History of Economic Bubbles and Lessons for Investors Riding the Hype (Part-1)

History of Economic Bubbles and Lessons for Investors Riding the Hype (Part-1)

Most of the catastrophes and devastating events in the history wouldn't occur if it wasn't for the envy and greed of the mankind.

“You must have controlled greed to get rich.” says Warren Buffett, the greatest investor of all time.

What is striking about this sentence is that he puts the emphasis on control not greed. As a wise man, he knows uncontrolled greed leads to destruction more often than controlled greed leads to wealth. This is not a new phenomenon, we have seen uncontrolled greed of mankind leading to destructive situations throughout the history: Wars, crisis, environmental disasters… Economic bubbles are one of these disasters that often struck societies after a period of uncontrolled greed.

Today, we are going to dive into the four great economic bubbles in close history and try to extrapolate lessons for today’s investors.

1. Tulip Mania (1634-1637)

In Holland, Tulip was traditionally traded in the summer months just after the flower had bloomed in the June. After the blooming, the grover would then lift the Tulip bulbs off the soil, wrap it in dry papers and keep it indoors before replanting it in October. These months between June and October when bulbs were kept dry indoors were called as “dry bulb season”. This was the time when the prospective buyer first saw the blooming Tulip and paid for it. These contracts were immensely detailed as the grower would have to deliver the exact same Tulip that the buyer paid for. This was the traditional way of Tulip trade.

In early 1630s, the form of Tulip trade changed deeply. Instead of selling Tulips individually, growers started to sell Tulips by weight when they were still in soil in exchange of promissory notes. The weight was measured in asen which is 1/568 of an ounce. The contracts specified the current and expected weight of the Tulip at the time of delivery. Indeed, the magic word is “expected”. Soon, the traders figured out that Tulips could weigh, and most of the time would weigh, heavier than the expected weight on the promissory note and started trade those notes for a little premium, a futures market was created.

Soon after speculators came in the market and they paid hefty premiums for the notes spiking prices even higher. Those notes were now changing hands more than 5 times a week and a note for the delivery of a decent Tulip with average weight were selling for a full year’s salary of a carpenter or a decent house on the canal bank in Amsterdam. Growers never delivered the Tulips promised because nobody was going back and asking for a delivery. It wasn’t about having the best looking Tulip anymore, it was about making more money.

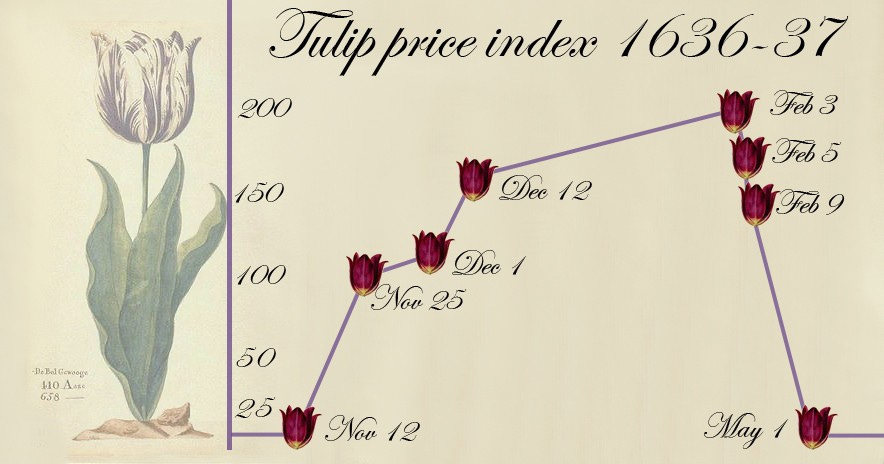

People were basically futures contracts with an expectation that they would always find somebody who would pay more. The connection between the price of notes and the value of underlying Tulips was long cut. The first irrational economic bubble of the modern history had emerged. People were finding somebody else to sell these contracts, until, they couldn’t.

