Google: Cracking Monopoly or a Thriving Ecosystem?

Google is depressed from many angles: ChatGPT, Antitrust investigations, employee relations etc... It's getting sold off, what should we do?

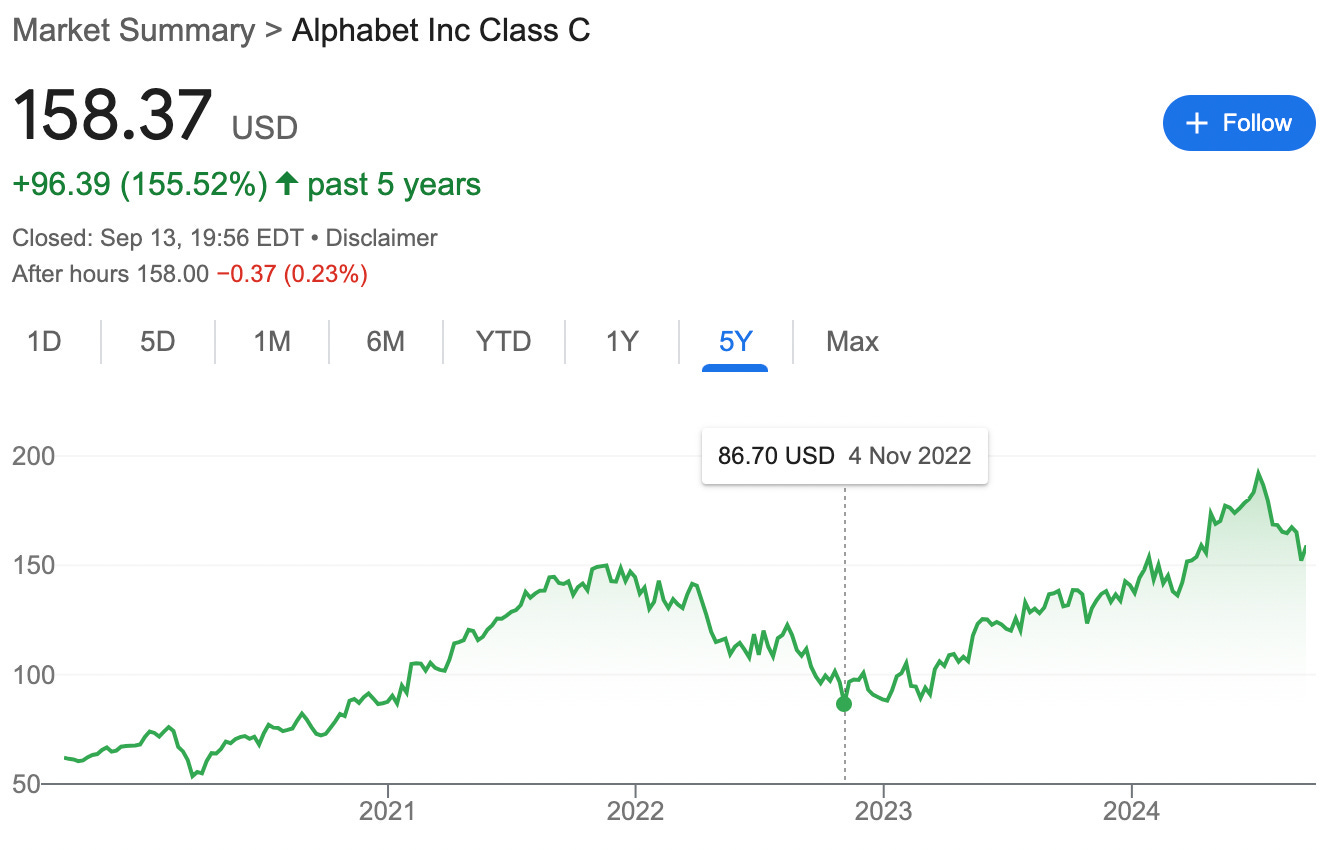

I am going to tell you something amazing. Just look at this chart 👇

See the dip in November 2022? This was a huge buying opportunity, yet many people missed it.

Even Bill Ackman started buying after this and now his average cost basis in Google is just below $100.