DoorDash: Undervalued Giant With 2x Potential!

One of the best opportunities in the market.

Everybody is fixated on AI…

Twitter and Substack are inundated with people posting about semiconductor stocks or AI-cloud stocks that can run further or about the next so-called bottlenecks..

We have also made a lot of money on these themes.

I was one of the first people who wrote about Nebius on Twitter and this platform, and my early shares have now made 11x. Another banger was AMD. We bought it earlier last year, and it’s now a 5-bagger for us.

However… The space has become too crowded recently, as all the people who missed those bangers since 2023 have flocked to the market over the last few months.

I am not saying this just for retail; it applies to many professional managers as well.

So, for most investors in the market, the current modus operandi isn’t finding businesses whose stocks are undervalued compared to their fundamentals, but trying to find stocks that may move higher due to the hype over their business or products.

Too many people are acting this way that it creates many opportunities in non-AI companies, even though they are already very well known. Some of those businesses are performing incredibly, but simply not enough money is flowing into their stock to bump up their prices to the levels they deserve.

DoorDash is one of these ignored businesses performing very well.

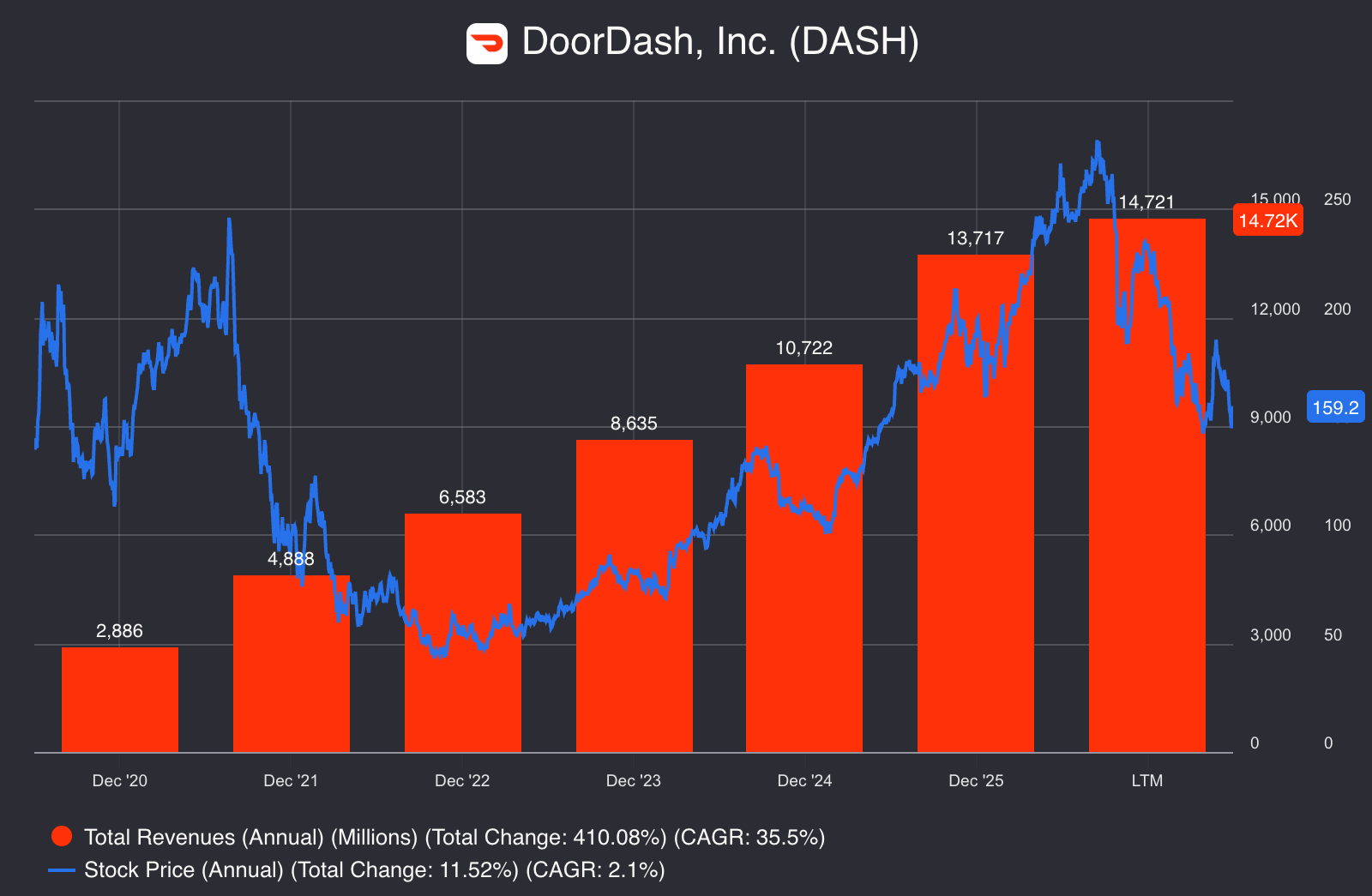

Take a look at this:

Its revenue is now almost 7x what it made in 2020, yet the stock has gone nowhere.

Of course, it was pretty overvalued when it made its IPO during the COVID bubble. However, it’s grown its way out of its overvaluation. If the market hadn’t been fixated on AI, it would have already re-rated DoorDash here and bumped up the price. This hasn’t happened. Market doesn’t care because it’s not AI.

This makes DoorDash an incredible opportunity for those who:

Want to deploy capital outside of speculative AI names.

Are seeking a foundational anchor for their portfolio.

Don’t want to play momentum & demand game.

It’s simply an old school bet—high growth, giant moat, attractive price.

So, let’s cut the intro and dive deep into why I think DoorDash is a great opportunity now and what you can expect from it going forward.

What you’re going to read:

1. Understanding The Business

2. Competitive Analysis

3. Investment Thesis

4. Fundamental Analysis

5. Valuation

6. Conclusion

🏭 Understanding the Business

After graduating from law school and before I took an analyst position in an investment firm, I started as a lawyer in the Bay Area.

Before settling into the competition department, I spent some time in the Venture Capital department and made many friends in the industry. One of those friends was working in a reputable firm that makes dozens of investments every year.

A topic we often discussed was how they picked their investments. He told me that their simple principle was “investing in solutions, not in products.”

They simply wanted the company to solve a critical problem that people having the problem would readily pay for, rather than making a product that requires you to make people desire it through marketing.

I asked how they understand whether something is a real problem. He said, “we love it when the founders themselves have the problem.”

This was simply the investing thesis of Silicon Valley after the Internet revolution.

Indeed, look at the great companies that emerged in the post-dotcom and pre-AI period, essentially from 2000 to 2022, you’ll see the same pattern pretty often:

Uber: Founders had an unpleasant experience of trying to find a cab.

AirBnB: Founders wanted to rent out their free couch to pay their rent.

Dropbox: The founder was sick of his USB. He wanted remote access to his files.

All these companies grew quickly because the problems founders had were shared by millions of other people across the world. When they offered the solution, the world jumped on it.

DoorDash is one of those businesses inspired by a problem its founders had.

It was 2012, and co-founders Tony Xu, Evan Moore, Andy Fang, and Stanley Fang were still students at Stanford University, living on the campus. They noticed a pretty basic problem when they wanted to order food—none of their local favorites were delivering to the campus.

When it came to delivery, options were limited to the established giants that had their own delivery networks, like McDonald’s and Domino’s. Their local favorites couldn’t offer delivery because their volumes were often too low to operate profitably while paying for a deliveryman, car/motorcycle, and fuel.

At the time, they were taking a class in entrepreneurship where they had just learnt the concept of decoupling the customer value chain. It basically refers to breaking apart the traditional sequence of activities customers go through with an incumbent business, then taking one specific step and offering it as a value-added service.

