Finishing June: Our Portfolio Outperforms S&P 500 by 31%, Here Is What We Own!

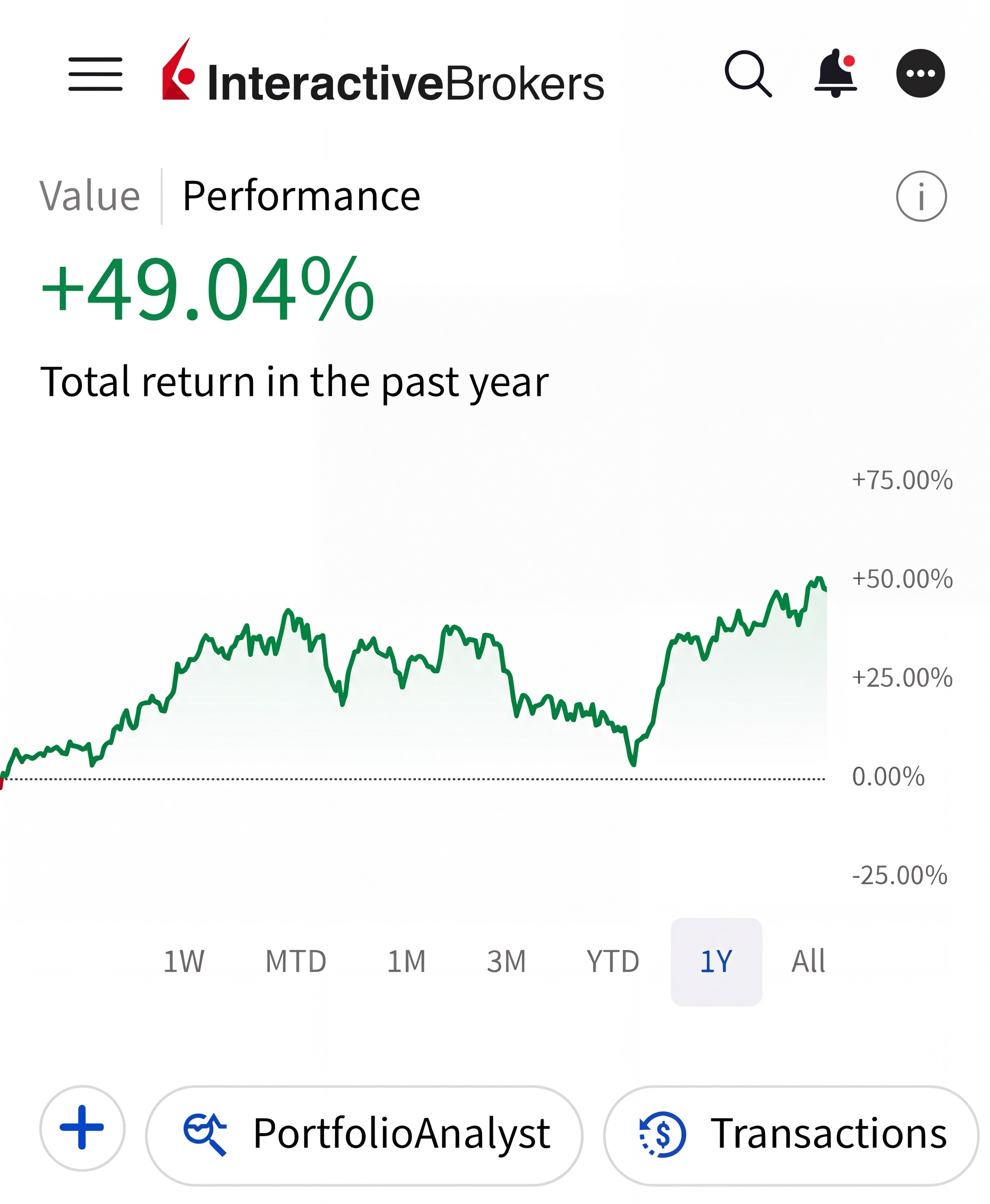

Portfolio is now up 49% over the last twelve months against 18% of the S&P 500!

💥Our portfolio is outperforming the market by 31%!

Portfolio is now up 49% over the last twelve months against 18% for the S&P 500!