Nobody knows how and when it started; nobody knows whether somebody just shouted “this is nonsense”, or some Tulip whale dumped all the contracts he had into the market but someday, prices started to go down. Rumor has it that one day, a trader in Haarlem couldn’t find any buyers for the contract and the rumor of this event spread fast within traders, plummeting Tulip contract prices.

Nobody knows the actual circumstances that burst the bubble but we know that one day people were trading mansions in Amsterdam in exchange of Tulip contracts and the next day nobody wanted it. Rumors went on to say that many Tulip traders committed suicide by jumping in canals because of the collapse and many growers burnt all the Tulips out of anger. We don’t know whether these really happened but we knew that people were selling their most valuable belongings to get their hands on these futures contracts and many people were devastated when one day they woke up and found out that their contracts were no longer worth a dime.

Lesson #1: Speculation in the Market is Destructive

Those people trading contracts didn’t even know they had invented futures contracts, a complex form of investing in assets. This was very dangerous as there was no safeguards that could protect uninitiated people from vast amount of losses. They probably thought they were just playing with an innocent instrument used to exchange Tulip’s even when they were still on the ground.

Today, there are significant safeguards to trade future contracts in the regulated capital markets. You can’t just go to your broker and ask to buy some features contracts. They will ask you questions to verify that you are aware of the risks, you can afford to lose in the trade and beyond all, you know what you are dealing with. None of these were present at the time of Tulip mania.

People were not buying the underlying asset, they were buying the promise of making quick money. If they were buying the physical asset, Tulip, they would have asked way sooner whether what they paid was worth what they get. Imagine, would you accept to trade your house for a Tulip bulb? Indeed. Now let’s change the question. Would you sell your home and buy futures contract only to double your initial investment and get even bigger mansion in no time? Now factor in the fact that everybody doing this was making fortunes on it. It’s now more likely right?

You should never trade complex instruments that you don’t know. Why? Because there is some genius in the market who will make money on your ignorance. In this case, market is just a mechanism that takes the money from ignorant and gives it to knowledgable. Always ask what is the underlying instrument worth? If those people could look beyond the notes and ask whether a Tulip was worth their houses, most of them would probably have avoid those trades.

2. South Sea Company Bubble

The Great Britain fighting two wars simultaneously in the early 1710s: Spanish Succession War and Great Northern War. The economic stress of two wars was apparent on the British Government which was constantly issuing new national debt to finance the wars. In 1710, national debt reached to unsustainable levels and British Government formed a special committee to address the issue.

General picture was grim. Government owed 9 million pounds without no specifically allocated resource to pay it. Financiers and bankers came up with a scheme to consolidate Britain’s national debt. According to the scheme, they wound a company and mandate holders of national debt to surrender these debt certificates to the company in exchange of the company stock. Later, government would issue a monopoly in slave trade between Africa and South America and would make fixed payments to the company to finance its operations and the company would distribute earnings to its stockholders. That was a great way to consolidate national debt and attracted much interest from the public. After all, who doesn’t want to exchange his junk bonds for hefty dividend payments?

Excitement around the scheme increased even more when Britain obtained monopoly, as a part of Treaty of Utrecht, to supply African slaves to Spanish America. It was certain that the company would make a lot of money after all it wouldn’t have any competitors. However, the things didn’t go as planned. The Company faced with significant hurdles supplying slaves to Spanish America as most of the governors didn’t buy slaves from South Sea and it was forced to sell slaves for loss in the West Indies.

For a long time though, nobody noticed what was happening as it was extremely hard to understand financed of the South Sea company. It had two main operations: Financing and trade. Its financing operations were much like a bank. It was buying national debt in exchange of stocks below par value because there was huge excitement around the company and expectation was that the stock would become much more valuable in the future due to the monopoly the company had and thus people thought buying stocks below par value was better than holding the national debt. See what is happening here? The company was doing arbitrage operations in its own stock. If you do that for 5 times, you create an excess value of 100 pounds for which you can issue another stock on par value of 100 dollars. If you can repeat this forever, you can make infinite money.