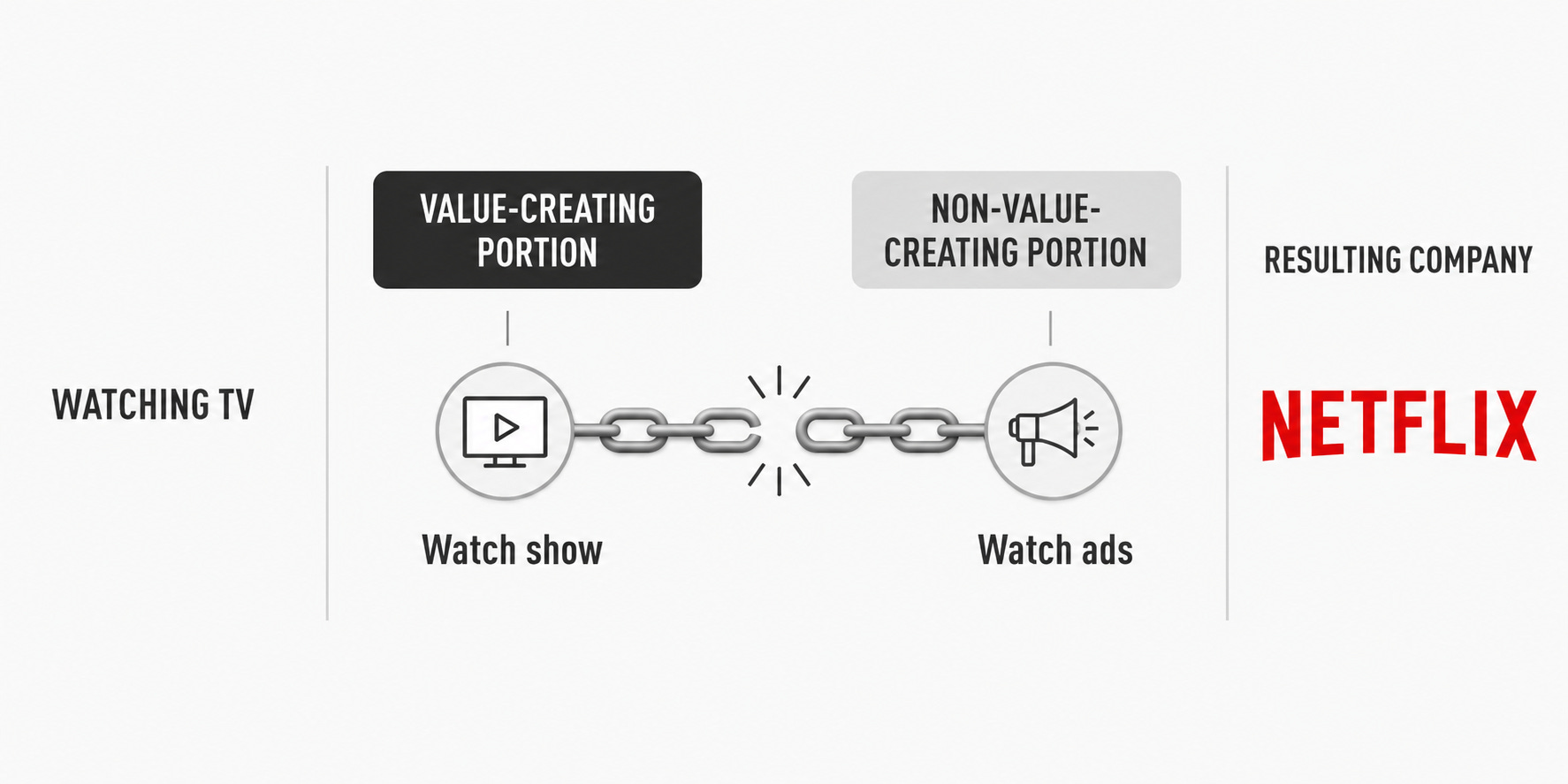

Take Netflix as an example.

In traditional TV, value-creating activity for the audience is watching the show they want. Having to watch ads doesn’t create any value for them. Netflix saw this, broke the value chain, and offered a valuable part as a standalone service that customers want to pay for to get rid of the ads.

They reasoned that delivery wasn’t a value-creating activity for low-volume restaurants, but it was for customers, so it could be decoupled. A restaurant shouldn’t need to offer delivery by itself; delivery should be a different service, and customers would be willing to pay for it.

They took menus of their favorite Palo Alto restaurants, made a simple HTML website, and published it to test the idea. They didn’t have an online order process. You had to call the number on the website to place an order. The founders would go to the restaurant, buy it themselves, bring it to you, and take the payment.

They named it Palo Alto Delivery:

It was an instant hit.

They received their first order within 30-45 minutes after they published the website. Orders grew so fast that soon the founders couldn’t catch up and hired other students for delivery, creating the primitives of their current business model.

This early success prompted other local restaurants to join the system and increase their sales, which required more delivery guys and a better payment system. To meet this demand, they streamlined their onboarding to allow restaurants and third-party deliverers (it calls them dashers) to join DoorDash at will.

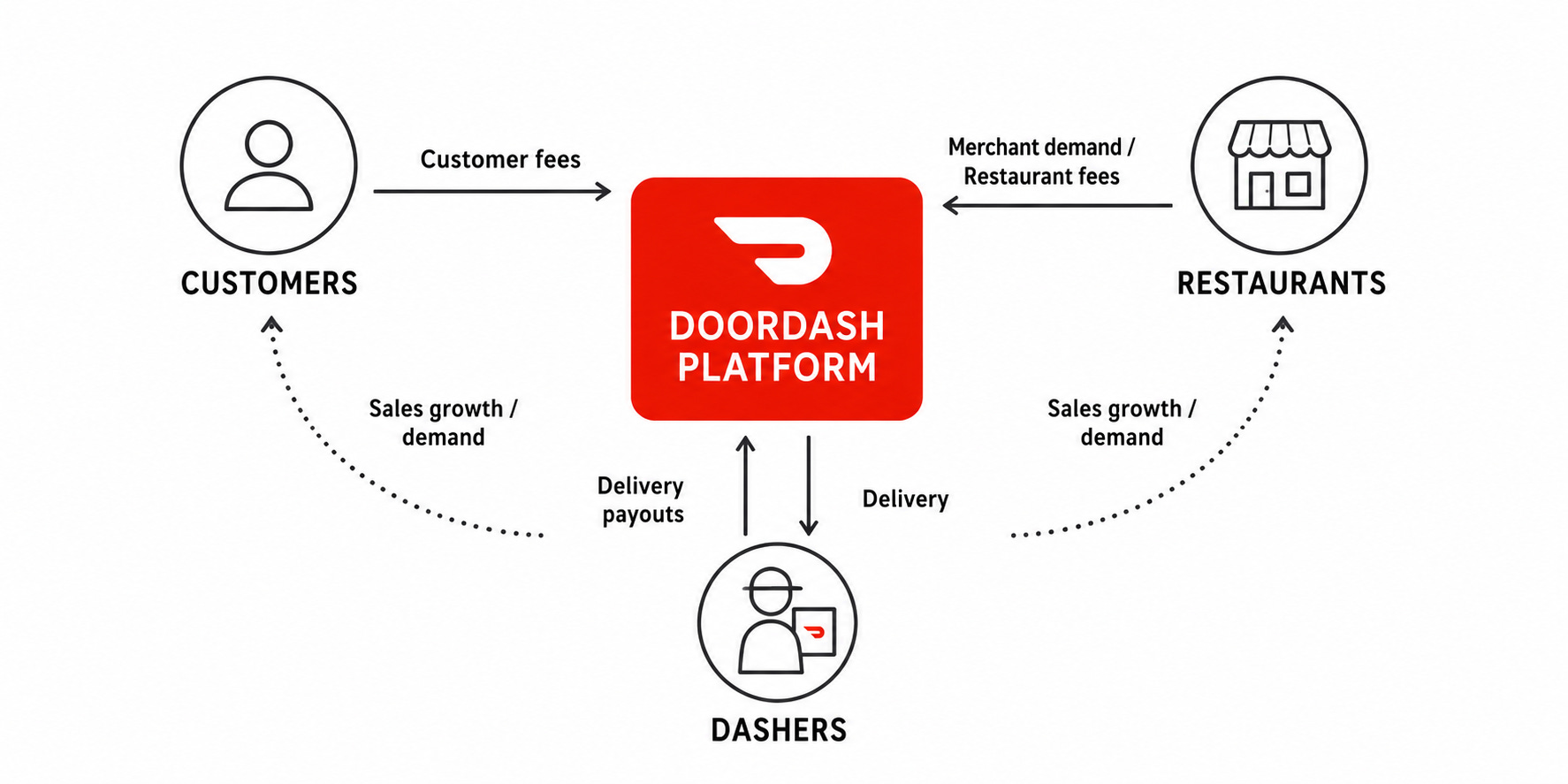

After these modifications, they re-designed their model to link all three parties, customers, restaurants, and deliverers in an interdependent way. It charges fees to both customers and restaurants per order, from which independent deliverers get paid, and DoorDash generates its top-line revenue.

This model essentially decoupled the delivery as a value-creating activity in and of itself and embedded it into a self-sustaining network. And this is exactly what DoorDash is—it’s a network of three interdependent parties:

You can basically read it as a centralized delivery network where sellers and end customers pay for delivery and platform maintenance. Founders saw this and instantly understood that they could leverage this model basically to deliver anything in any geography, not just to deliver food in the US.

So, as the platform grew, they leveraged its power to enter new verticals and geographies:

2019: Officially completed its expansion to all 50 US states.

2020: Launched grocery and local convenience delivery.

2021: Acquired the European delivery company Wolt and launched its ad business.

2024: Launched a commerce platform, allowing branded delivery service and apps.

2025: Acquired Deliveroo, a delivery network focused on the UK and Ireland.

Do you see what it did?

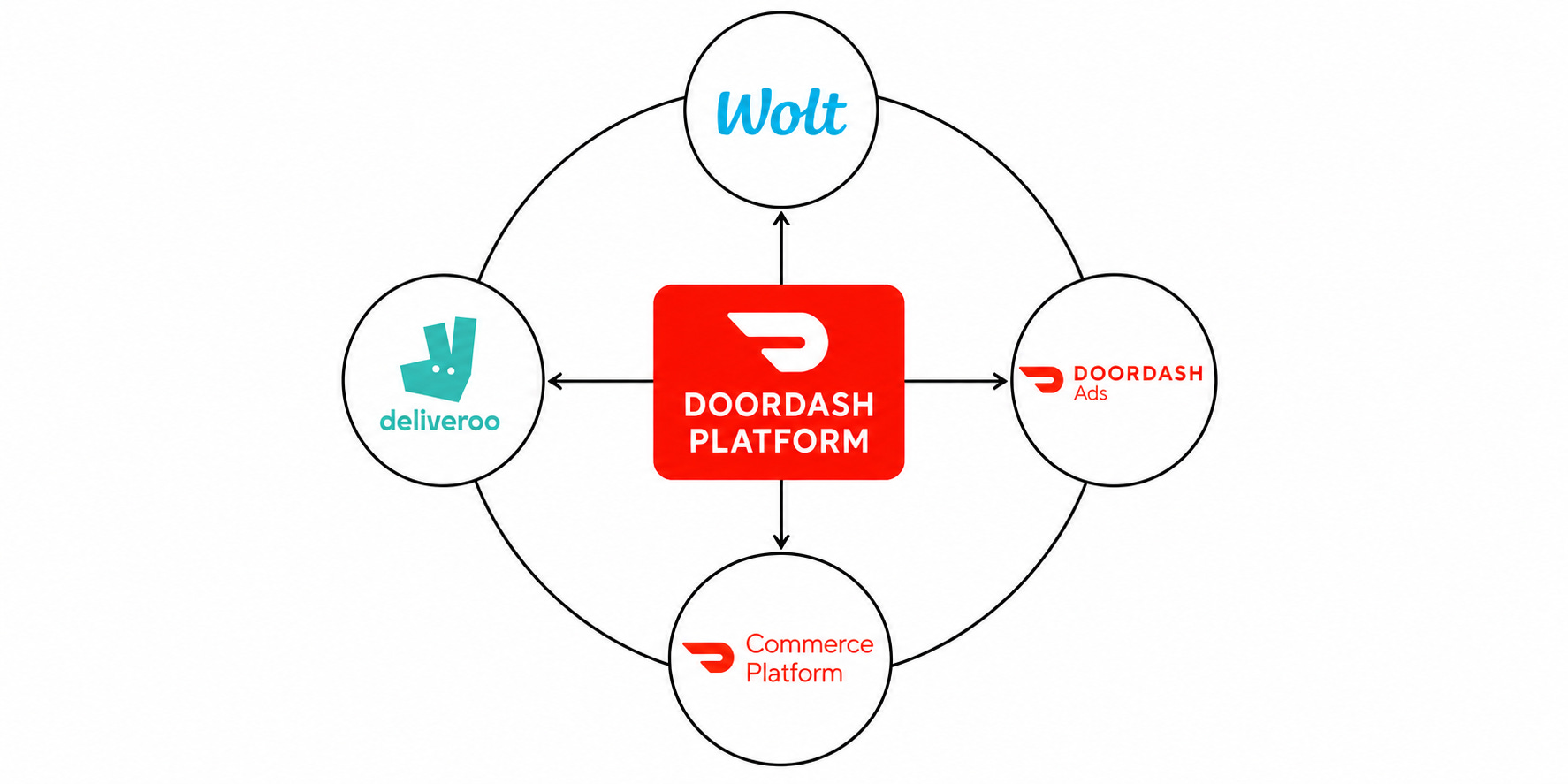

It used its core DoorDash platform to expand into other delivery verticals like groceries. It used its growing capital base to expand internationally by bolt-on acquisitions. It then used this expanded delivery platform to launch complementary businesses like commerce and ad platforms.

