Buying This Boring Business With 3x Potential!

A rare undervalued opportunity in a broadly overvalued market.

Markets are exhibiting more casino-like behavior than they did in the past—this is what Warren Buffett said in his 2023 Annual Letter to Berkshire shareholders:

What followed this was perhaps even more striking:

He ended up warning investors against succumbing to these behaviors, as it always, at some point, ends up in disappointment and loss of their hard-earned money.

What he warned against is exactly what’s happening in the markets today.

People are chasing small-cap stocks trading at 200-300x forward earnings under the name of AI bottlenecks, with the assumption that a future evolution of the technology will create demand dynamics that will justify those prices.

Sounds familiar? If not, I recommend you read some of the investment theses about the new internet companies of the dot-com era.

I am not saying bottlenecks don’t exist; they do. But this doesn’t mean they’ll evolve exactly as we see today, and it definitely doesn’t mean paying 100x sales (yes, sales) for a stock is sensible. It’s not, and I guarantee anybody that they’ll end up losing money if they consistently pursue this.

Only group that makes money out of this feverish behavior, as Warren Buffett says, is the promoters of this behavior, i.e., the promoters of these stocks.

They take positions in small-caps before, then post about it in coordination, creating the hype. Some people naively follow them, believing in the future potential of the stocks, while others follow the greater-fool theory, thinking that they’ll be able to ride the hype and sell way higher if they are early enough.

And nobody is immune to this kind of behavior, even the best of the game.

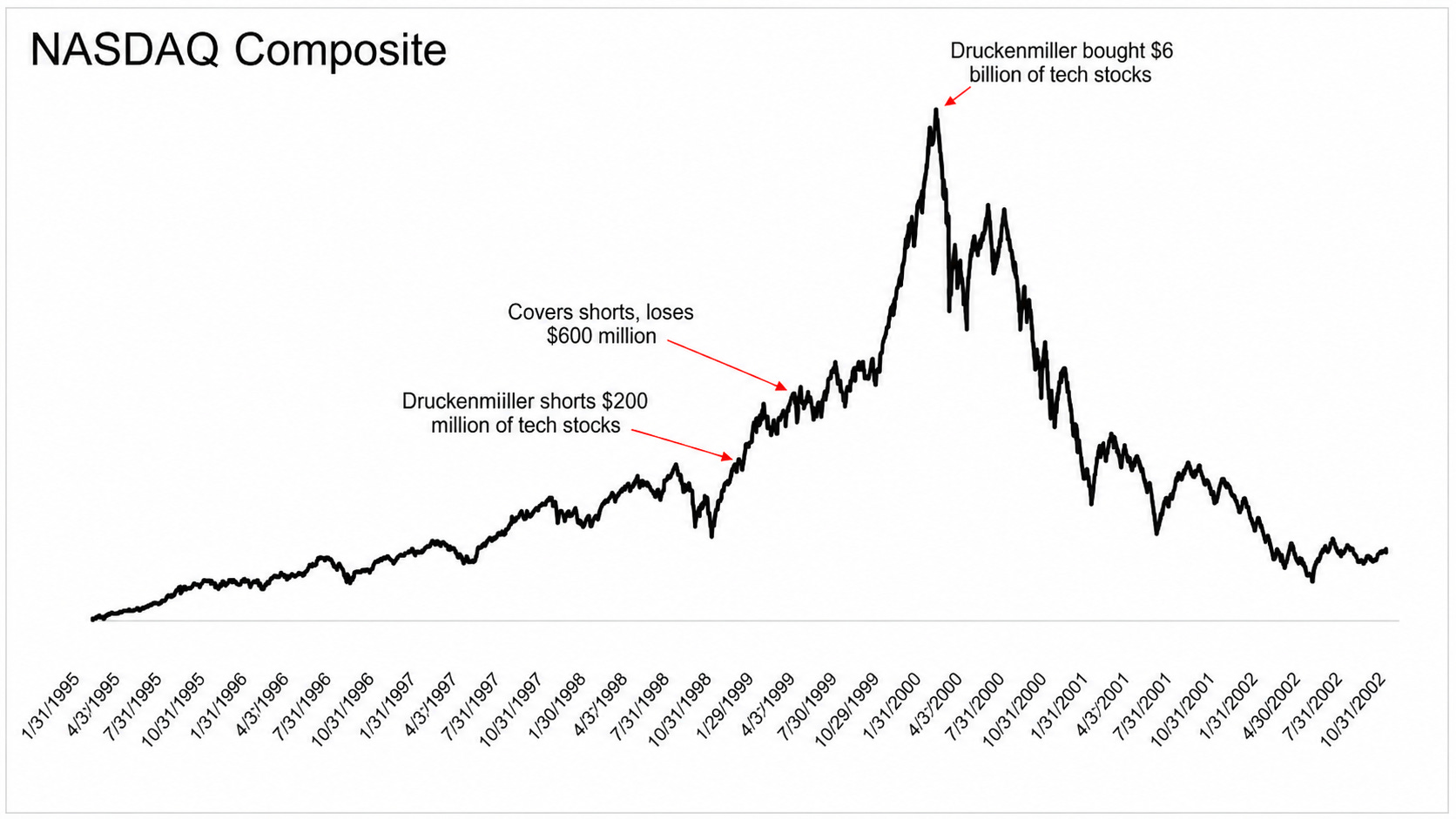

Druckenmiller shorted $200 million in internet stocks in 1999, expecting the bubble to burst. The market kept rising, he got FOMO, and covered his shorts with a $600 million loss. He then went long, buying $6 billion of tech stocks. The bubble burst, and he lost $3 billion on his overall tech exposure.

When asked what he learnt, he said—“I didn’t learn anything. I already knew that I wasn’t supposed to do that. I was just an emotional basket case and couldn’t help myself.”