There is something I need to do before I start talking about the portfolio.

I have received so many nice messages lately, as this month was nothing but pure alpha creation. It’s my duty to thank our members. They are not just readers; most of them are active contributors, and many of them are friends I can call by name.

The community has always been an integral part of our success, as it’s a medium where decisions and thoughts about the prospects and current positions mature. So, it’s my duty to give our great people credit here. They are not passive beneficiaries but active contributors to our performance. Once again, thank you all.

This has been a hard but amazing month for our portfolio.

Value reached its high-water mark while ytd performance remained stable around 21%, and TTM performance came at 49%. If our portfolio were an official fund, it would have outperformed all but one of the major Wall Street funds YTD:

Most people focus on the headline performance, and indeed our headline performance is great. However, what’s better for me is that the portfolio has behaved exactly as it was designed to. This is the most important thing for me as it shows our knack in controlling portfolio posture and positioning.

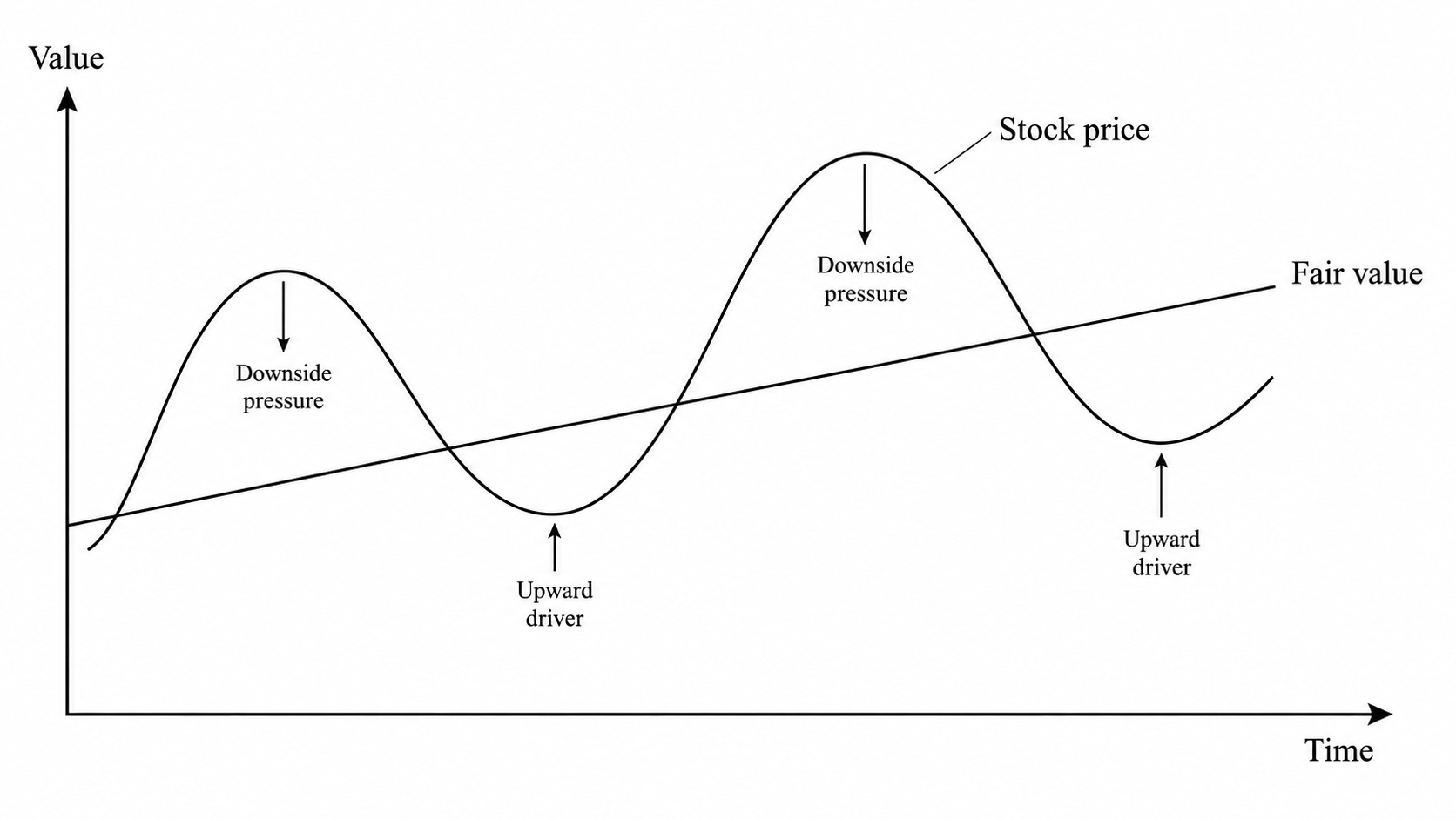

If you have been following this publication for a while, you know that one of the themes I talk most about is “base effects.” This is the biggest problem of high-performing portfolios like ours.

It’s very simple in principle.

When you buy an undervalued stock, and it reaches full value, it sets a high base. From there on, it’ll be harder for the stock to go up as mean reversion turns to downward pressure from upward driver. If you remain inert, you are more likely to see the price decline than rise. This happens as long as fair value, since it tends to be the mean in the long term, doesn’t rise faster than price in all periods:

The way to overcome this is portfolio turnover, i.e you dump/reduce fully valued stocks and buy new prospects instead that have room to go higher until they reach fair value.

Portfolio turnover comes as a natural urge to most investors. The problem is that most investors don’t want to tolerate intermittency in their performance. When they see their portfolio up 50%, they want to buy things that will go up fast and make that 50% to 60%. This is often what kills long-term returns.

The problem is that when the momentum becomes undeniable and easily observable, stock is often either about to reach full value or already beyond it. Thus, mean reversion has either already turned to downward pressure or is about to turn.