These arcane financing operations were hiding the losses of the company and driving the stock price to new highs day after day. It was much like early Enron case. However, none of these operations can last forever. Earlier or later, people run on the banks only to find the bank is empty.

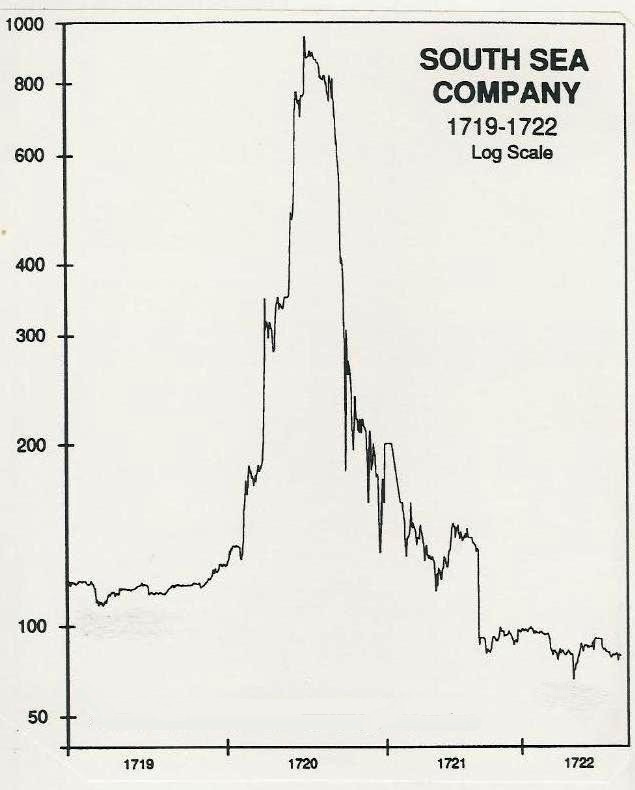

By the end of April 1720, stock was selling at almost £350, then nearly £600 by the end of May, and £950 by the end of June. The overinflated share prices then peaked at around £1050, before suddenly dropping to £190 (below their original value) in the late summer, and then dipping even further to £124 in December 1720. The South Sea Bubble had well and truly burst.

Lesson #2: If you don’t know valuing a business, don’t pick stocks.

South Sea scheme was genius. Nothing was wrong by design, the plot was simple: It would take the government debt and government would finance its operations in exchange and it would make immense amount of money by capitalizing on its monopoly position and would pay its shareholders hefty dividends.

What could go wrong? It was certain that it would make a lot of money because it didn’t have any competitors by design. You can make infinite money if demand is constant and you don’t have any competitors. The problem is design rarely works the way it was supposed to work. Business is full of ups and downs and this is why what makes money is execution, not expectation.

If investors knew how to value South Sea Company, they wouldn’t pay those premiums they paid. The problem was they didn’t know how to value it. As Warren Buffett says every investment decision, in the end, is a value decision, even growth is a factor that effects the value, nothing else. You need to know three things to value the company:

How it makes money

How much it makes per year

How stable the earnings are

Then valuation is simple. You should calculate how much money the company is expected to make in the next ten years and then figure out how much you are willing to pay now for all these future earnings. This simple. If you can’t see how the company makes money, you can’t estimate how much money it will make and can’t know what is your acceptable buying price.

I can understand how Dunkin makes money: By selling donuts and coffee. Then I ask how many donuts it sold last year? How many more donuts it sold last year than the previous year? How many donuts it can sell next year? What is the average price? Multiply the price with number of donuts I expect it to sell. That’s it.

I don’t know how Palo Alto Networks make money. I know it provides cybersecurity services but I don’t know how these services are valued, where is the demand, what are threats to the business? I can’t foresee it.

Now what you own and why you own it. Remember, risk doesn’t come from volatility, it comes from not knowing what you own.