It’s essentially become an ecosystem of complementary businesses, feeding from a central platform that is a multi-sided network:

This is what DoorDash is and how you should see it.

If you draw the definition of what it does rather than its natural character, you’ll miss the strength of the business and endless opportunities waiting for it. It’s an ecosystem business, centered on a core multi-sided platform.

The importance of seeing the business this way cannot be overstated, as this is what gives DoorDash its immense competitive strength, which is one of the core elements making it an amazing investment opportunity.

🏰 Competitive Analysis

If you have been following this publication for a while, you know that competitive strength is at the core of our investment philosophy.

The reason is simple.

Investors make money when the intrinsic value of a business increases over time by more than what the market is pricing in today.

That increase in intrinsic value is driven by growth in earnings. The less competition-resistant the business is, the less likely it is to grow earnings by more than what market prices today, as competitors will come in and steal excess profits.

Competition here is used broadly. It includes actual competitors in the same product market, and alternatives that may emerge over time due to technological development.

Naturally, if you get the competition part right and are willing to wait patiently, you’ll almost certainly end up making money, provided that you don’t pay excessive prices for the initial acquisition of shares.

So, the competitive strength of the business is the first thing we look at.

As somebody who spent his early career as a competition lawyer, then focused on competitively strong businesses in his career as an analyst, and is in the process of taking his PhD in competition economics, I have probably evaluated the competitive dynamics of thousands of businesses and business models.

I can say that one model is basically undisputed—multi-sided platforms.

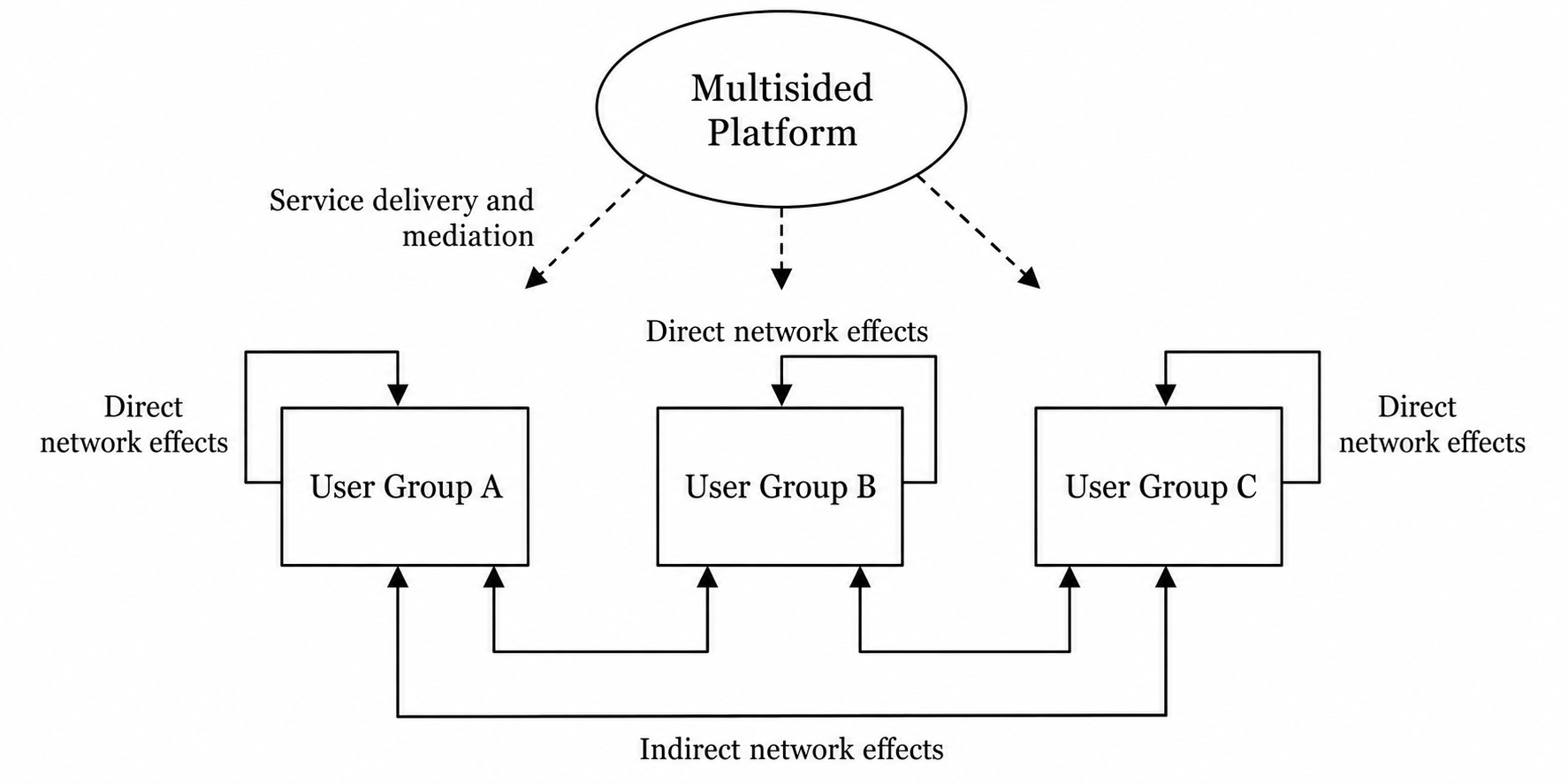

The reason is simple. Multi-sided platforms can house both direct and indirect network effects at the same time:

The mechanic is pretty simple.

For some products, the value customers get out of them increases with the number of people using the same product. This is the textbook definition of direct network effects. The classic example is the telephone. The value of it increased as the user count grew.

This already creates a very strong competitive position. Think about WhatsApp. People don’t switch away from it even though there are other free apps, because everybody is already on WhatsApp.

For some smaller group of products, called platforms, there is not just one but multiple different groups of users. In these models, growth in one user group increases the value for the other and drives growth of that group. This is called indirect network effects.

The classic example would be brick-and-mortar shopping malls. As the number of stores in the mall increases, it attracts more shoppers and vice versa. However, without shoppers, an increase in the number of stores doesn’t automatically drive further growth in the store count.

Most businesses don’t benefit from any type of network effects, and among those that have network effects, 99% has either one or the other. Having both is a pretty rare phenomenon.

If you have one of them, it can give you a very strong competitive position.

If the network has reached the tipping point, it becomes very hard to unseat it. What’s the tipping point? It’s the network size beyond which it’s more advantageous for every user to join that network rather than others.

Think about Facebook. The tipping point was when any potential user had more friends on Facebook than on any other comparable network. After that point, everybody effortlessly joins the network, growth jumps, and sustains until saturation:

As the network beyond the tipping point offers more objective value to any potential customer, it’s very hard to steal users from that network, thus very hard to compete with it and disrupt it.

Now, imagine a platform that has both direct and indirect network effects, both beyond the tipping point. It would be virtually impossible to disrupt it.

