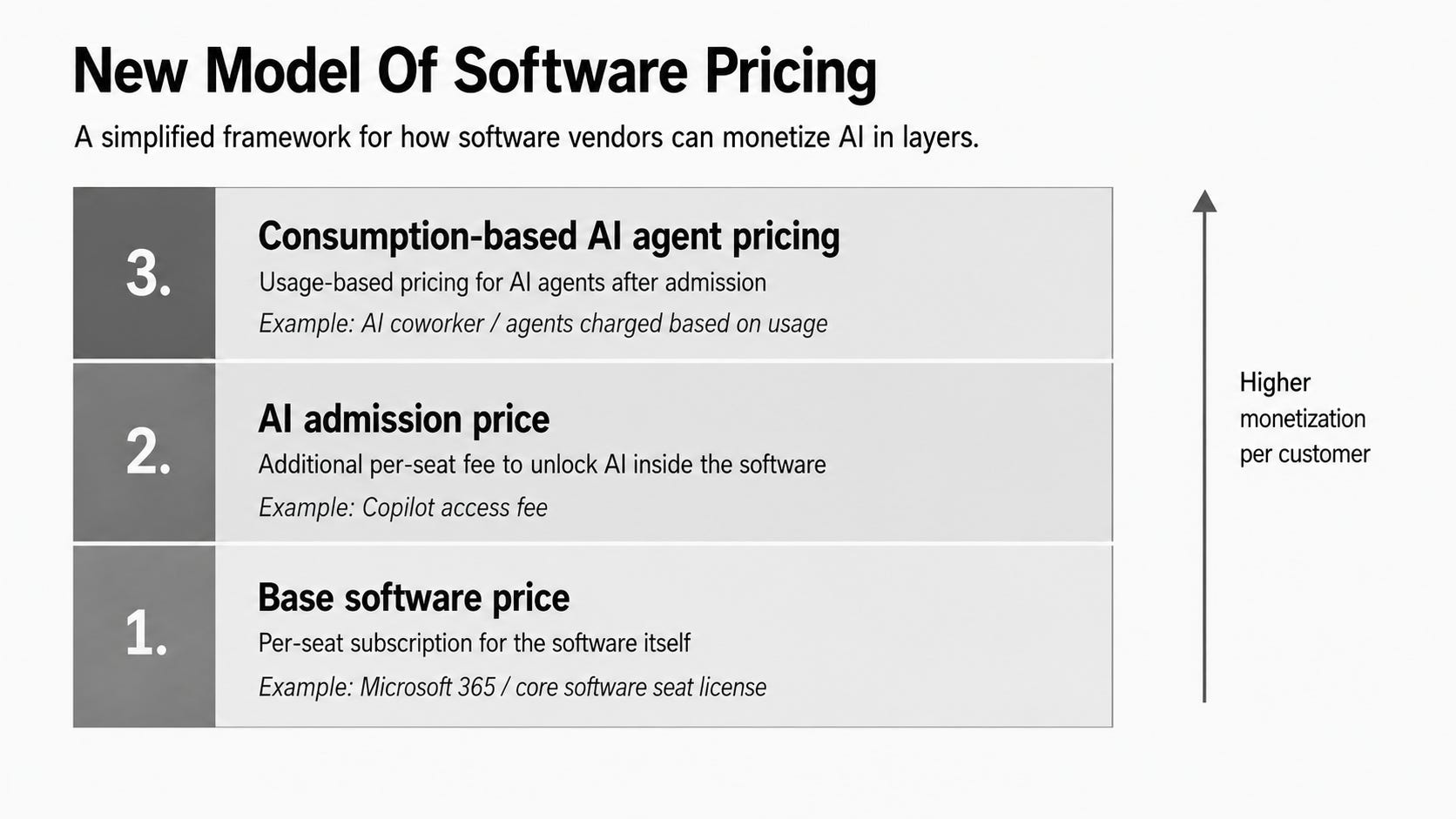

In the AI era, software pricing will change once again as AI agents will become the main forces of knowledge work and humans will act like orchestrators.

This enables essential software operators to create three-layered pricing:

Base price per seat for the software itself

Admission price per seat to use AI in the software

Consumption-based usage of AI agents after admission

We are already seeing this as Microsoft has started to push through this model already. They are currently charging extra to unlock Copilot in Microsoft Software. This is required to use Copilot Cowork, which is agentic AI that can work across Microsoft apps and deliver the end product. Cowork pricing, however, is consumption-based.

This will be a significant driver of both software and AI revenues. Microsoft currently has over 450 million commercial Office/M365 customers, and only around 20 million of them are paying for Copilot, which is around 3-4%.

There could be two counterarguments here.

