Data Center Power Play Trading At 30% Discount

Revenues jumped by 48% last year driven by data center contracts and it's just the beginning.

The past two weeks have been incredible for us.

Our AMD position that we entered in early 2025 has become a four-bagger.

We turned out to be right on Oscar as it delivered a monster beat. Stock hit $20.

Fluence Energy, which we picked last October, jumped by 100% over the last week.

Thus, I have received many kind DMs over the past week. I tried to respond to everybody, and I want to take this as an opportunity to once again thank everybody for their kind words. Thank you.

Among all the wins above, the Fluence thesis was possibly the most divergent alpha, as nobody was watching it when I published the thesis in October.

Most people think the stock moved up violently because the hyperscaler deals it announced were a surprise. It wasn’t. It’s always been the thesis.

When I looked at it in October, the case was obvious:

Almost all AI data centers need batteries as the cost of intermittency is high.

Fluence was the best-positioned one as it was a JV between AES and Siemens.

Fluence was the first mover in reshoring, with 100% American manufacturing supply chain.

As a result of being a JV by AES and Siemens, Fluence had already inherited most, if not all, hyperscalers in its book of business.

In the thesis I published in October, I wrote this:

So, it already had relations with hyperscalers, and its 100% American manufacturing supply chain made it even more attractive, thanks to tariffs on Chinese products. Thus, it was only a matter of time before it announced a new hyperscaler deal.

This was the core thesis, not a surprise, unlike what many people take from the aggressive re-rating.

After the stock moved, many people tried to chase it. You don’t need to.

Power is currently the biggest bottleneck for building data centers and scaling AI. There are many opportunities across power generation and distribution supply chains. Demand for power distribution equipment is especially tight as data center demand is growing way faster than the manufacturing capacity for these products.

Today, we’ll dive into one of these companies that is riding the exploding demand for power distribution equipment, and it’s still under the radar. Literally nobody talks about it.

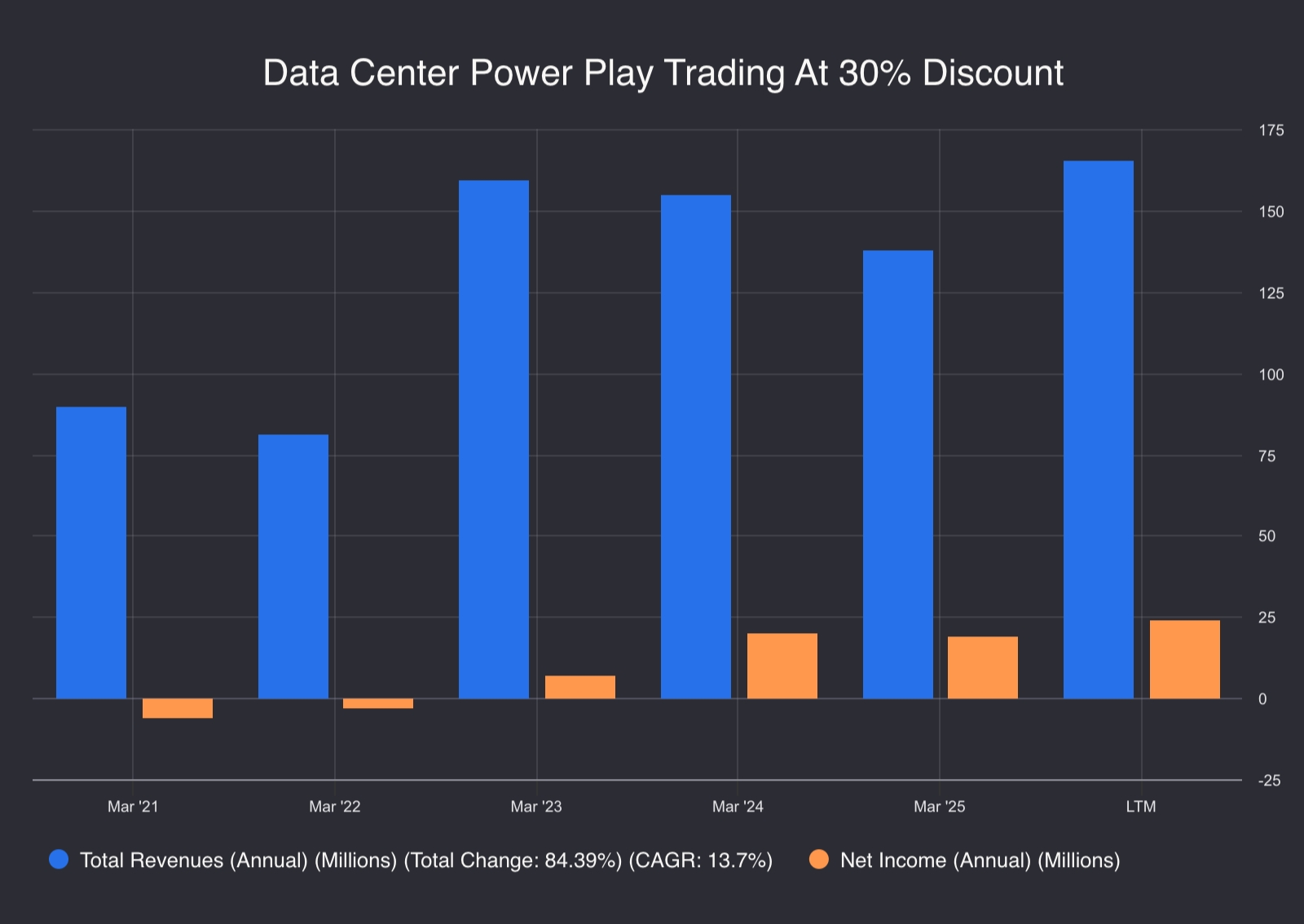

Tailwinds are already hitting the wheel. Revenue jumped by 48% over the last twelve months, thanks to five data center contracts it received in that period:

In January, it received a data center contract half as big as its total revenues in 2025. Yet, this is just the beginning as the data center buildout in its market is still in very early innings, so it’ll likely receive dozens of these contracts over the next decade.

What’s even better is that this optionality hasn’t been priced into the stock as it’s still trading near 17x earnings against the industry average of 30x.

This is one of the best risk/reward opportunities I have seen in the power equipment industry for a long time, as the whole industry has been aggressively repriced due to the data center buildout.

So, let’s cut the introduction and dive deep into this hidden gem.

🏭 Understanding the Business

Power demand from data centers will triple over the next decade, increasing from 500 TWh in 2025 to over 1,500 TWh in 2034.