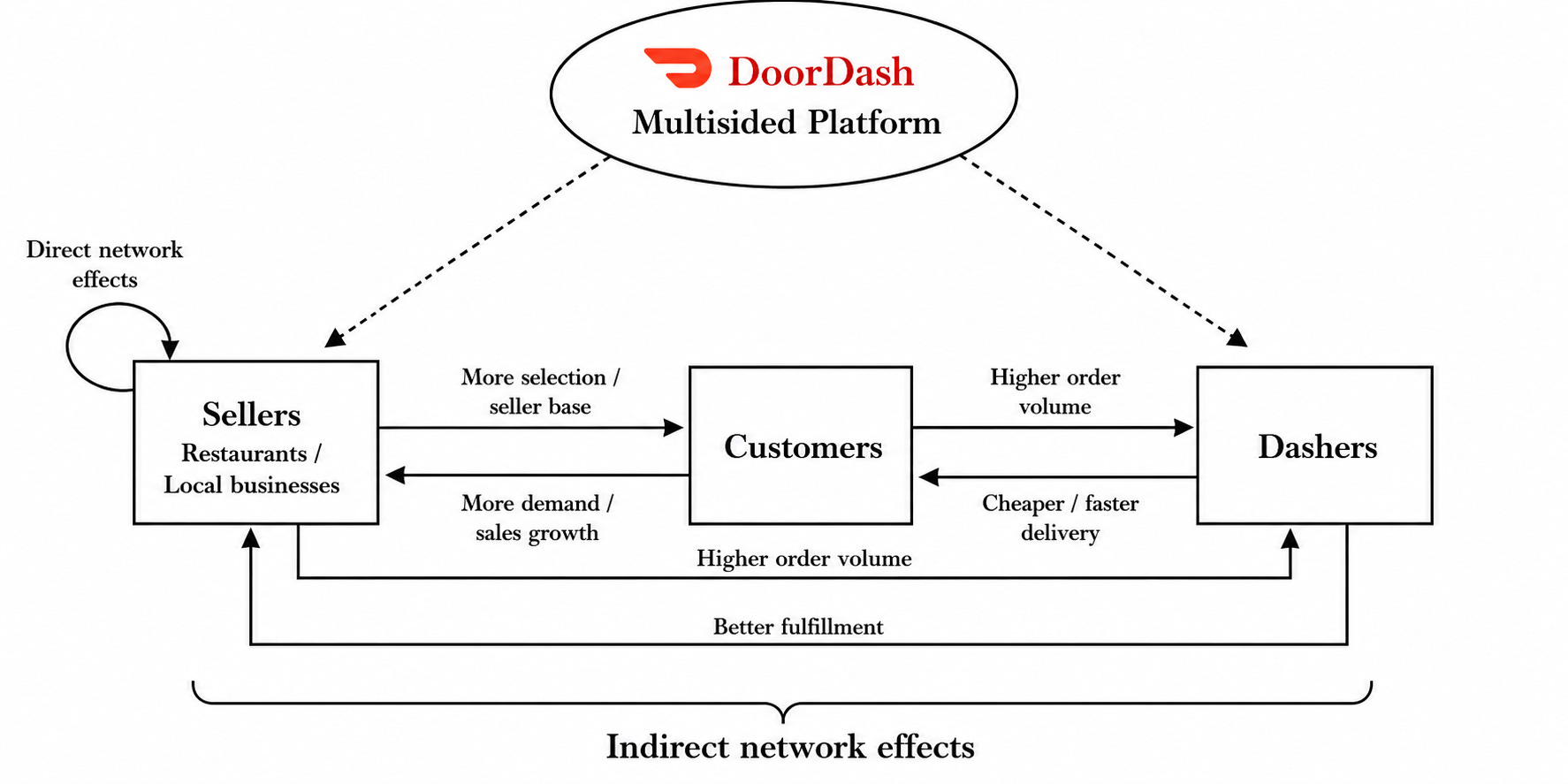

That’s DoorDash.

Its network has three sides—sellers(restaurants/local businesses), dashers, and customers.

As the sellers in the system grow, it attracts more end customers as they come with their customer base. Seller growth also propels further seller growth because other businesses don’t want to slide behind in competition and want to tap into that customer pool.

Customer and seller growth naturally drives network volume higher, which invites more dashers. The more dashers a platform attracts, the cheaper it becomes to deliver products, attracting more customers and sellers.

And this cycle of growth self-sustains, as all three networks here are beyond the tipping point since DoorDash is by far the biggest delivery platform in the world.

Every new potential customer will likely find more restaurants and better prices on DoorDash than competitors. For every prospective seller, there are more prospective customers on DoorDash than others. For every delivery guy, DoorDash offers more revenue opportunities than any other competitor.

Result? Every prospective customer, seller, and delivery guy is more likely to join DoorDash than the alternatives. This makes it almost competition-proof against other businesses.

On the technological disruption side, it’s equally strong. Delivery is a complex function that requires human-level coordination while picking up the package from the seller and dropping it off to customers home. There are thousands of sudden, impromptu interactions involved in the process,

AI and robots won’t be able to take on this complexity anytime soon. It’ll be decades before they can learn to even successfully navigate our streets that were designed for humans. Even when robots can fully replace human deliverers, DoorDash will be the best-positioned company to capitalize on it by deploying robot deliverers, as it already owns the distribution.

In short, DoorDash has one of the strongest competitive positions I’ve ever seen.

Even when a business benefits from a single network effect beyond the tipping point, it’s very hard to unseat it. DoorDash benefits several of them beyond the tipping point. It’s also resistant to disruption by AI, thanks to function complexity and its installed base.

Simply, it’s as close as any company can get to “undisruptable.”

As long as it has growth opportunities, this competitive strength will enable it to exploit it—and it has ample growth opportunities.

📝 Investment Thesis

My DoorDash investment thesis relies on three pillars.

1️⃣ There is a huge runway for growth.

DoorDash is such an exceptional company that the degree of domination it has reached makes people think that it’s a mature business.

Indeed, this was the perception when I talked with friends about the investment opportunity in DoorDash. Those who never looked at it thought growth could be hard because it’s already everywhere.

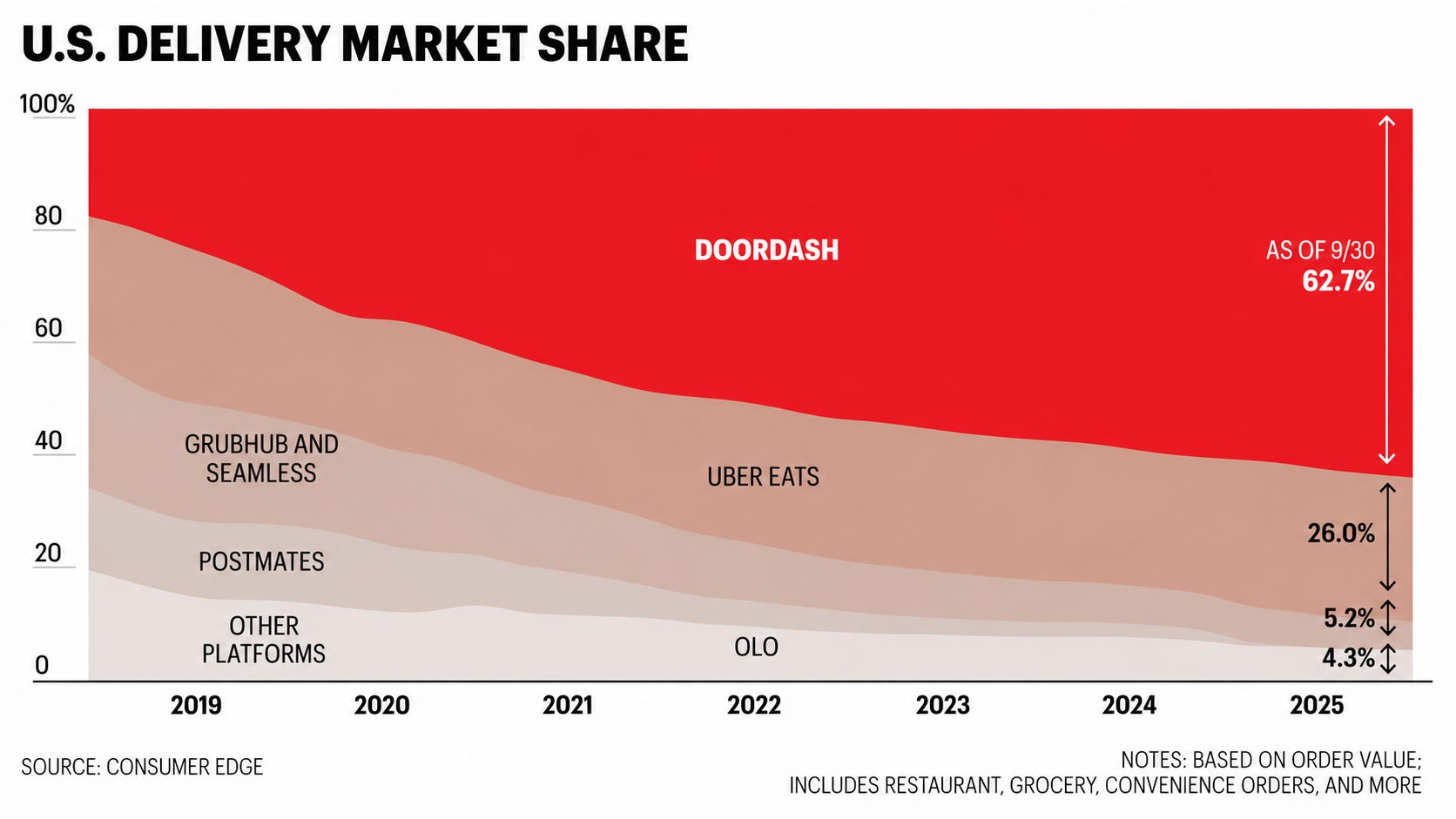

They are right to think that way, as DoorDash controls 67% of the food delivery market in the US, per Consumer Edge:

Yet, it’s just a 13-year-old company that is still early in its growth story.

The global online food delivery industry is expected to reach ~$620 billion annual run-rate by 2030, while the quick commerce run rate is estimated to hit ~$380 billion in the same period, per Grand View Research.

Even if DoorDash can reach just 3-5% global penetration, which is plausible given its dominance in the $US, we are looking at a $30-$50 billion revenue opportunity, and this is excluding other revenues from the commerce platform and ad business.

It generated just $14.7 billion last year, and only 16% of it came from global markets.

Even if the real growth of these markets stops beyond 2030, DoorDash will still be able to grow fast by increasing its global penetration.

2️⃣ AI will drive significant margin expansion.

As I said above, DoorDash is still a very young network.

With network businesses, it’s endemic to see expanding margins since fixed costs are spread over a larger customer base as the network grows. Thus, when we value younger networks, we look at similar networks that are more mature and assume margins in maturity will be similar.

DoorDash currently has 6% profit margin, confirming the young network proposition.