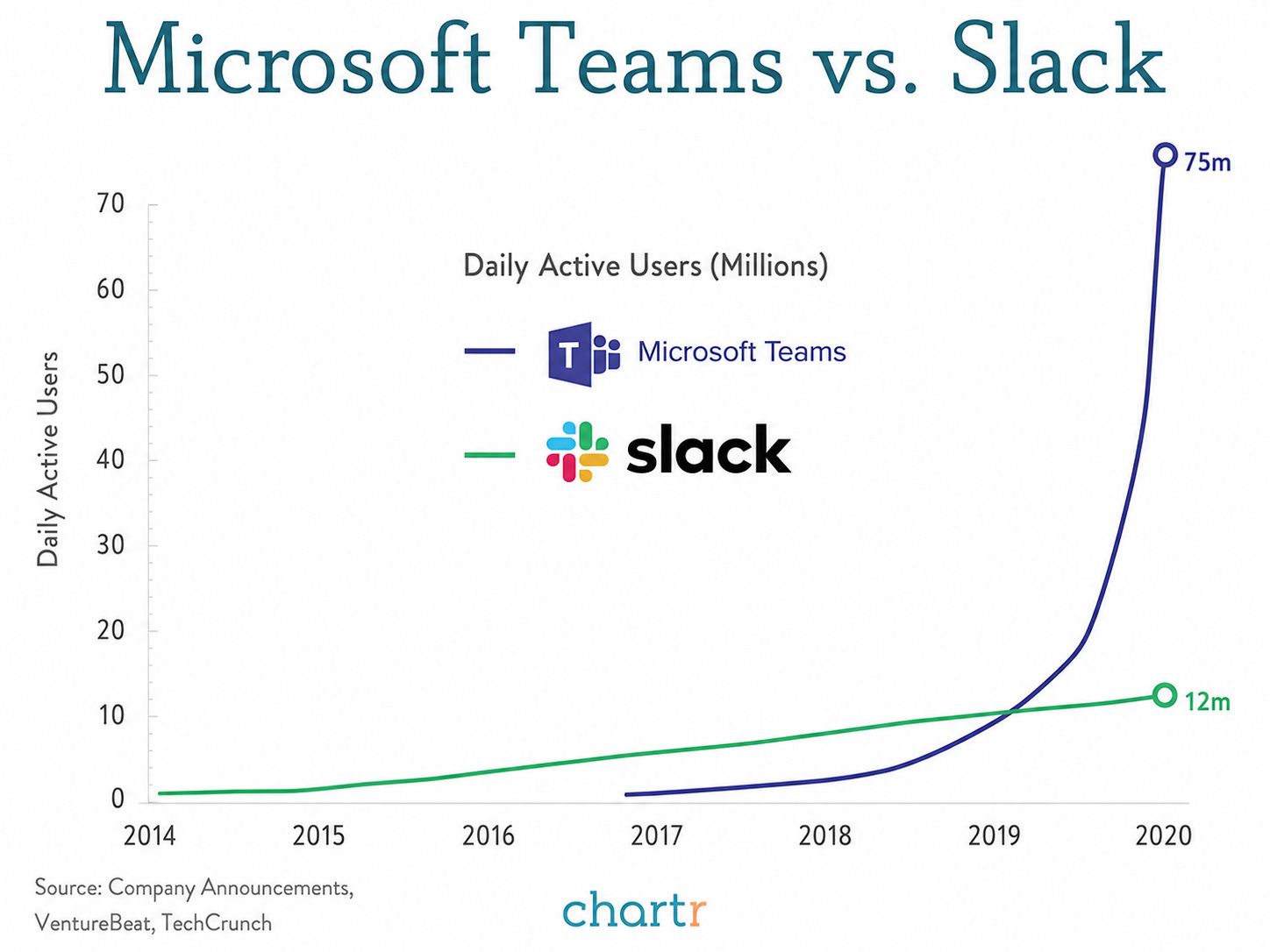

First, I see some people think integration of third-party LLMs like Claude would work better than Microsoft’s own implementation so people won’t buy Copilot. Those who argue this simply don’t know the history of platform leveraging in tech. Microsoft Teams is a recent example.

It was launched after Slack, and the user experience was way inferior. But it has overtaken Slack in just three years, as distribution is always the king:

Microsoft will surely leverage this and can make the user experience better than all other competitors, as we are talking about an application that sits on its own platform.

Second, some people argue Copilot AI is inferior to others. It was, but Microsoft solved this by making Copilot in the form of a model aggregator. You can pick from Claude and ChatGPT models depending on the task. Microsoft will still likely have positive margins here as consumption will flow through Azure.

As a result, Microsoft software and licenses revenue can even accelerate while contributing to AI revenues at the same time.

So, in short, Microsoft has ample growth opportunities going forward. It’s very well positioned to be one of the biggest winners of the AI boom, while its software business can still keep growing thanks to its position as the default medium of knowledge and changes in pricing structure forced by AI.

As we established durability and optionalities that should be reflected in valuation, we should see whether there are any red flags in fundamentals before creating the valuation model.