3. 1929 Stock Market Crash

There is a reason why 1920s is called “Roaring 20s.” US had emerged one of the big winners of the World War I and it was generously exploiting the benefits of being a winner.

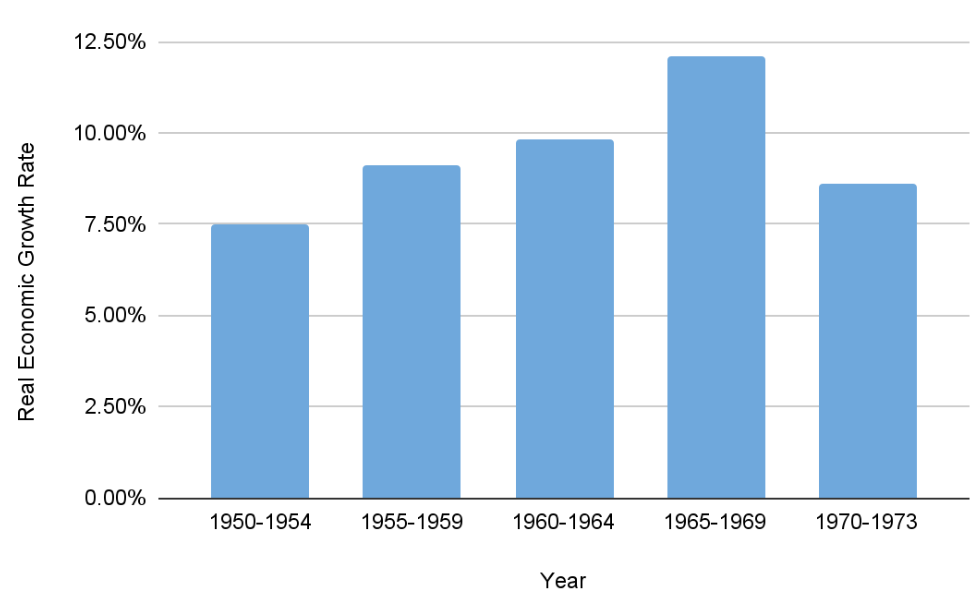

US economy was booming, it grew 4.2% annually from 1920 to 1929. It was the era of major industrial and technological developments that resulted in significant development in welfare and enhancement in living standards. There is a rapid adoption of the automobile to the detriment of passenger rail travel. Though suburbs had been growing since the late nineteenth century their growth had been tied to rail or trolley access and this was limited to the largest cities. The flexibility of car access changed this and the growth of suburbs began to accelerate. The demands of trucks and cars led to a rapid growth in the construction of all-weather surfaced roads to facilitate their movement. The rapidly expanding electric utility networks led to new consumer appliances and new types of lighting and heating for homes and businesses. The introduction of the radio, radio stations, and commercial radio networks began to break up rural isolation, as did the expansion of local and long-distance telephone communications. Recreational activities such as traveling, going to movies, and professional sports became major businesses. The period saw major innovations in business organization and manufacturing technology. The Federal Reserve System first tested its powers and the United States moved to a dominant position in international trade and global business.

Result? The stock market was booming. Companies like Ford and General Electrics were the drivers of the economic growth and rapid change in the society. As the new technologies were spreading across the US, productivity was increasing and in turn re-fueling the innovation and economic growth, creating a self-sustaining cycle of economic machine. This rapid development was taking stocks to daily all time highs. SP Composite Index (predecessor of SP 500) increased 20% annually from 1920 to 1929. This was and remained an unprecedented bull-run.

As the stock market seemed invincible, more and more people were attracted to stocks. At first, it was only reserved to initiated but economic boom created large amount of surplus capital and capitalists put that capital in work in the market. Stock market looked invincible and ordinary people started to make money by just betting on symbols they don’t even know the meaning of. And guess what? They made money. Everybody was making money, more frightening everybody was making easy money.

