10 Lessons From 2024 Berkshire Hathaway Annual Shareholder Meeting

10 Lessons From 2024 Berkshire Hathaway Annual Shareholder Meeting

It was the first one without Charlie. His wit and wisdom were largely sought after, though, this meeting didn't come short in terms of lessons about life and investing.

“Over time, we worked together to achieve his vision. Charlie, in effect, became the architect of today’s Berkshire.”

-Warren Buffett, 2024 Berkshire Hathaway Annual Meeting Movie

Charlie Munger was perhaps among one of the broadest philosophers in our age. At first he was only known to the small crowd attending Berkshire Hathaway Shareholder Meetings. However, over time, his wit and wisdom attracted fans from entrepreneurship, philosophy, math & sciences, sports, entertainment and every other area you can think of.

Buffett, describes this phenomenon as “he was more broader than me, he never stopped wanting to learn more.”

Berkshire Hathaway’s 2024 Annual Meeting was pervaded by the sadness for loss of this great man.

Annual Shareholder Meeting Movie is normally dominated by Buffett’s advice and advertisements of products of Berkshire subsidiaries. This time, it was different. The movie was completely devoted to Charlie Munger and it got a standing ovation from the crowd. If you haven’t seen it yet, just click the link below 👇

Berkshire Hathaway Annual Shareholder Meeting Movie

As per the Berkshire Annual Meeting Movie, this issue would normally be about recent earnings reports of the companies that I follow closely: SOFI, Starbucks, PayPal, Amazon and Apple. However, I didn’t want to skip Buffett’s best advice from the meeting. You will still get earnings reviews within the next week.

In this issue, you will read:

Why has Berkshire trimmed its Apple position?

How would he invest small sums of money?

Buffett’s views on share repurchases

Buffett’s view on capital allocation

Berkshire’s foreign investments

Buffett’s advice on job picking

And much more…

Let’s cut the BS and get started!

1. Why Did Berkshire Trimmed Its Apple Position?

This was the headline of the day because Buffett trimmed Berkshire’s Apple position by a significant 13%.

Its Apple position is now worth around $135 billion, implying that Buffett sold around 790 million shares.

When explicitly asked, he said that it was for tax reasons and Apple will continue to be Berkshire’s core holding unless something drastic comes up.

Everybody took this answer for granted initially but when you think about that it doesn’t make that much sense.

Why?

Because you are selling an asset that has significant appreciation potential while you have a massive $189 billion cash pile by which you can pay the taxes and you wouldn’t lose an asset with appreciation potential.

But he chose to sell some Apple.

Between the lines, he hinted that he doesn’t have any concerns about Apple’s earnings potential but the valuation is now too high that he thought it made sense to take some profits, pay taxes and grow the cash position.

Indeed, when you think about it Apple was a $500 billion company in 2016, when Buffett first bought Apple, and it was trading at 11 P/E. Now, it’s nearly a $3 trillion company and trades at 27 P/E.

He just thought that the current valuation warrants some profit taking but I am also sure that he wouldn’t hesitate to buy even more Apple if the stock market crashes tomorrow.

2. Right Way to Look at Share Buybacks

If Berkshire is known for one thing, it’s that the Company doesn’t pay any dividends to the shareholders.

The reasoning behind it is simple: Buffett thinks that a business should pay dividends only if it can’t make good use of the excess capital it has.

What does this mean? What is a good use of capital?

For Buffett, this means Return on Equity.

Buffett thinks if the company is able to allocate capital better than shareholders themselves and provide them with above average returns, it should retain the earnings and allocate capital itself.

For individuals, the benchmark here is annualized S&P 500 historical return, which is around 10%. Buffett’s track record of 20% annualized return for over 55 years nearly doubles this. Thus, it only makes sense that Buffett prefers to allocate capital himself rather than the shareholders.

For American companies, average Return on Equity is around 12%, above this number is considered exceptionally good. Between 2019 and 2023, Berkshire scored 13% annualized ROE. However, if you go back to the first days when Buffett acquired Berkshire, it delivered way more than 13%.

You have two very good arguments to retain capital and not pay dividends: Buffett invests better than shareholders and Berkshire allocates capital better than most American companies.

This makes it look like it’s very plausible for Berkshire to buyback its own shares.

After all, it would be buying shares of a company that delivered above average returns on equity.

This was asked to Buffett and his answer was kind of surprising to me.

He said “Berkshire can’t exercise aggressive stock buybacks because class A shareholders are rarely willing to sell.”

When you think about it, this sentence totally reflects Buffett’s views on buybacks.

He thinks that buybacks should not be considered differently from other common stock investments and thus they should be price dependent.

He previously touched upon this in 2020 Annual Shareholder Meeting

He thinks that buybacks only make sense at the right price and buying back shares just to support stock price is not the best action to take for shareholders.

This once again illustrates his fundamental thinking on investment: All investment decisions should be price dependent.

This is the long standing teaching of Benjamin Graham.

“What you pay determines your rate of return.”

-Benjamin Graham

He simply is not willing to pay more than it deserves even for his own company.

This is simply not just a lesson on buybacks, but it eloquently articulates how you should approach all investment decisions.

3. How Would He Invest Small Sums of Money?

In the 1999 Berkshire Annual Meeting, Buffett indicated that he would be able to achieve around 50% annual return if he was managing a smaller amount of money around $1 million.

This question came up in this meeting again, though, in a different way.

This time, Buffett was reminded of this view and asked what method he would use to achieve this, Cigar Butt investing or buying exceptional companies at fair prices?