📊 Fundamental Analysis

➡️ Business Performance

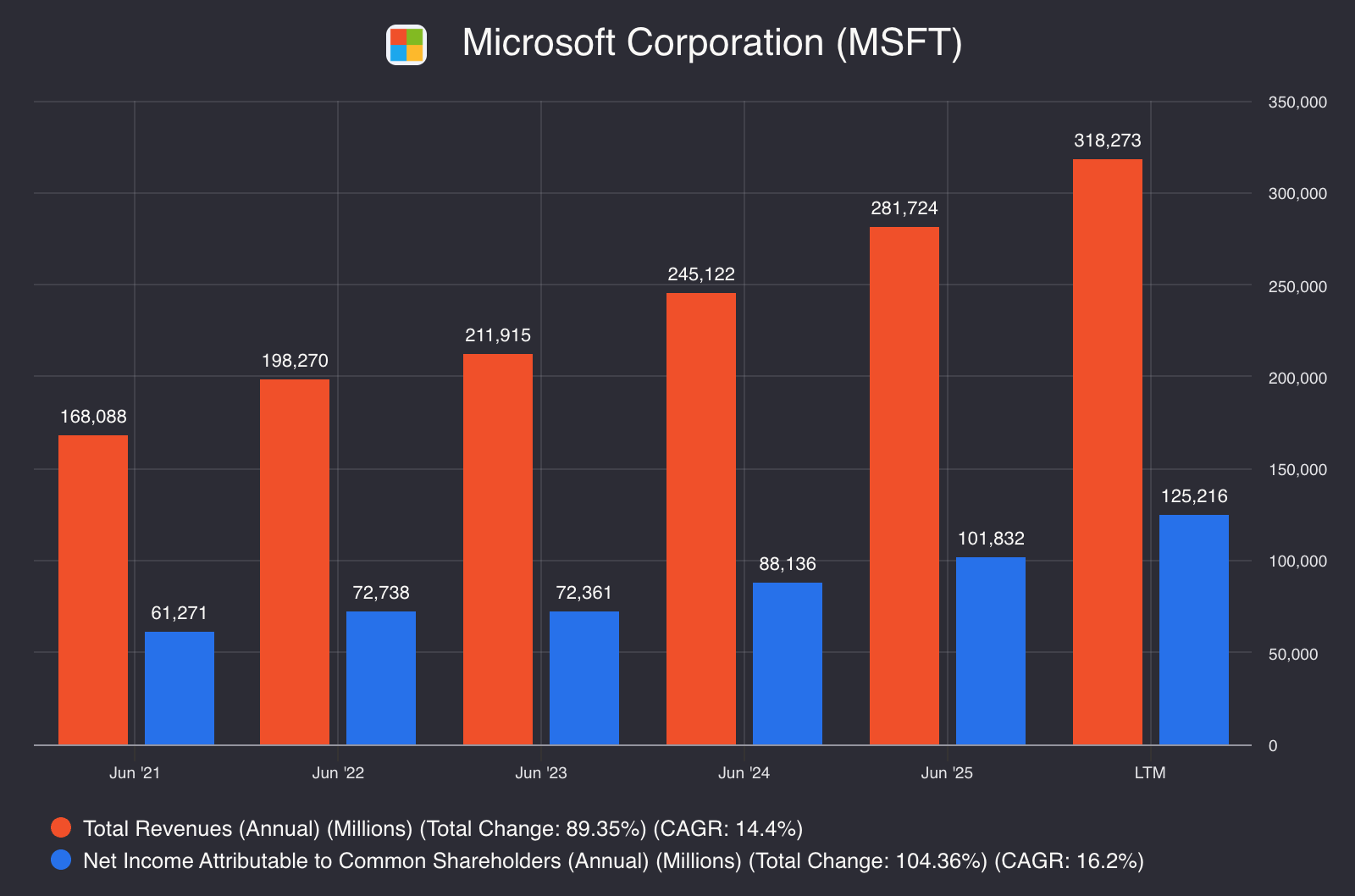

Well, there is nothing much to say for Microsoft’s past performance. It’s a rare event, and one of the most powerful forces in the history of business.

We are looking at a $3 trillion company that is 50 years old and still growing like a young-growth company:

What’s even better than this is the underlying transformation of Microsoft’s business, which illustrates its spawning ability.

In 2023, it generated a total of $212 billion in revenues. This has grown to $318 billion over the last twelve months, meaning it added $106 billion in revenues since then. The cloud division was responsible for 51% of this growth, as it grew from $73 billion in revenues in 2023 to $128 billion over the last twelve months.

For Google and Amazon, only 27% of their total growth came from cloud in the same period, meaning Microsoft is ahead of others in shifting its core business to AI.

We are looking at a 50-year-old company that still managed to position itself as one of the pioneers of an emerging revolutionary technology and derives substantial growth from it. I can’t imagine a better scenario for a 50-year-old, $3 trillion company.