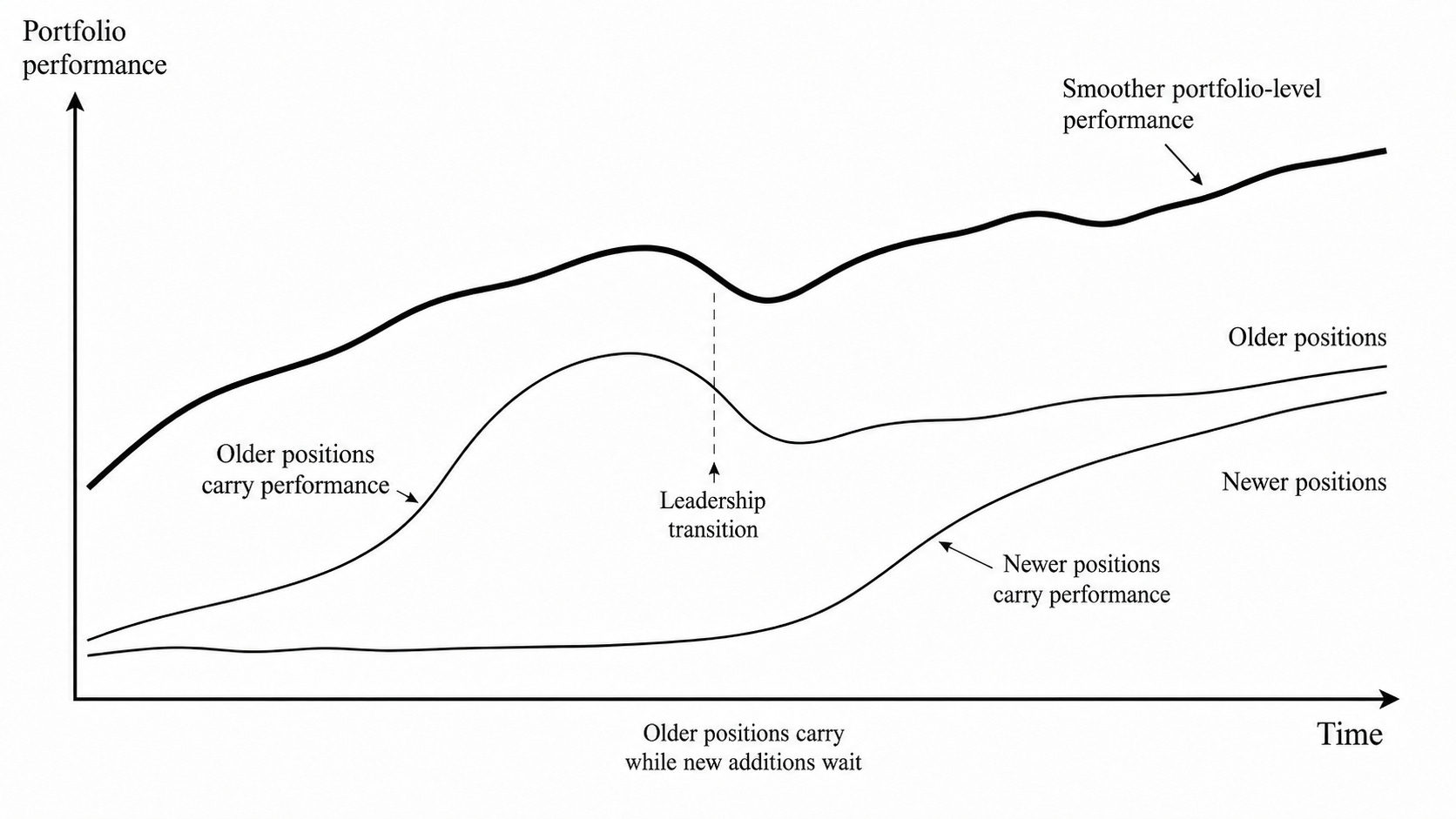

The correct move here is the exact opposite, and it’s actually what prevents performance intermittency at the portfolio level.

When we exit or trim a position, we always reallocate capital to what’s undervalued at that stage. The natural consequence of this strategy is that new positions tend to take longer to perform, as we can’t know where they are on the downward-sloping curve. They are rarely at the bottom tip.

This creates an intermittency at the individual holding level. But, if we are right on the thesis, it eventually climbs the upward sloping side of the curve, driving portfolio performance.

When this is practiced consistently with discipline, portfolio-level performance intermittency also declines substantially as positions perform at different times. Thus, as we wait for new additions to perform, older positions that already started their move on the upward sloping side of the curve carry the performance.

For instance, in 2025, one of our most substantial performance drivers was SoFi, which we aggressively bought in late 2023 and early 2024. Meanwhile, our Oscar position that we bought in late 2024 didn’t do much throughout 2025. This year, Oscar has become a multi-bagger for us, driving substantial alpha.

This way, portfolio performance kept improving without any major intermittencies.

At the beginning of this year, I made three important claims according to this strategy:

One of our big positions that lagged in 2025 would drive alpha in 2026.

We would look at international markets and derive alpha from there, as the US was already expensive.

We would keep making opportunistic purchases in the AI space and the US generally.

I am very happy that all these have materialized.