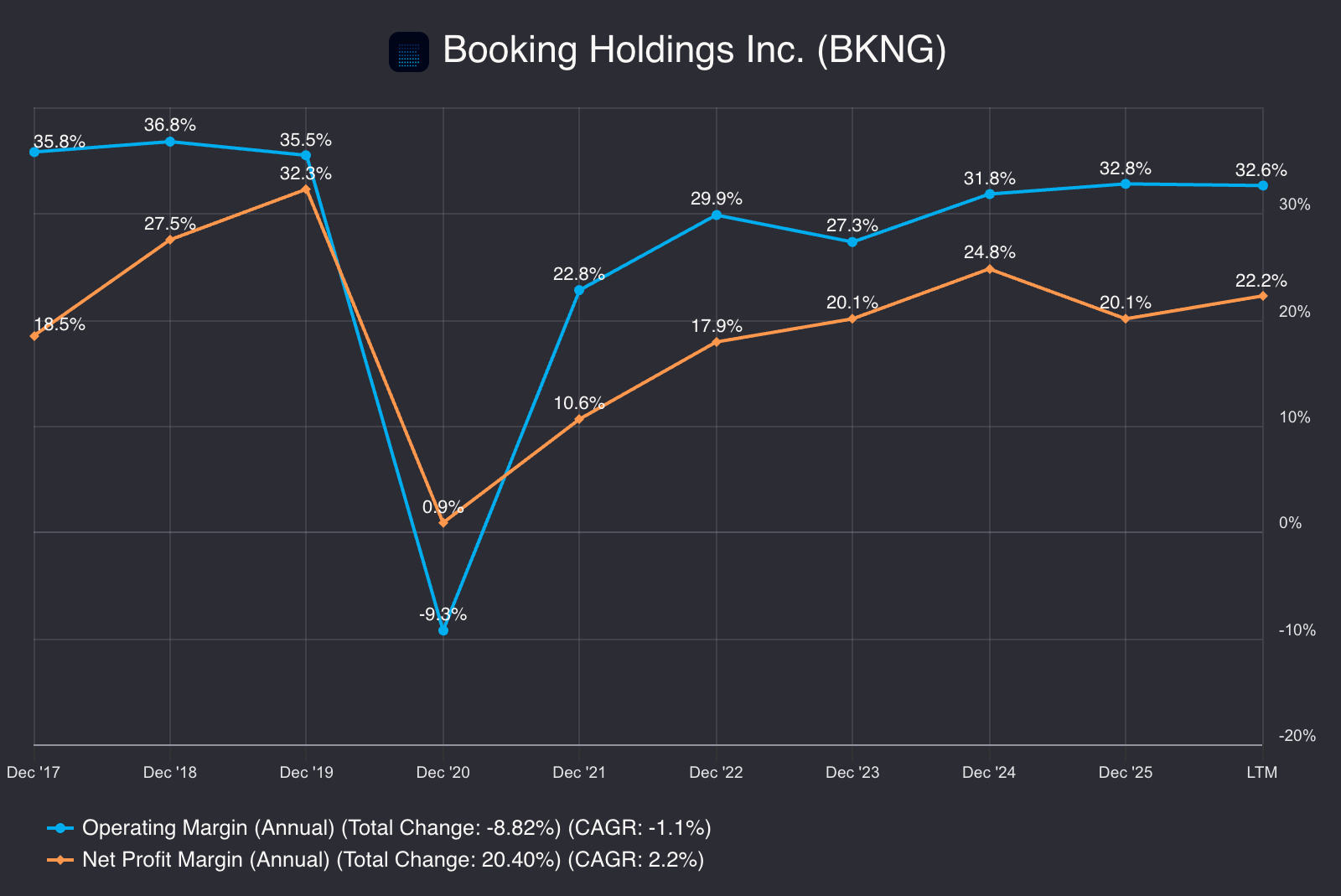

When we look at more mature networks like Booking.com, we see that profit margins can go as high as 30% and the operating margin is consistently above 30% (ex-COVID):

Thus, a reasonable and conservative maturity net margin assumption for DoorDash would be between 25-30%.

However, these mature networks reached maturity when there was no AI. They achieved these margins while employing thousands of software engineers writing code by hand. The deployment cycle was months. Now, each engineer is probably at least 10x more productive, and deployment cycles are 10x shorter.

So, these platforms can probably be run by a fraction of the workforce they have today.

We are already seeing this as Meta announced it’ll lay off 10-13% of its workforce.

As a result, maturity margins will move higher. Valuation models will need to be updated to factor in perhaps +35% net margin rather than something between 25-30%.

The market currently doesn’t price this in, and models haven’t been adjusted to reflect higher margins in maturity, creating substantial optionality for marketplaces.

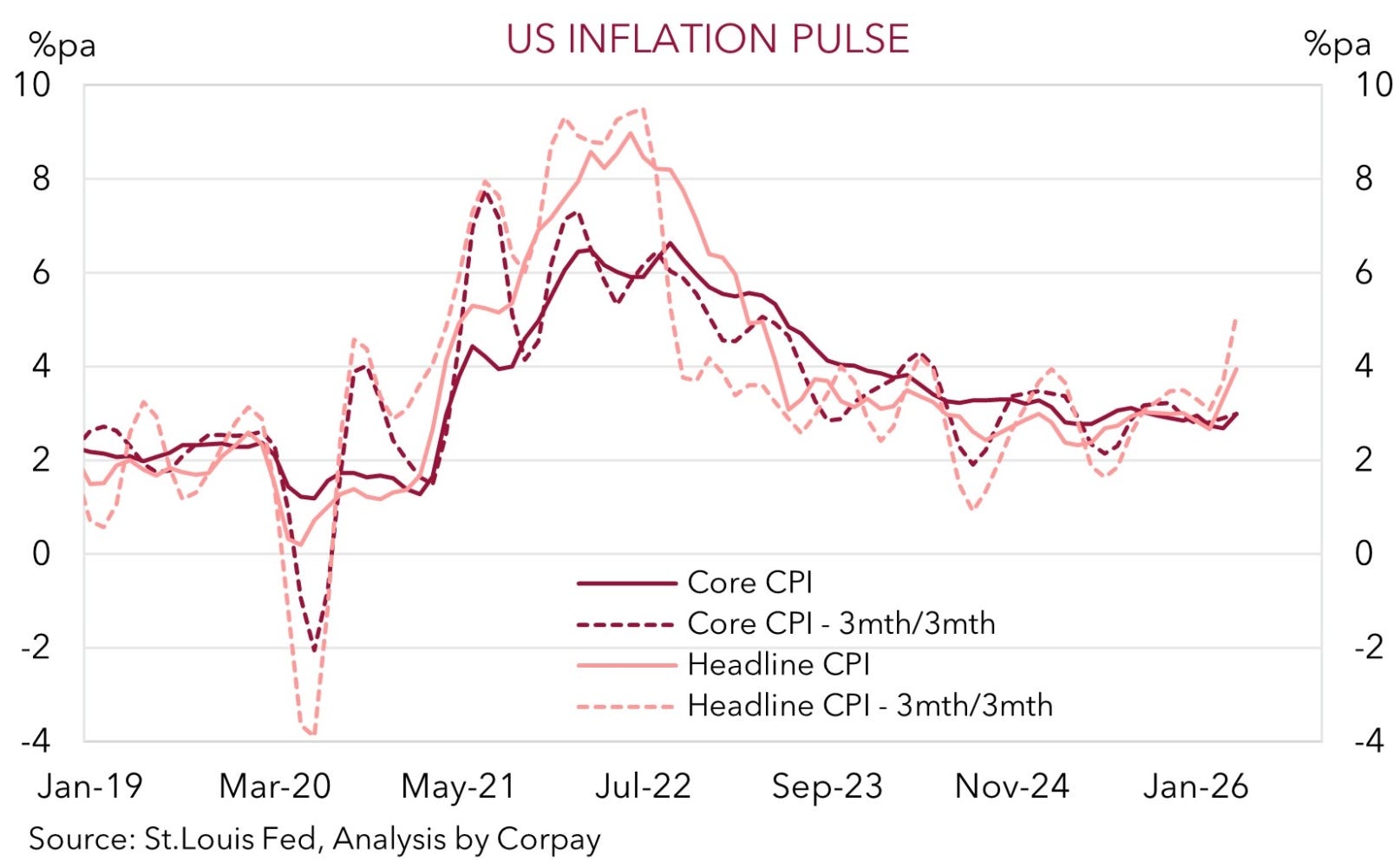

3️⃣ It’s inflation-proof.

Inflation has been a global problem since COVID, and it’s not going anywhere soon.

Most developed economies have taken inflation under control through interest rate hikes post-COVID, but it’s now ticking up across the globe due to several factors like reciprocal tariffs, the Iran War, and increasing energy costs driven by exploding power demand from AI buildout.

We are already seeing inflation tick up as headline inflation hit 3.8% in April and outpaced wage growth for the past three months:

I expect this to continue as the effects of the tariffs still haven’t fully kicked in, the conflict in Iran continues, and AI buildout keeps driving power demand.

In this environment, businesses that struggle to pass costs to customers will be hit while those with pricing power will be largely insulated, or even benefit from inflation.

DoorDash is one of the strongest companies in the latter group.

Its business model automatically passes costs to customers as it charges sellers a commission based on the basket total, and both % based platform fees and flat delivery fees to its customers.

Commission-based fees increase alongside inflation as the basket totals grow. Given the dominant position of its network, it enjoys giant pricing power, enabling it to hike flat fees above inflation.

Thus, inflation is often a tailwind for DoorDash rather than a headwind.

Even if high inflation leads to higher rates, rate hikes, and even recession, the shrink in order volume has proved to be temporary as delivery is a mega-trend.

In the 2010s, fewer people ate at home compared to the 2000s, and now even fewer people eat at home than in the 2010s. This won’t reverse, given that birth rates drop and family sizes shrink. These people often prefer ordering online rather than cooking for themselves.

We can easily see this by looking at the high inflation period in the aftermath of COVID-19. Even though volumes dropped a bit in 2022-2023, it quickly recovered, and companies like DoorDash have become even more profitable due to higher base prices.

In short, DoorDash is an exceptionally well-positioned business.

It still has a giant global market opportunity ahead, it can increase margins beyond what’s been standard for marketplaces due to AI, and it can turn inflationary pressures into incremental growth thanks to its massive pricing power.

I believe it will exploit all these opportunities going forward. Its capability to do so is proven by the exceptional execution since it has become public.

📊 Fundamental Analysis

➡️ Business Performance

I analyze hundreds of businesses every year.

When you look at the income statements, for some companies, you need to put in additional effort to understand what’s happened so far and where they are going, and for some others, it’s all crystal clear. You feel like you are just watching a masterful execution, similar to the way you watch a masterful movie.