If you can just make more money by putting money in the market why not to bet more money and make even more? It seemed plausible. Brokers started to offer stocks for 10% downpayment and the rest would be covered by the gains. Suddenly, ordinary people like the grocery store owner, carpenter, tailor was trading in the market at 10x leverage. Never a good thing.

The rumor has it, one day somebody shout “sell” on the maket floor and few people followed. Those who saw them started selling too which is perfectly normal. However, when they sold and stock market declined, brokers had to sell their leveraged holdings because they were collateralized against the stock. Suddenly, everybody started to sell and small investors that bought stocks on leverage didn’t just lose their gains, they lost their life savings. Those who saw them in this miserable position sold their holdings not to share same faith with them and that buying frenzy of roaring 20s turned into a selling frenzy.

It took 3 years for the market to dip. In 1932, it dipped at $41, 381% loss decline from 1929 high of $381.

Lesson #3: Leverage is Doubled Edged Sword, Don’t Use It.

Leverage wasn’t intended for the use of retail investors. Indeed, it’s a fundamental tool to use in finance but those who exploit it are usually bankers, financiers and corporations that undertake leveraged buyouts i.e buy assets by securing a loan against the value of the asset they are buying.

Perhaps the most well-known and common form os leverage is mortgage. It is essentially getting a loan secured by the property itsel. If you default on the loan, the bank forecloses the real estate and and tries to make up for its losses buying selling it or capitalizing on it by some other way. Taken to the extreme, leverage never plays well as we have seen in the 2008 crash.

What turns leverage into a gamble is that incalculability of short term developments. You may be right all the way about the long-term fundamentals and direction of the events but leverage mandates short term thinking. If you are leveraged 10x, 10% fluctuation in the market causes you to lose all your position. This is not a favorable risk/reward ratio for an intelligent investor.

If you are not a financier, banker or a corporation, you will be better off avoiding it.

4. Japanese Asset Bubble

Japanese economy today is a product of a miracle. In the post war period, Japanese economy grew on average 9% annually from 1955 to 1973, meaning size of economy doubled in every 8 years. This is by far the rapid economic growth in the modern history, may be only second to the rise of China after 1979. It didn’t stop here, Japanese economy grew at average annual rate of 4% until 1990. The period is known as the “Japanese Economic Miracle.” Miracle it was indeed, in just four decades, Japan went from a war-torn country to the second largest economy in the world.

The factories were working non-stop, Japanese people had long forgotten the meaning of unemployment, Japanese corporations were technological powerhouse. The country was epicenter of consumer electronics having invented the bestsellers like Atari, VHS, Walkman… It was well outperforming the US economies in memory chip production. Everything was great, until it wasn’t.