➡️ Financial Position

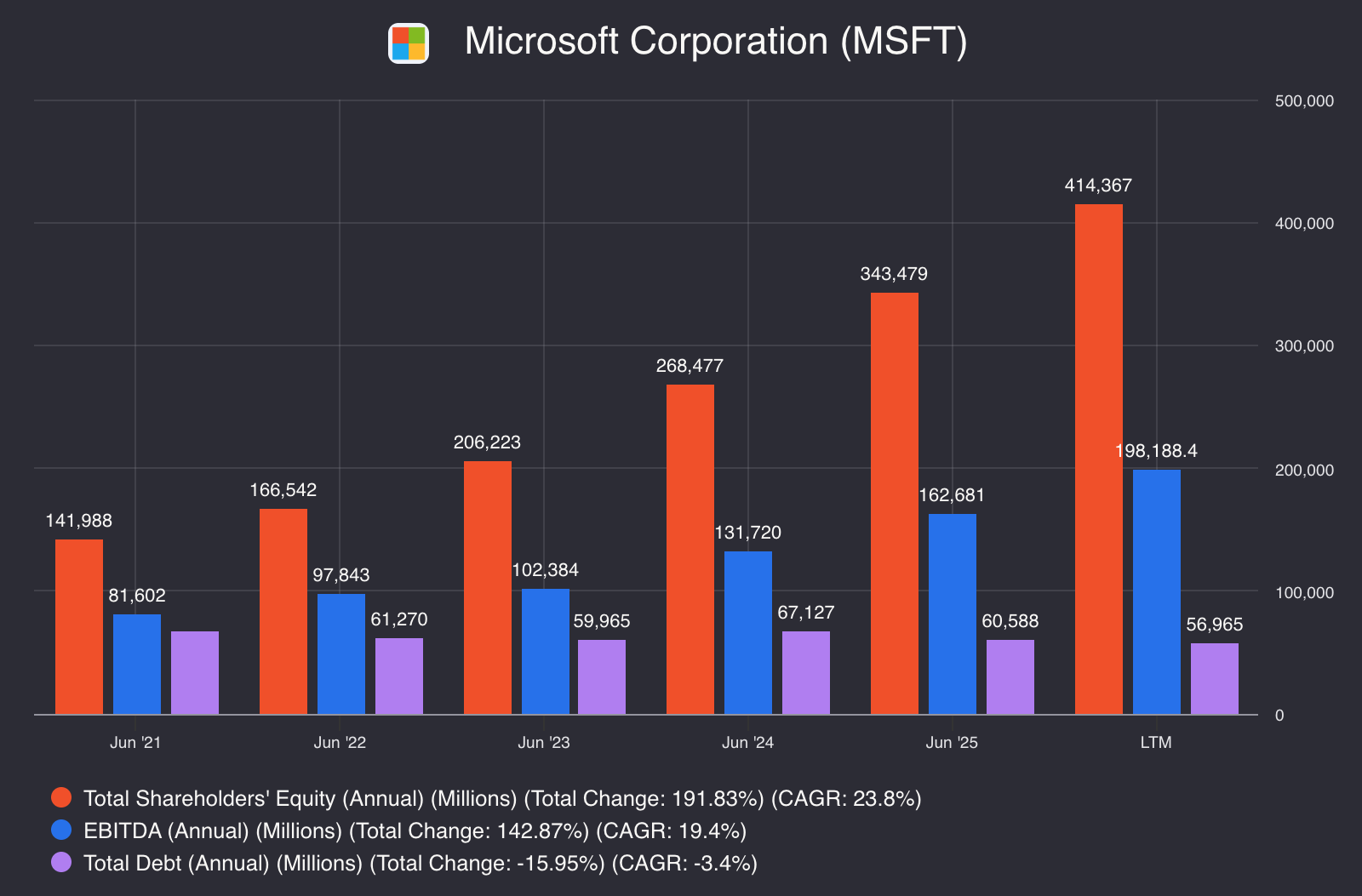

If there was something like a gold standard of financial health, it would be a perfect declining line through total equity, EBITDA, and total debt.

Microsoft has it:

Thanks to its gigantic cash flows, it doesn’t need to utilize much debt in its operations. This is the most important thing for public shareholders, as it eliminates the possibility of permanent loss of capital.

This means, in the worst-case scenario where AI capex goes completely trash, all Microsoft is losing is a few years of cash flows, which doesn’t detract much from terminal value, as we already established the durability of the business.

This part doesn’t require much further deliberation. It’s one of the strongest companies in the world and will remain so.

