Buying This Market Leader With 100% Upside Potential!

Simple business that is dominating its market and still growing. Yet, the valuation is unreasonably cheap as investors are focused on AI and tech investments.

Best opportunities often hide in plain sight.

This is what keeps puzzling me about investing. But when you think about that, it only makes sense.

One of the beauties of investing is that it doesn’t converge to one correct answer, unlike most other disciplines.

In science, you have one correct answer; in most day-to-day jobs, there is a correct answer that works for everybody in the same position

In investing, it’s different.

In investing, once many people concur on the same answer, it loses its value. You can’t generate alpha by betting on it anymore. Suddenly, what makes sense is taking the opposite side of the trade, even if the first people who made the bet were right.

Most people correctly think that you have to find relatively unknown stocks, so-called hidden gems, to make real money in the market. That’s of course correct.

Yet, when everybody does that, high-quality businesses known to everybody become overlooked. Their valuations are taken for granted, and investors don’t question their potential much as they rely on market efficiency.

Here is an example:

JP Morgan, the biggest bank in the US, quietly made 3x in the last 5 years.

It was known to everybody, yet most people didn’t even question its potential for further growth 5 years ago.

Let me tell you something controversial—we’ll see many JPMorgans in the coming years.

What the hell does this mean? It means that I think many companies already dominating their markets will have a period of strong outperformance.

Why? Because of what I call the Great Consolidation.

Today, most industries are more consolidated than they were 50 years ago.

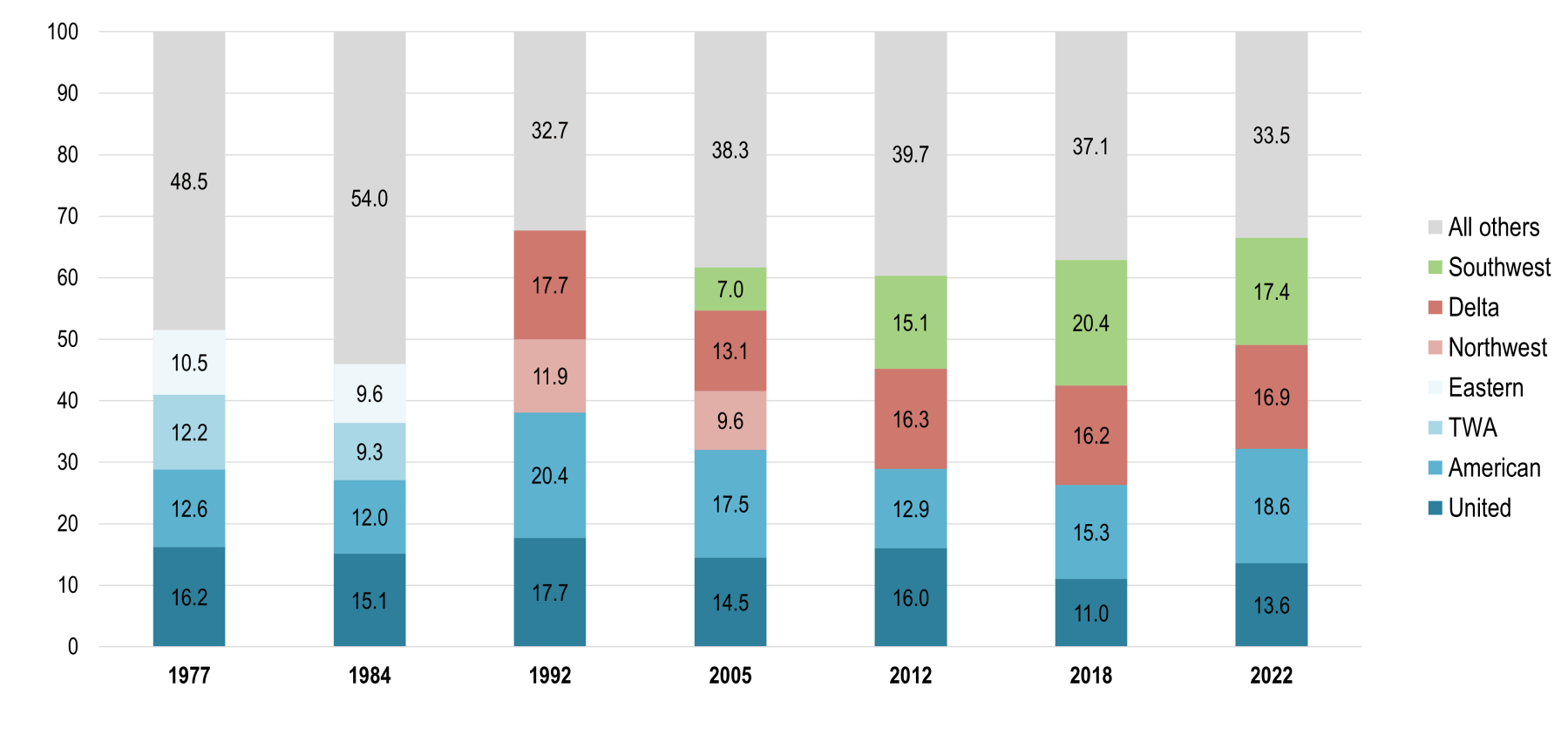

That applies even to markets known to be highly fragmented. The airline industry is an example.

In 1977, the top four airlines owned 51.5% of the US market; today, they own 66.5% and the market has consistently become more consolidated since 2005.

You can see this in many other industries. There are two reasons for this:

Globalization.

Technological development.

Globalization is responsible for the consolidation on a global scale. Before globalization, different countries had their own dominant coffee chains. After globalization, everybody is competing with Starbucks.

Technological development, on the other hand, led to consolidation on the national level. Mobilization and communication got easier, so companies had an easier time expanding from one state to another and from one city to another.

The natural result of this is that a business that is a bit better than the competitors gets a disproportionately larger market share.

When there is no access limitation, everybody wants to stick with the best.

This favors market leaders. When presented with a choice, more and more people pick the leaders, and markets consolidate around a few companies.

Performances of leaders like JP Morgan, Ryan Air, and O’Reilly in what’s normally known as fragmented markets illustrate the phenomenon.

This is not going to reverse anytime soon.

Thus, I believe market leader companies that trade at attractive valuations offer high returns at low risk, as I believe markets will continue to consolidate around leaders, and we’ll see many JP Morgan-like performances.

I found such a business that is hiding in plain sight.

Look at this:

It’s a boring business that is the leader in its market, and it’s not under threat of disruption by AI.

It has grown revenues by 22.8% annually since 2020. It’s still aggressively investing for growth and trading at just 11 times earnings with a 4% dividend yield.

I bought a small position in it a while ago, and I am now looking to grow it.

I think it has 100% upside potential from the current levels, with a very limited downside at 11 times earnings.

So, let’s cut the intro and dive deep into this gem I am buying!

🏭Understanding the Business

Simple, boring, and consistent. These are the foundational pillars of a successful investment, according to Peter Lynch.

Look at some of the best-performing stocks in the last twenty years, and you see this holds:

Monster Beverage, 28.3% annualized return

Domino’s Pizza, 18.5% annualized return

Chipotle, 24% annualized return

In the same period, the S&P 500 returned just 10% annually.

Result? Investors flocked to these businesses, hoping to find the next Monster or Chipotle.

At some point last year, we had Cava trading at 300 times earnings, Wingstop at 150 times, and Celsius at 100 times.

Yet, there are still similar businesses that are largely ignored by the market despite having a track record of consistent growth and a strong market position.