Nobody is immune.

In an environment where getting carried away is so easy, we have to consistently remind ourselves that almost nobody made a fortune trading dotcom stocks in the 2000s, only the shameless pumpers.

Look at all the great investors, Buffett, Munger, Lynch, etc. You can’t find a single one who made money playing the speculation game we are seeing in the markets today.

For long-term wealth creation, the recipe is simple—buy quality and never overpay.

But.. Are there still high-quality businesses with solid growth prospects and attractive valuations left in the current market environment?

The answer is an emphatic “yes.”

Fortunately, people’s clustering in the sexy industries and hype zones leaves the boring corners of the market ignored, creating opportunities for those willing to look.

I have just found such an opportunity:

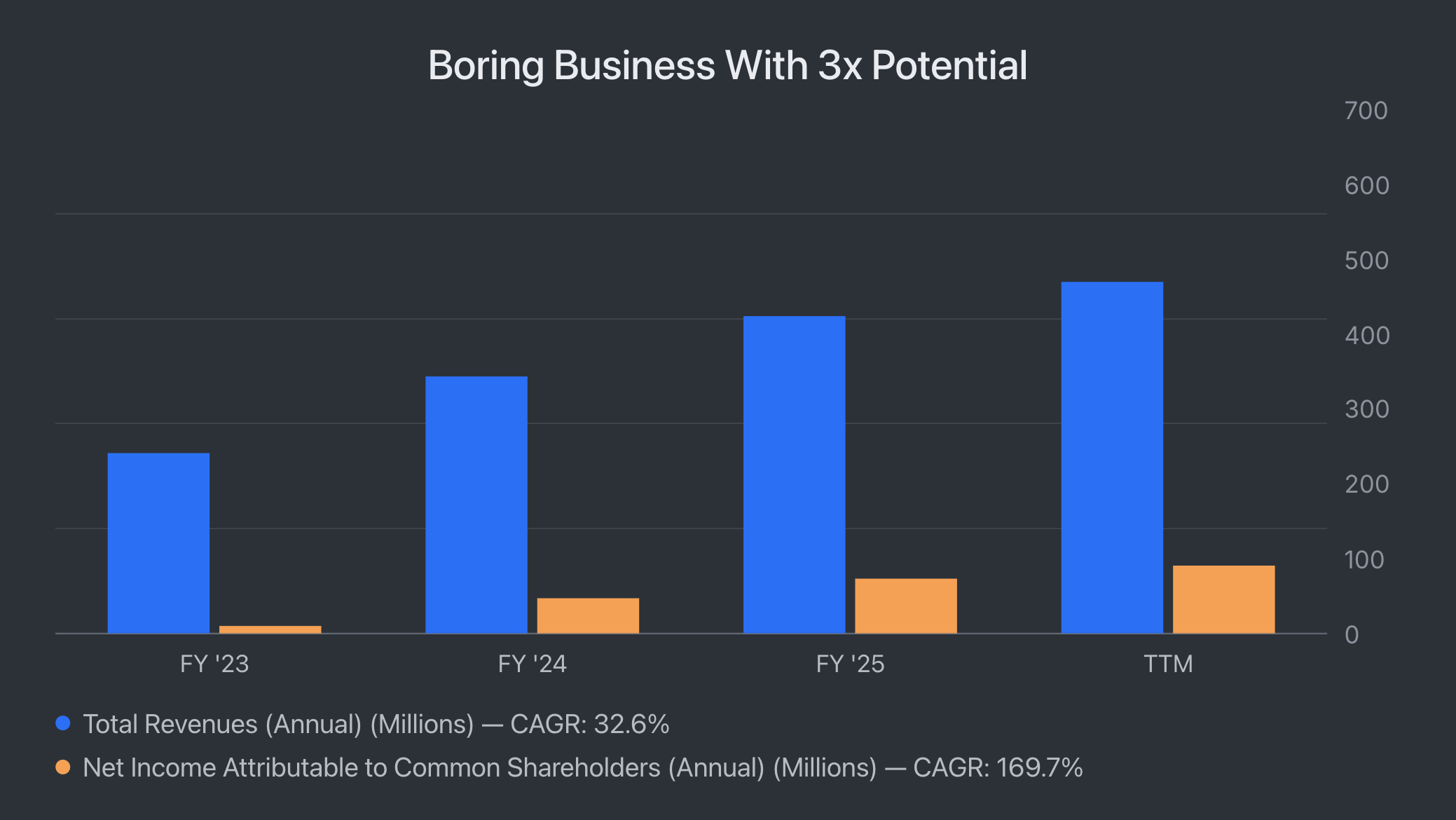

Revenues grew by 32% annually since 2023.

Net income has almost doubled since 2024.

Return on equity expanded from 14% in 2024 to 18% now.

What’s even better is that the stock is trading at just 10x this year’s earnings, and the management is aggressively buying back shares.

It’s a rare, mispriced opportunity in this market. I have been following the company for a while and recently decided to pull the trigger after their latest earnings print came even better than I expected.

It will be a multi-bagger over the next few years, even if it can hit conservative growth targets.

So, let’s cut the introduction here and dive deeper into this gem.

🏭 Understanding The Business

The more niche you get in the market, the more inefficiency you’ll find. This has always been a well-known fact among investors.

If you are managing a small sum, go niche, overlooked corners of the market. You’ll see more inefficiency because the companies in these spaces generally lack broad analyst coverage and are too small for institutions to be interested.

The same principle applies in business as well.

The more niche you go, the more supply gaps you’ll find. Given that these gaps will be relatively small, you can create a defendable business if the product is sticky, as it’ll keep the contestable portion of the market small enough to make the entry unfeasible for potential competitors.