➡️ Capital Allocation & Profitability

⏺️ Margin Profile

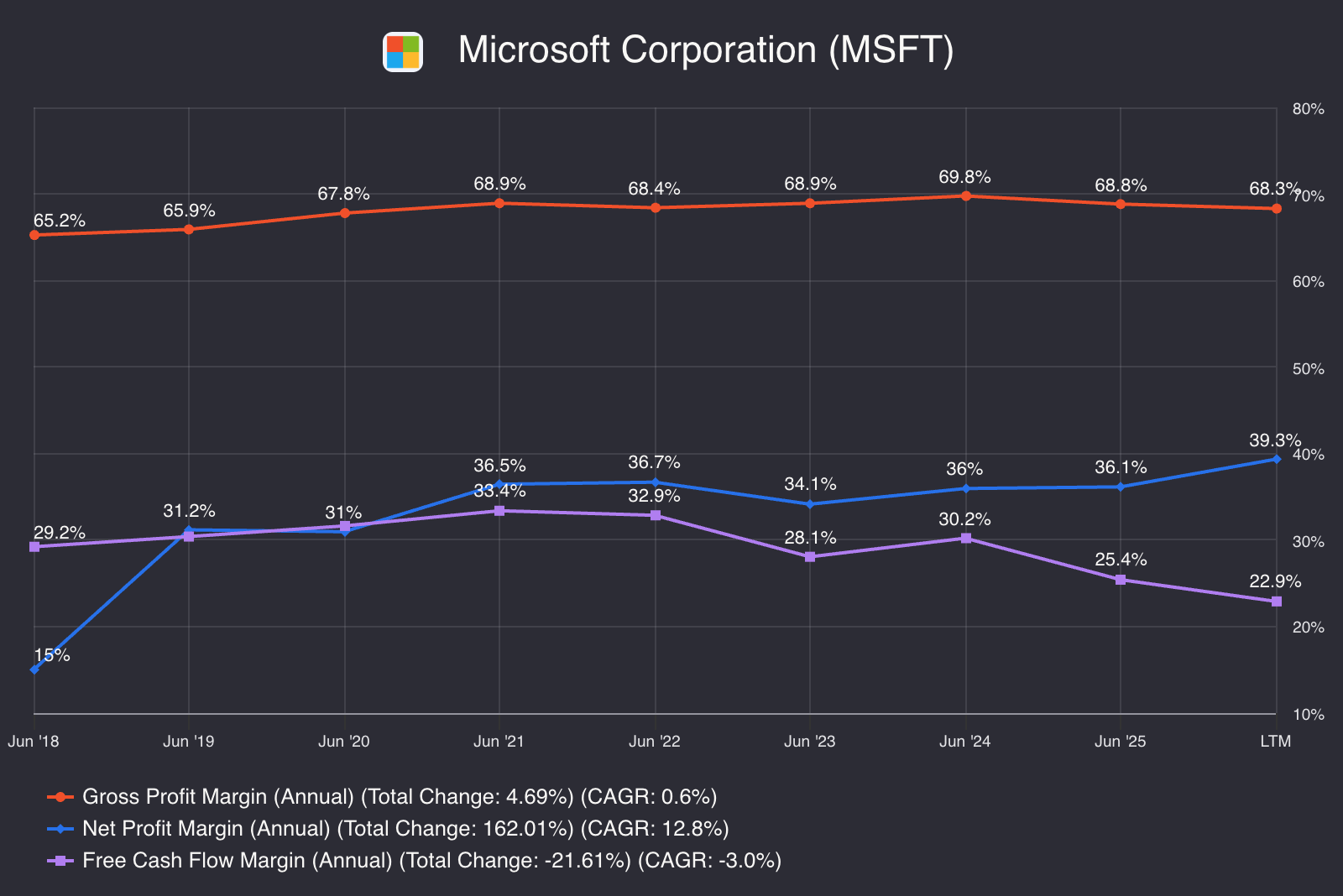

Throw gross, net, and free cash flow margins of Microsoft onto the same chart, and you’ll clearly see why it’s an amazing investment.

Look at the gross margins first.

Microsoft’s gross margins have been exceptionally stable since 2018. More importantly, gross margin is now exactly where it was in 2022 before the launch of ChatGPT, which means AI has not affected its software business at all.

Net margins, on the other hand, substantially expanded in the same period, from 31% in 2019 to 39% over the last twelve months. Considered in relation to stable gross margins, this shows its incredible operating leverage.