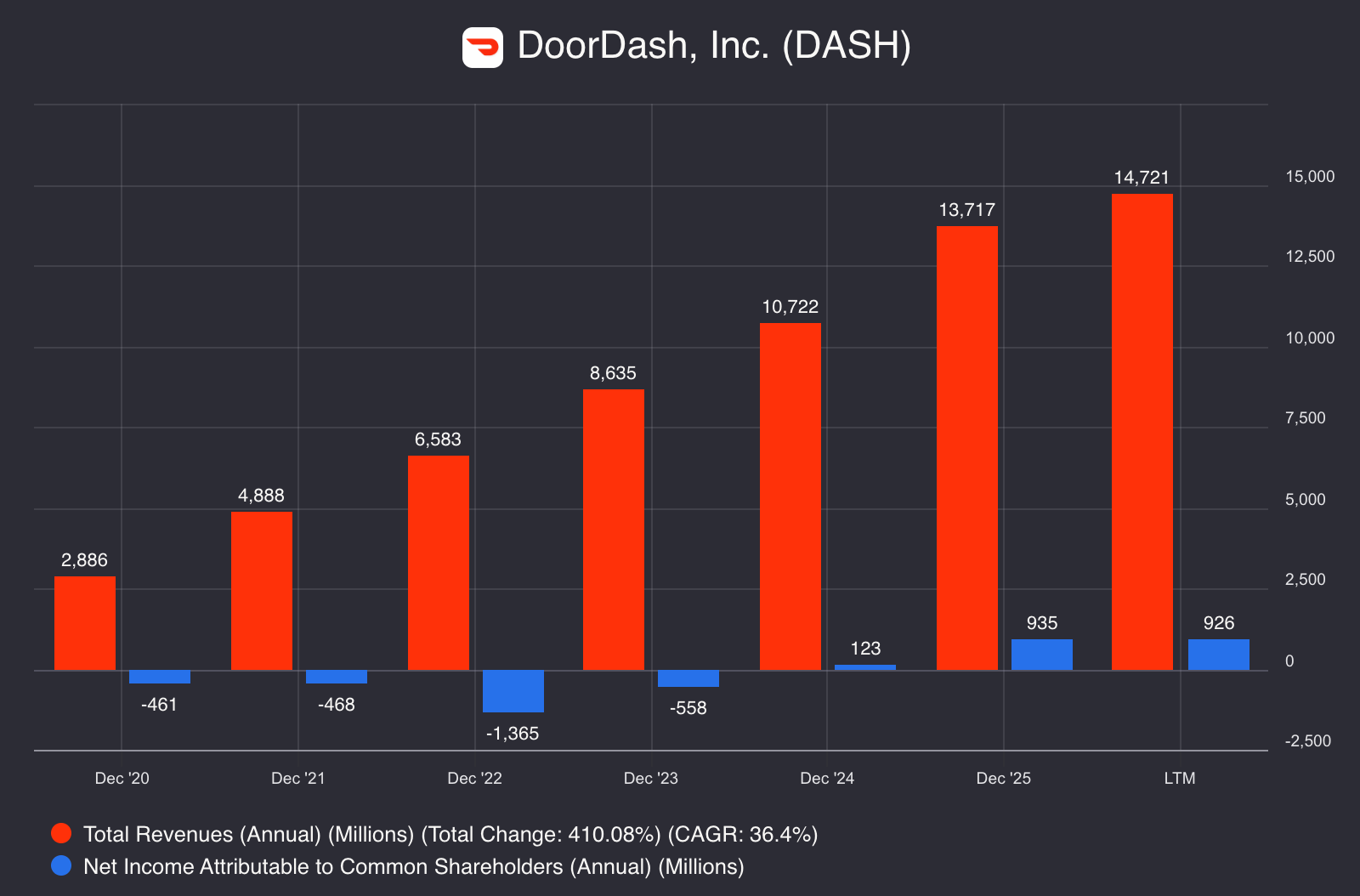

DoorDash fits squarely in the latter category. Take a look at this:

It delivered 36.4% annual top-line growth since 2020 while achieving profitability. Most young growth companies experience a significant drop in growth while they transition to profitability, but DoorDash didn’t have it. It even accelerated. This further illustrates how exceptional a company we are looking at.

Headline numbers already look amazing, but if you look deeper, it gets even more impressive as you see the business has already validated one of the core pillars of my investment thesis.

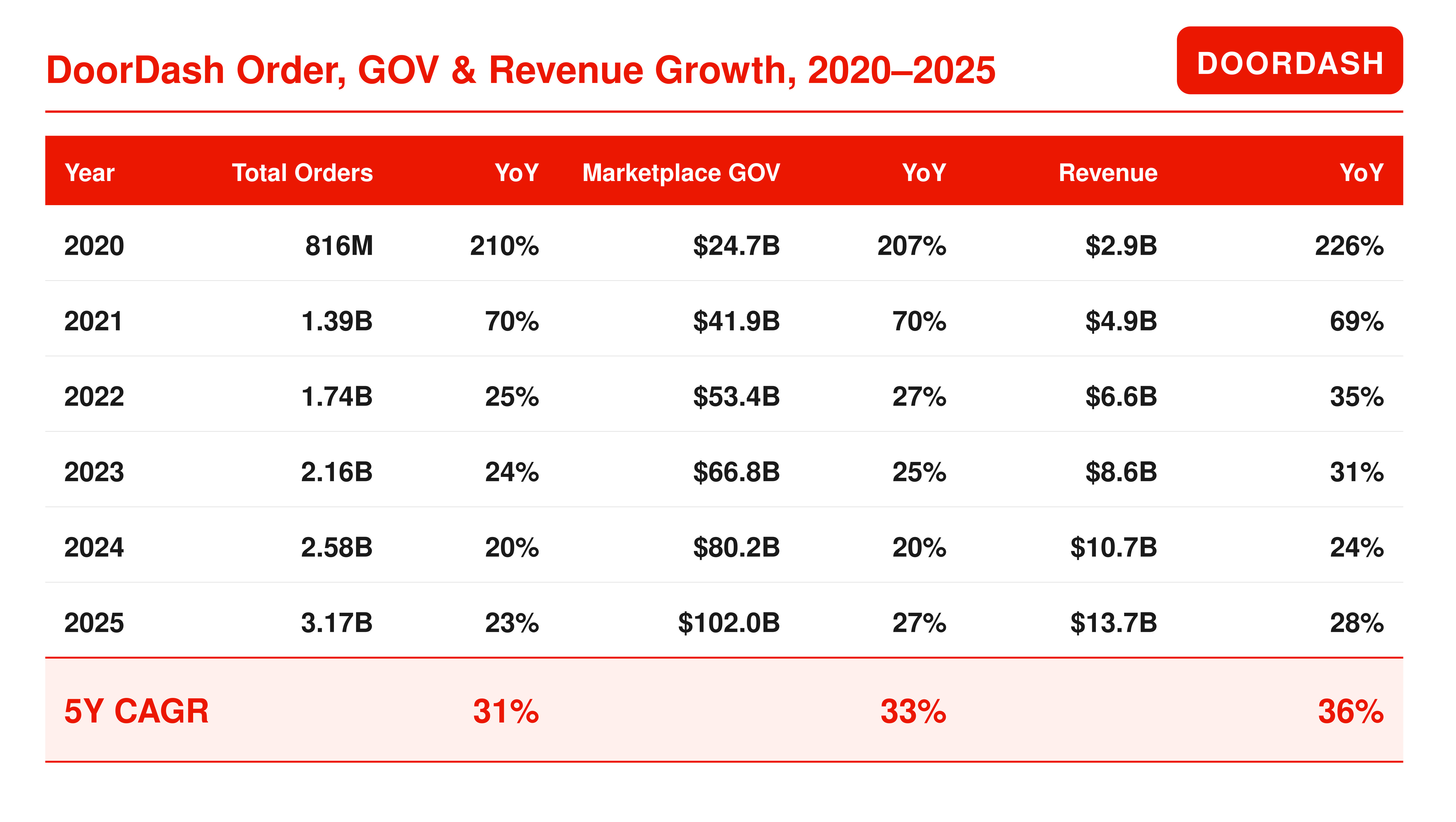

Take a look at this:

As you see, its total orders grew by 31% annually since 2020. Gross order value (GOV) grew at 33% CAGR, closely following the order volume. Revenues, on the other hand, grew by over 36% annually in the same period, illustrating sheer pricing power.

We are looking at a business executing at an elite level and validating core pillars of the investment thesis at the same time. It rarely gets any better than this.