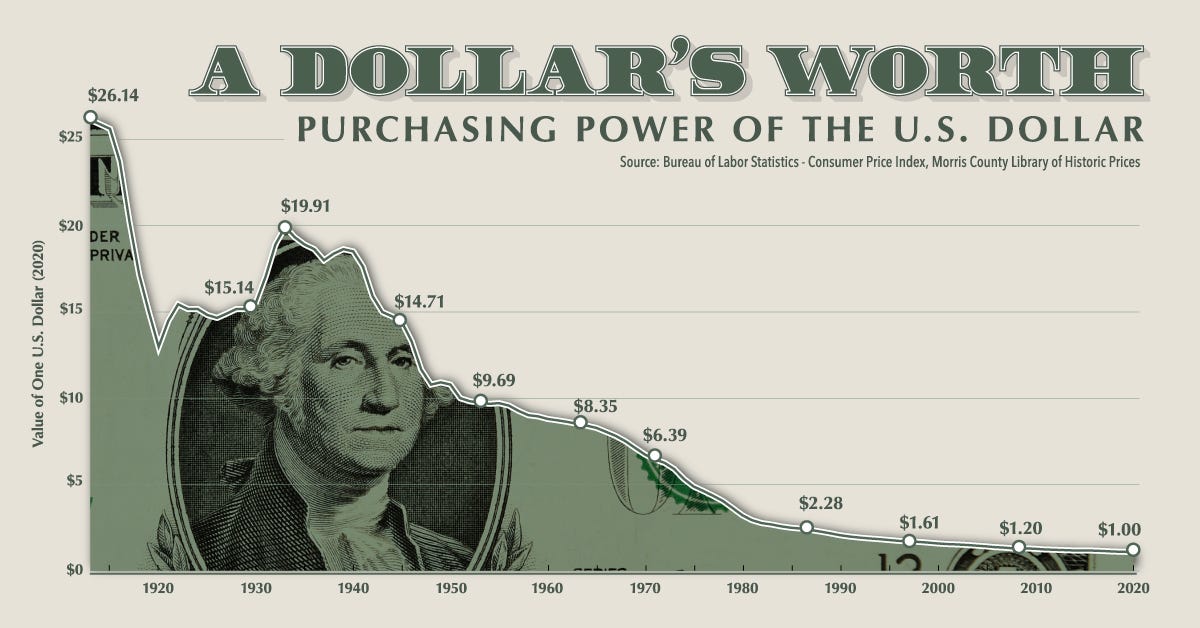

In the beginning of 1980s, US Dollar gained 50% value against other major currencies in the world, including Japanese Yen. This was catastrophic for the US, as exports had become amazingly expensive and their Japanese counterparts became equally cheap. Japan was major beneficiary but the US was bleeding. To stop this, US pressured for a meeting which led to a gathering of finance ministers of the 5 largest economies in the world in Plaza Hotel, New York known as Plaza Accord.

The outcome was simple: Devaluation of dollar.

In the following years, USD lost 50% of its value against Japanese Yen, putting strains on Japanese export machine. American exports became much cheaper while their Japanese counterparts became more and more expensive every passing month.

To counter these developments, Japanese Central Bank decided to do two things: Boost local consumption and and implement loose monetary policy to counter the devaluation of dollar. To implement this policy, interest rates were reduced by 50% in the following two years, government boosted consumption by loosening credit conditions applied by the public banks. Suddenly, everybody had access to money, a lot of money. This ignited a chain reaction: Japanese real estate prices started to increase so did their value as a collateral and thus people could borrow even more and the cycle went on and on.

Not just retailer investors was doing this, also corporations were involved in heavy buying. Accounting regulations allowed capital gains to be added to the bottom line at the time so corporations also closed massive real estate deals and bought local stocks and added their capital gains in their bottom line, further skyrocketing stock prices. In 1990, bubble had become unsustainable and burst, just like every other bubble before.

The magnitude of collapse was so great that it took 30 years for Japanese Stock market to recover and get back to 1990 levels. Many banks went bankrupt because they were so exposed to the real estate loans that they lost all the money when those properties collapsed in value. Many people had invested their life savings in the bubble and they ended up losing everything.

Lesson #4: What is Risky at Cheap Prices is Risker at Higher Price

There were many signs smart people of the time could understand the massive overvaluation and skyrocketing risk in the market. All the major stock indexes in the world was trading around 10-15 PE while Japanese Stock Market was trading at 60 PE without much change in corporate earnings.

When the prices inflate, risk necessarily increases regardless of whether it can be justified or not. When the prices go higher, you can withdraw and look for opportunities. Many do the same, they think the momentum will take the market even higher and they don’t want to give up what they see as a sure way to make some quick & easy bucks. Even if this proves to be the case in 90% of the time, as a rational investor you should still miss the chance rather than taking the risk. If you don’t see the chance you missed as money you lost, it will be way easier to do it. There are and will be infinite number of opportunities in the market, I guarantee you.

When looking today’s markets, I recommend you to take historical occurrences into account. History tends to replicate itself more often than you think. This is especially true for the markets. If we had drawn enough lessons from the first bubble, second would have never happened, yet it did and they will keep happening.

Try preserving your rationality at all costs. In the next part we will dive into dotcom bubble and 2008 global economic crisis, two of the most influential bubbles of our time.

Stay sane and invested!

Oguz-The X Capitalist