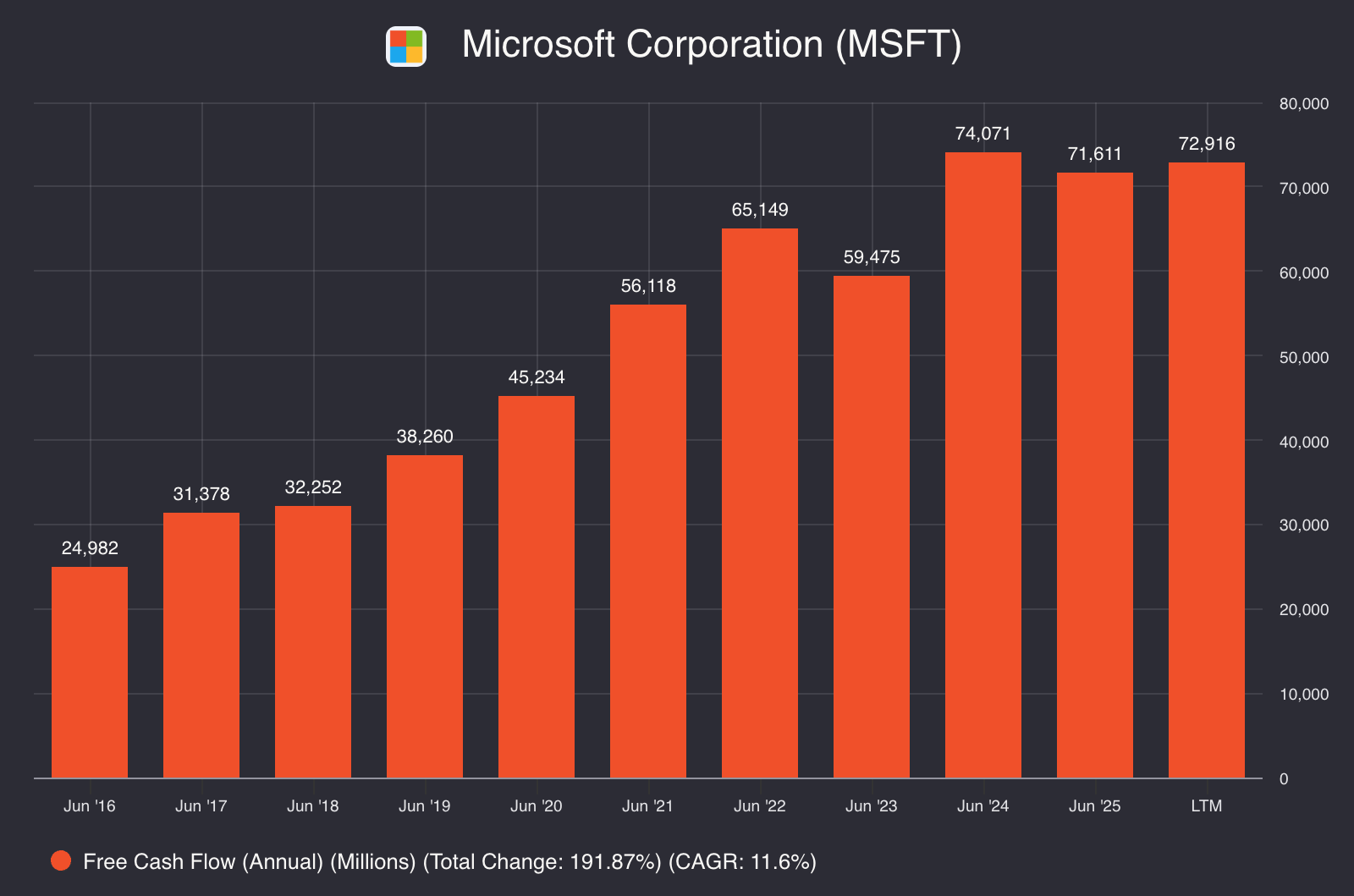

Plus, as you see, despite heavy AI spending, Microsoft's free cash flow margin is still above 22%, making the case that Microsoft is not drowning in sunk AI costs.

Finally, looking at gross and net margins together also refutes a bearish argument that’s taken off lately. AI bears make the case that cloud infrastructure economics get mega-cap tech companies closer to capex-heavy industrials than capex-light tech businesses. Microsoft’s gross margin has remained stable since 2022, and net income margin expanded, which clearly refutes this argument.