➡️ Financial Position

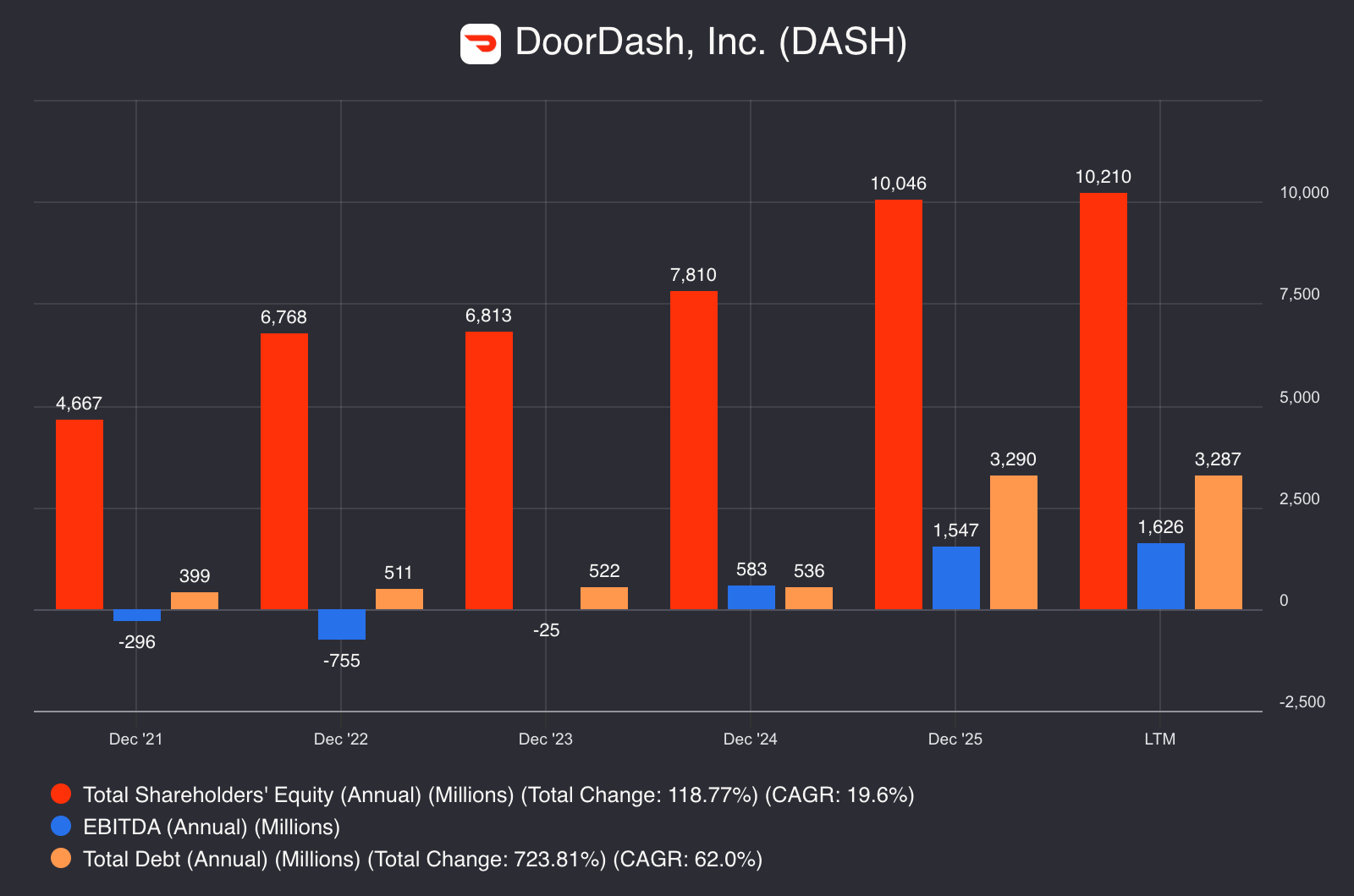

Two words are enough to describe its financial position—rock solid.

It’s impressive that DoorDash managed its balance sheet conservatively despite its insane growth, illustrating that its growth is almost solely driven by network effects and platform strength.

It currently has over $10 billion in equity against just $3.2 billion in debt, and its annual EBITDA can pay the debt in two years:

What draws attention here is the jump in its debt in 2025. This was driven by the $2.85 billion loan it received from JPMorgan Chase to finance its $3.9 billion Deliveroo acquisition.

If it weren’t for the Deliveroo acquisition, we would probably be looking at somewhere around $400-$500 million in debt with $1.5 billion in EBITDA, given that Deliveroo didn’t significantly contribute to DoorDash’s 2025 EBITDA, as it was making $16 million net profit at the time of acquisition.

So, its financial position is even stronger than it looks on the surface, which is already amazing. No red flags here.

➡️ Profitability & Capital Allocation

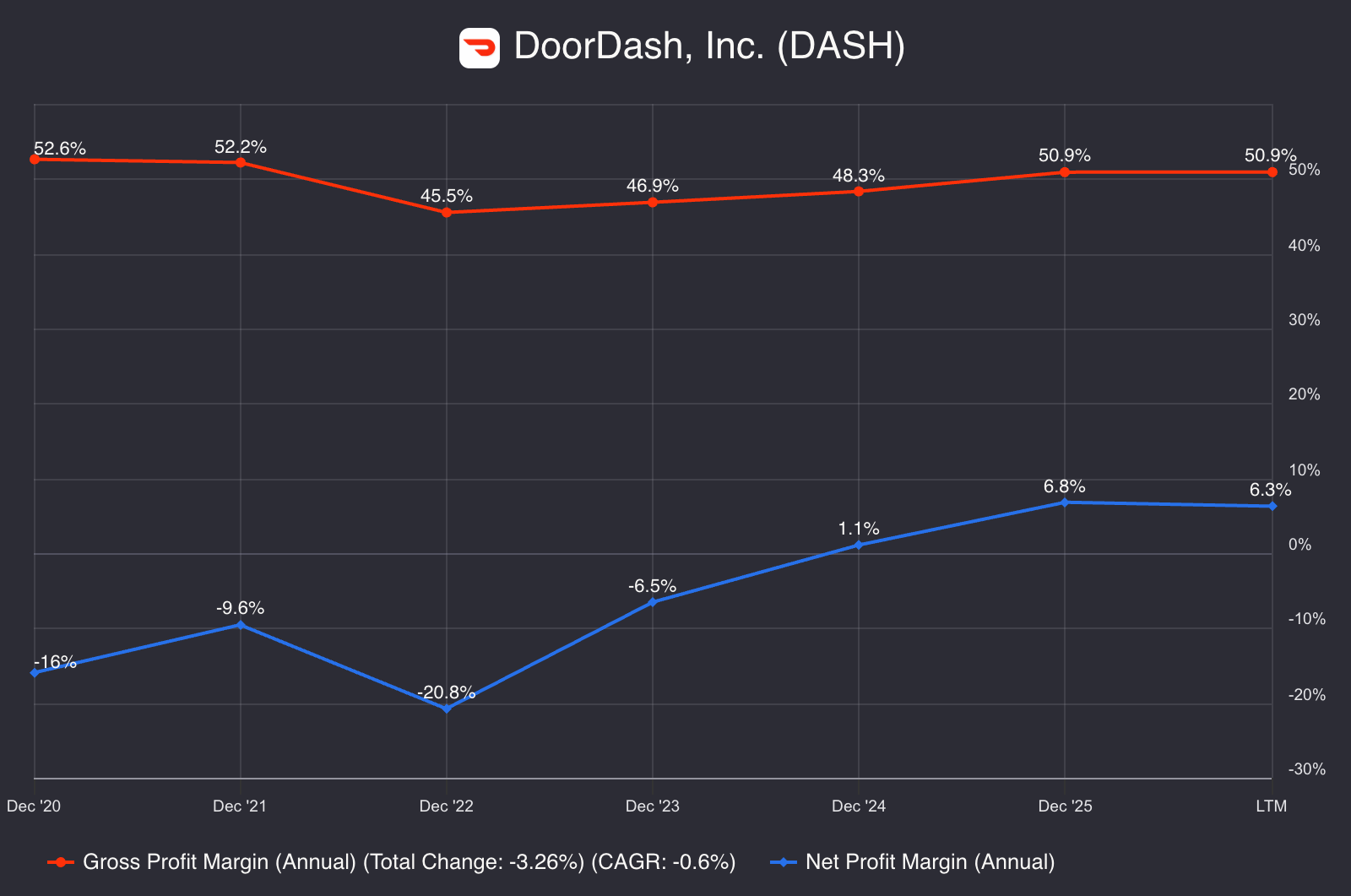

⏺️ Margins

Its margins tell the exact same story we laid out about DoorDash—a dominant platform business that has just transitioned from a startup to a young growth company:

Stable gross margins validate its competitive advantage, while rapid net margin expansion post-inflection indicates it has reached platform feasibility, where the cost to serve additional customers is way below the marginal revenue generated from them.

This is the perfect time to get into these businesses as they are still growing fast and the market doesn’t usually price them to the full extent, given that future growth and end margins are still uncertain.

The key is correctly evaluating the competitive strength of the business. If it really has durable unfair advantages, the uncertainty is way less material than the market thinks, making the discount an opportunity.

DoorDash has the characteristics that make its advantages durable.

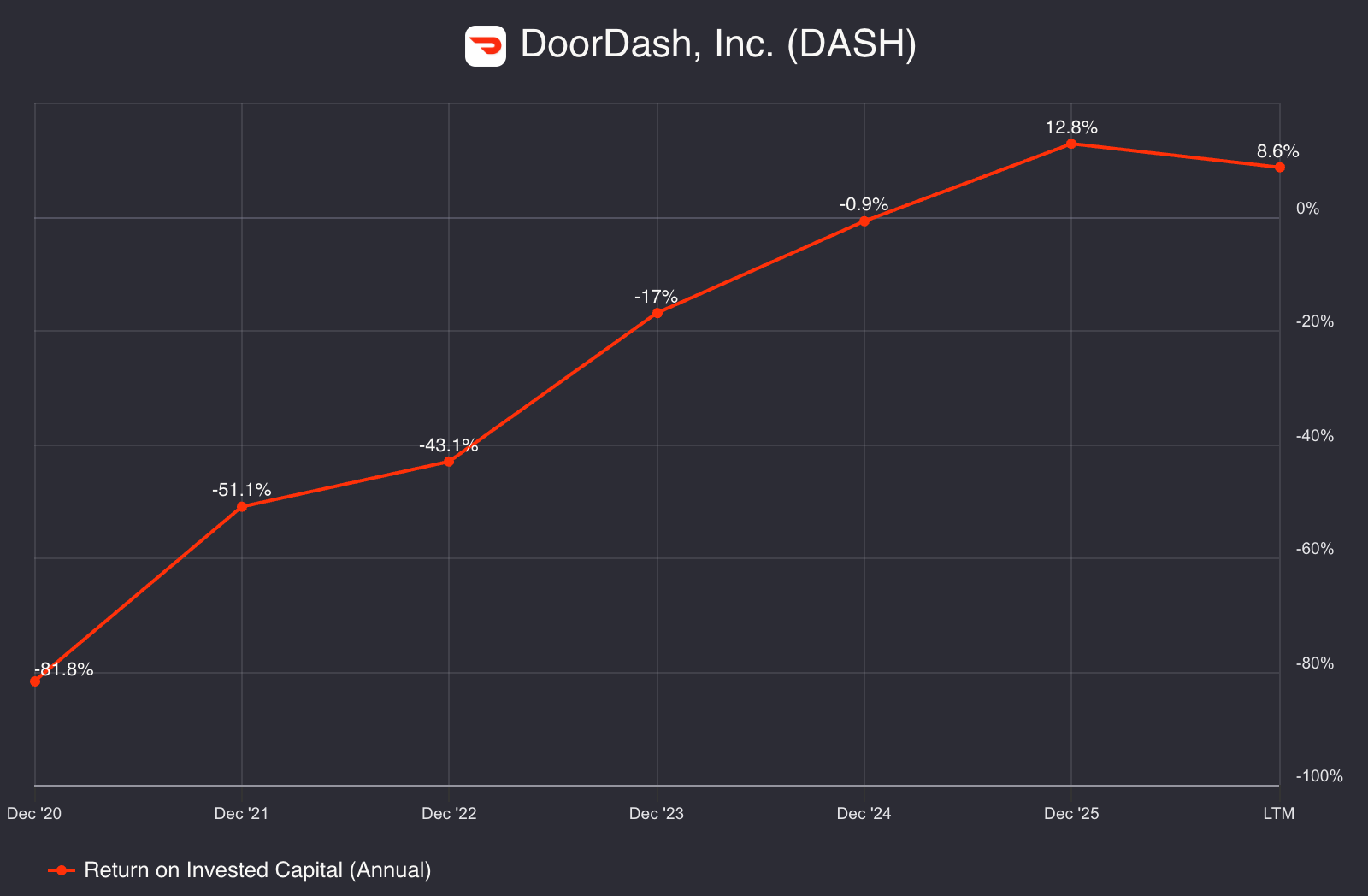

⏺️ Return on Invested Capital (ROIC)