The position that lagged in 2025 is up nearly 30% this year, driving alpha.

The non-US position that we took in January has become a multi-bagger.

We made an opportunistic purchase in the AI space and exited after a 30% run.

We are not deriving alpha from randomness; the strategy we set out earlier drives alpha. This is what makes me happier than the headline performance because it’s what counts. It’s what shows that themes can come and go, sectors may explode or implode, some countries can stall, and some countries may grow fast; regardless, our strategy can drive returns.

We have derived performance from AI, from semis, from healthcare, from serial acquirers, from education, from financials, all in 12 months thanks to our consistent application of this strategy. It could be AI today and something else tomorrow. We don’t care; we have a strategy well suited to drive returns wherever the alpha is.

We’ll keep implementing the strategy with discipline, and I am confident that we’ll derive alpha regardless of changing market conditions, as we have done so far:

Our portfolio is now outperforming the market by 31%!

The following transactions took place in our portfolio in June:

Exited 2 positions.

Trimmed 1 position.

Opened 4 new positions.

In the previous updates, I had provided my outlook for each company in the portfolio. Below, I’ll provide an outlook for our new positions as well and share overall portfolio commentary/strategy going forward.

So, let’s dive in.

🚨Our portfolio is proprietary to the members supporting the publication🚨

Members get portfolio updates every month!

Here is a 25% discount to celebrate new readers!

Valid only until Monday!

📊Here Is Our Full Portfolio!

As of today, we have 22 holdings in our portfolio.