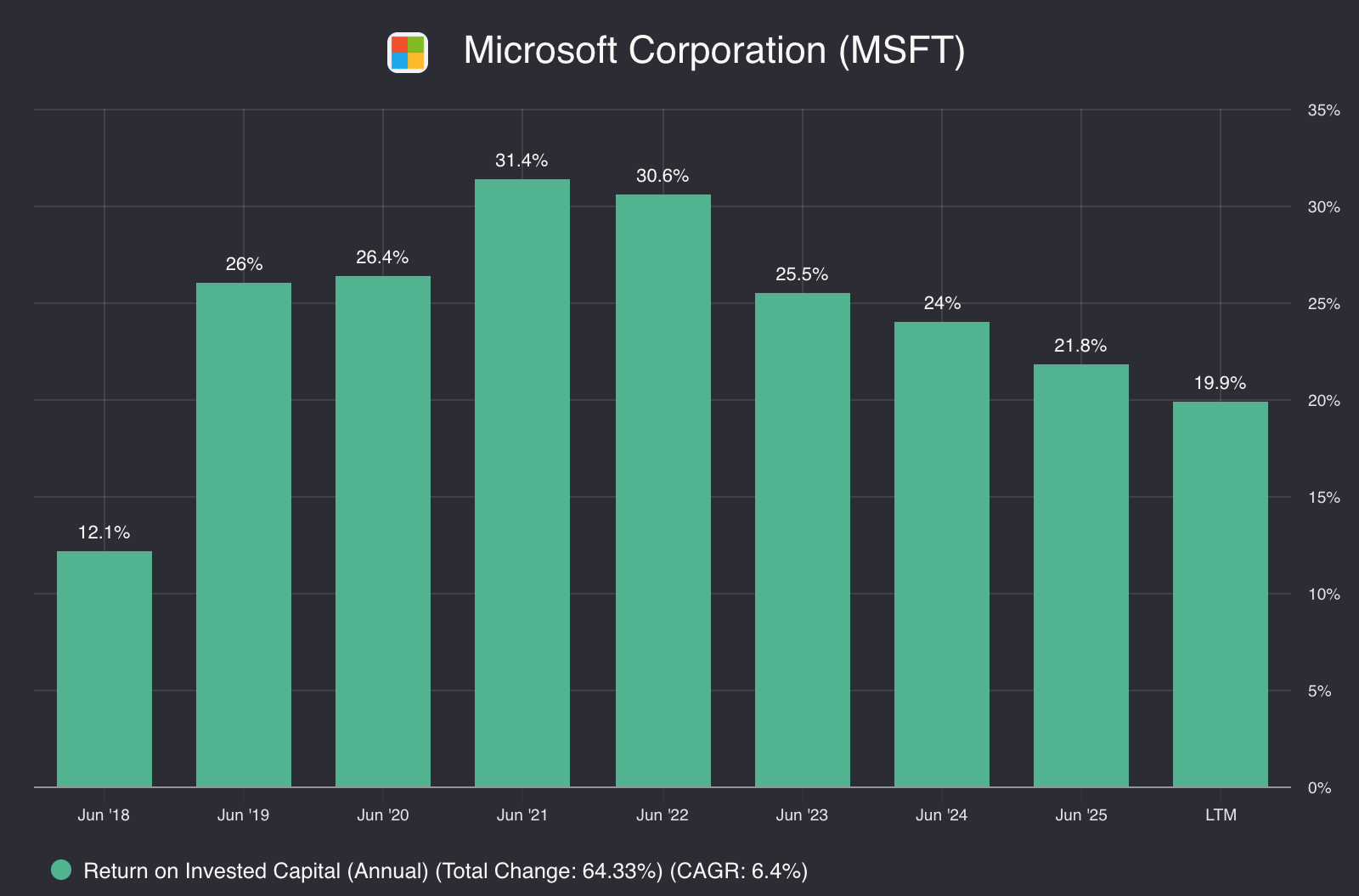

⏺️ Return on Invested Capital (ROIC)

Microsoft’s ROIC remains at an elite level despite heavy AI infrastructure capex, which comes with ~18 months of lag between cash out and first revenue.

We clearly see this as Microsoft’s ROIC peaked in 2022 before the ChatGPT release and has steadily declined since then. If you know what happened with AWS, this doesn’t stress you.

Amazon got heavy criticism for absorbing huge AWS costs between 2011-2014, where stock appreciated only by 50%. Then it unveiled +25% operating margins in the cloud business in 2015, and the stock made 3x by 2017.

We’ll likely follow the same path with AI infrastructure capex as well. Microsoft’s ROIC will likely dip in 2027-2028 as the 2024-2026 capex ramp will hit, but then recover as we experienced with AWS.

In the meantime, Microsoft will get heavy criticism for investing large sums in a business that compresses ROIC; however, you should note that there is not much of an alternative. These are giant businesses and opportunities to deploy hundreds of billions in capex at a higher ROIC than WACC don’t come every day.

Alternatives for these businesses have been buybacks, which are less accretive for shareholders than even below-par ROIC, as stocks of these companies generally trade at a premium and buybacks themselves also tend to increase that premium. So, in most cases, they end up overpaying for own shares, which isn’t accretive to shareholder value over the long term.

So, Microsoft didn’t have any other opportunity but to go all in on AI infrastructure, and it’s going well so far.

Summing up—Microsoft’s financial position is rock solid.

The business has been performing at an elite level, the balance sheet is one of the strongest on earth, if not the strongest, margins clearly illustrate it’s not getting inferior economics from AI infrastructure, and ROIC is still well above satisfactory.

It’s as good as it gets. So, only one question left—is the valuation right?

📈 Valuation

As I have said above, the most important thing in investing is minimizing the permanent loss of capital. This is why margin of safety is a central concept.

It’s primarily applied in three layers:

First by picking a business with high durability.

The second layer is keeping future assumptions conservative.

The third layer is demanding a price below what even conservative assumptions suggest.

With Microsoft, we established the durability part and future optionality. The mistake many investors make is incorporating the optionality as accelerated growth beyond the baselines, which rarely works well.

In Microsoft’s situation, it could be justified to assume acceleration in growth given the potential of AI. Analysts project its cloud division can generate +$800 billion in revenue in 2030.

However, it’s already a $3 trillion company, so I wouldn’t project much acceleration from here to be conservative. Instead, I think optionality will reflect itself by extending the current growth period.