Its ROIC follows the young growth company trajectory as well. It hit the inflection point in 2025 and is currently standing at 8.6%.

This rapid expansion in a year signals that its ROIC will easily climb above 12%, the average for all American firms, and may continue to rise above 20% as more mature multi-sided platforms like Meta easily reach 25% ROIC. Uber is closer to DoorDash than Meta; it’s still growing fast, and its ROIC is already at 20%.

For a young company like DoorDash, the sales-to-capital ratio [revenue/(total debt+total equity-cash)] is more indicative of capital allocation performance.

As of the end of 2025, DoorDash’s sales-to-capital ratio stood at 2.1x, meaning it generated $2.1 of revenue for every $1 invested in the business. For Uber, it was at 1.7x.

Even if we assume 1.5x sales-to-capital and 30% operating margin with 25% tax rate, the normalized ROIC of DoorDash will be around 34% [ROIC = Sales-to-Capital×Operating Margin×(1−Tax Rate)] while it transitions from high-growth to stalwart status.

Summing up the fundamentals:

DoorDash has performed incredibly well since it became public.

Faster revenue growth than GMO validates the core assumptions.

It has managed its balance sheet conservatively without any red flags.

Margins profile describes a dominant platform beyond the topping point.

Return on capital is hidden as it became profitable in 2024, but the normalized trajectory is beyond impressive.

DoorDash has one of the strongest sets of fundamentals I have ever seen.

As we already checked the competition and fundamentals, there remains just one question—is the valuation attractive?

Let’s see.

📈 Valuation

The more competitive advantages a business has, the easier the valuation gets; the less competitive it is, the harder the valuation.

This is because valuation is simply forecasting the total of future cash flows of the business and deciding what they are worth today. The stronger the competitive position of a business, the easier it is to forecast future earnings.

Thus, when you have a strong business with durable competitive advantages, valuation is just coming up with plausible & conservative estimates about the future, and determining the current value of that scenario.

Luckily, we have such a strong business with DoorDash.

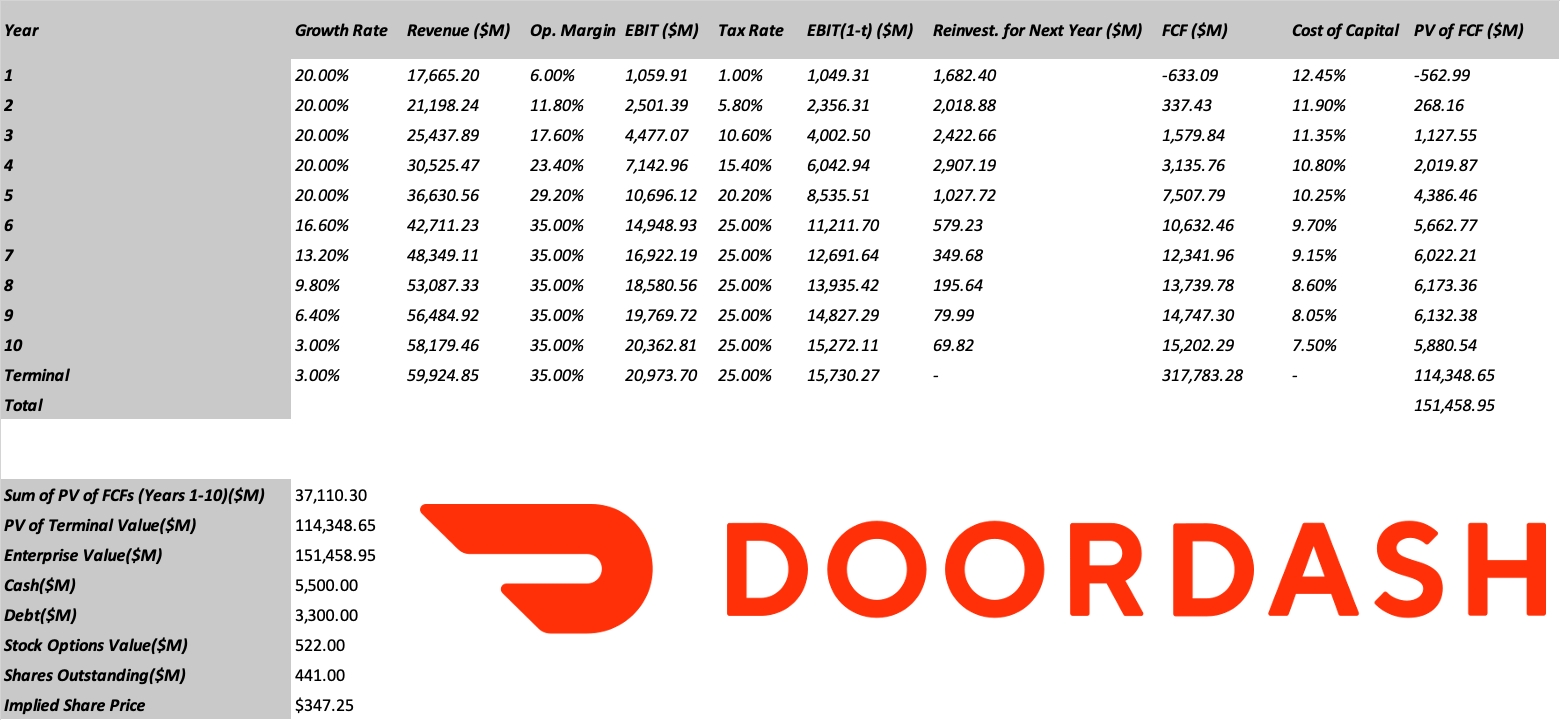

So, what would be such a plausible and conservative scenario for DoorDash?

I assume it’ll keep growing at around 20% CAGR over the next five years, and then it’ll gradually converge to 3% in the terminal period.

Though I believe net margins of these platform businesses can reach 35% due to AI-related efficiencies, I’ll remain conservative, exclude that scenario, and assume 35% operating margin at maturity.

I assume the end ROIC will be around 33%, as it implies a conservative 1.25x sales to capital ratio.

Its cost of equity is around 13%, based on the current risk-free rate, equity risk premium, and DoorDash’s beta. It uses very little debt, so I assume WACC is around 13%, and it’ll converge to 7.5% in the terminal period as it’s the average of mature American companies.

Fair value of outstanding options is $522 million based on their latest 10-K.

Marginal tax rate will be around 25%.

Here is how this scenario plays out:

This scenario gives us $347 per share intrinsic value for DoorDash. This is just around the high end of the current analyst targets, though I believe this is a conservative estimate; it doesn’t factor in any AI-related efficiencies.

I can’t see any reason why DoorDash can’t be run with a fraction of its current workforce when you think about the level AI technologies will reach in 5-10 years from now.

The current price is deeply undervalued in my view.

🏁 Conclusion

DoorDash is one of those rare platform businesses that benefit from both direct and indirect network effects. It’s very hard to compete or disrupt these businesses.

DoorDash has a unique position among all these platform businesses as it’s one of the youngest ones. The market normally optimistically prices these businesses, but it’s currently ignoring DoorDash, as all the money is flowing into AI infrastructure.

It checks all the boxes:

Giant competitive advantage

Ample growth opportunities

Track record of execution

Undervalued stock price

Normally, when the first three exist, the market optimistically prices the stock, but it’s currently ignored as all the money is flowing into AI.

That won’t last forever. Eventually, everything in AI will become absurdly priced, and investors will rotate into other opportunities. When they do, DoorDash will shine like a jewel, and those who seize the opportunity here will be handsomely rewarded.

Long DoorDash.

That’s all friends!

Thanks for reading Capitalist-Letters!

Please share your thoughts in the comments below.

👋🏽👋🏽See you in the next issue!

How would u value it vis a vis Uber. I know its not a pureplay delivery company but Uber does seem to be cheaper valuation wise n offers a more comprehensive package with mobility on top as well

Nice read on Doordash, but some things I'll flag out here:

Firstly your bull case argues simultaneously that:

(A) delivery is too complex for AI to handle for decades which supports the moat,

and (B) AI will allow DoorDash to run on a fraction of its current workforce, driving margins to 35%+.

These can't both be true. DoorDash's major cost drivers are dasher payments, insurance, and logistics ops and not software engineers. If the complexity argument is right, the margin expansion thesis is significantly weaker, and vice versa.

Also, the Booking.com margin analog has a structural problem I want to point out: Booking.com has zero operational logistics. Its margins are high precisely because hotels manage their own inventory and guests self-serve.

But DoorDash coordinates physical last-mile delivery at every order. This is a permanent structural cost that doesn't scale away the way software unit economics do.

I don't disagree with you, and not trying to push a bear thesis, but just pointing out things important for readers to note.