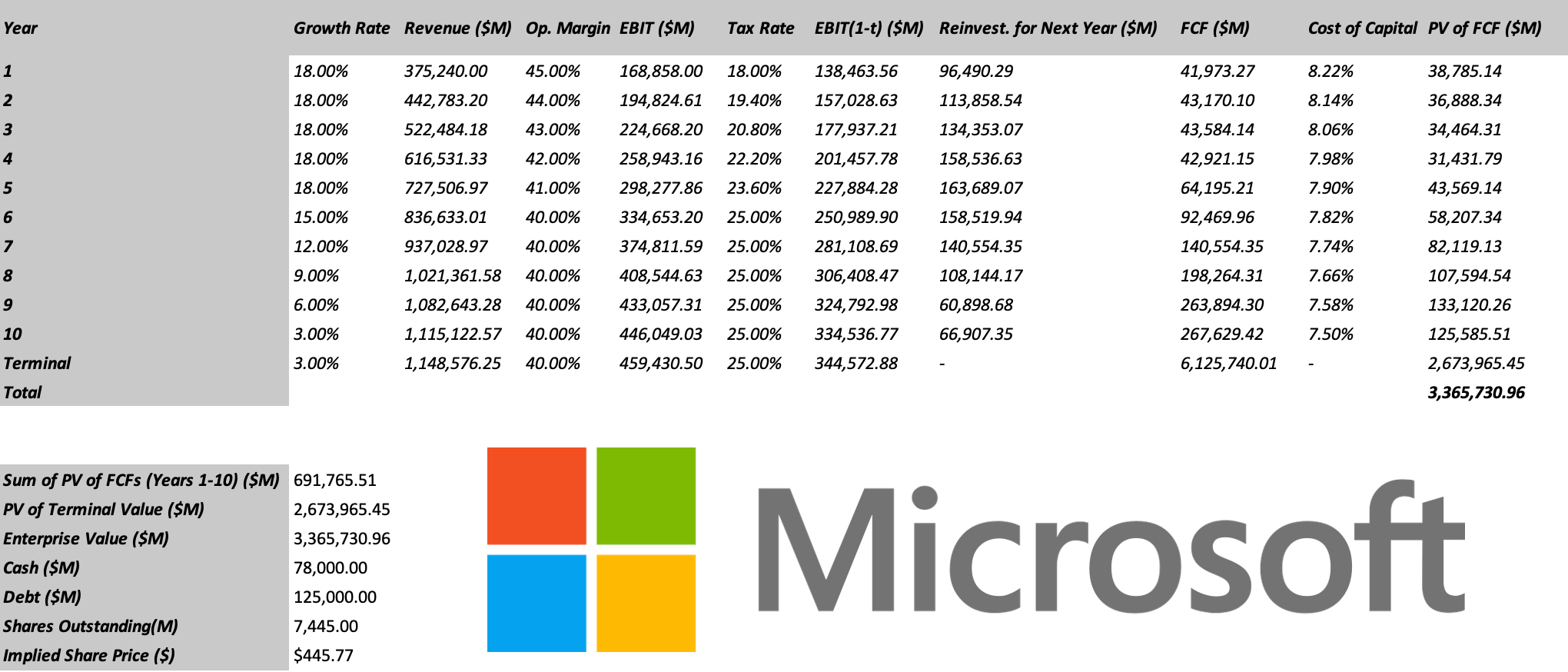

Here is what I would conservatively assume:

Its TTM growth rate is 18%. I assume 18% annual growth for the next 5 years, which then gradually converges to 3% in the 5 years after that.

The effective tax rate is currently around 18%; I assume the marginal tax rate will be 25%.

Operating margin will decline from 40% to 45% as cloud makes up more of the company.

Cost of capital will decline from 8.3% now to 7.5% in maturity, which is the average of mature companies in the US.

Terminal ROIC will be 15%.

Here is what this gives us:

As you see, even based on very conservative assumptions that price no acceleration in growth despite opportunities ahead, we end up with $445 per share fair value for Microsoft. The stock is currently trading at $390 per share, implying a 13% discount to the share value.

I would easily buy Microsoft even if it was only fairly valued, which makes the current price a no-brainer for me.

🏁 Conclusion

Exceptional companies tend to stay exceptional, and bad companies tend to stay bad.

This is why when there are discussions about potential deterioration of an exceptional business, you can find the best long-term opportunities.

Microsoft has been depressed by such discussions for some time now. However, if you really understand the model and go deeper to understand what actually makes Microsoft’s moat, you’ll see that it’s as strong as ever and possibly getting stronger, as it’s well positioned as one of the top beneficiaries of the AI revolution.

Sooner or later, the market will see this as well and re-rate the stock.

Meanwhile, we are getting an opportunity to buy one of the best companies in the world at a nice discount to fair value.

As I explained above, its software business is as strong as ever and will likely make even another jump in growth thanks to the changing pricing model of software. AI infrastructure business is already generating the bulk of the growth and will likely keep accelerating here over the next few quarters.

I am a buyer here.

Will make it one of my foundational positions next week if the price doesn’t suddenly jump before I can buy at the current levels.

Remember, investing is as simple as buying exceptional businesses at fair value. If you can catch them at a discount, even better. This is the case for Microsoft now.