He said “both.”

Though this can be taken as a simple answer, I think it’s again deeper than it seems and it shows how disciplined Buffett is when it comes to investing.

Certainly, one could think that buying exceptional companies at fair prices doesn’t make sense if you want to achieve around 50% annual return with a small sum of money.

However, when you think more, you see that this isn’t right.

Last year, you could buy Amazon for $90 per share, Apple for $140, Google for $90, Microsoft for $255 and a portfolio of those companies would be up between 50%-100% depending on your allocation.

At the time of market crashes or economic downturns, you don’t need to specifically look for cigar butts or other special situations like liquidations or mergers to achieve exceptional returns. You may find exceptional companies trading at ridiculously cheap prices and that would be your opportunity.

On other days, you will find those companies fairly priced or overvalued and you would have to look for cigar butts and special situations while holding onto your positions in those exceptional companies.

As Benjamin Graham established and Buffett followed vigorously, investment operations should be price dependent.

Never forget this.

4. Views on Capital Allocation

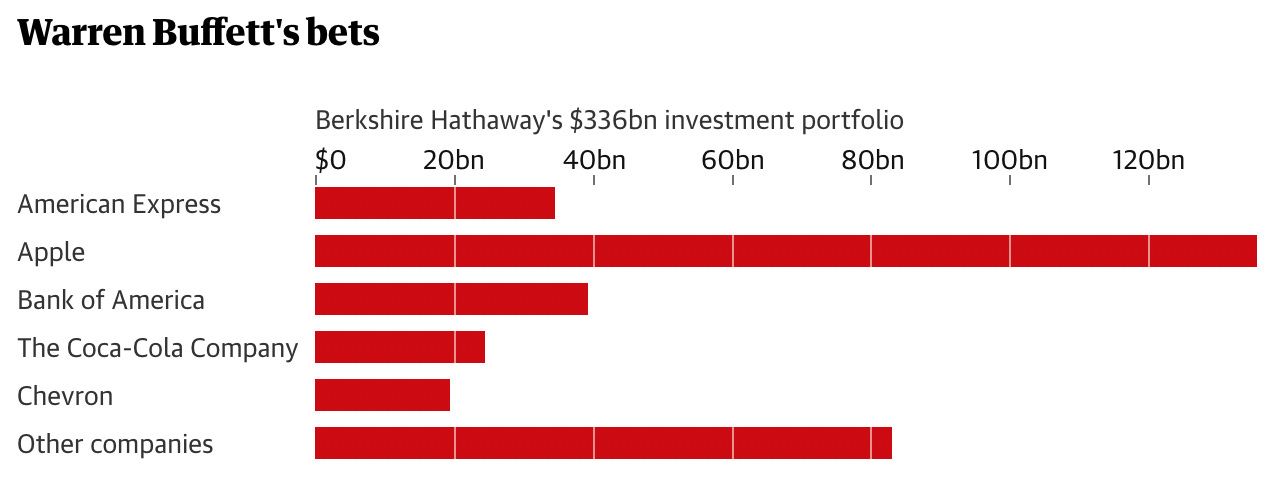

Today Berkshire’s stock portfolio is roughly worth $336 billion.

If it were a separate company, it would take over Costco as the 27th largest company in the world.

Managing this portfolio is of utmost importance for Berkshire and its shareholders. It’s a very important matter who will manage this portfolio in the post-Buffett era.

I should say I am surprised here.

I expected that Ted Weschler and Tod Combs would be managing Berkshire’s portfolio.

But Buffett said that he thinks that capital allocation is a non-divisible job that should belong to the CEO in its entirety.

I am 100% sure that Greg Abel is an excellent manager and director but we don’t have much knowledge on his investing skills.

Greg understands business extremely well, and if you understand businesses, you understand common stocks.

-Warren Buffett

This was how he addressed those concerns.

He indicated that Greg Abel will surely get help from others and from the junior money managers of Berkshire, but when it comes to the decision making, he will have the final say.

What’s the lesson we can draw from this?

Every stock has a company behind it.

You should analyze companies, not stocks and decide whether you would be willing to buy the whole company if you had enough money. If the answer is “yes” only then you should look at the price and make a price dependent decision.

Study picking businesses, not stocks.

5. Investing in Foreign Countries

“Never bet against America.”

Buffett previously emphasized this position in the 2020 Berkshire Annual Meeting and 2021 Shareholder Letter.

He reaffirmed this in this meeting.

He was asked two questions, one about whether he will be investing in China again and the other about whether Berkshire will pursue opportunities in the fast-growing Indian economy.

He didn’t exclude those possibilities but he maintained his firm belief in America.

He said “If we are to make something really big in the future, that will most likely be in America.”

He emphasized that America has been a great country for building wealth and capitalist democracy is the best system of governance ever invented.

With all its flows, America is the best implementation of this system and there is no reason that this will change in the near future.

Beyond America’s individual properties, he also mentioned that he doesn’t know the business environment in other countries as well as he knows it in America. This is why he feels better operating in America rather than any other country in the world.

All investors should indeed know the business environment and also the political environment in countries they are thinking about to invest in. I know the fast-growing India market looks very appealing right now and it’s fine if you have an edge in India.

But if you don’t have this edge, I wouldn’t invest in Indian companies just after analyzing them on paper.

If you are so afraid to miss it, buy the index, don’t bet on individual stocks, even Buffett doesn’t do that.

6. Advice on Job Picking

This is one of his best pieces of advice from the meeting:

“Find the job that you would like to have if you did not need a job.”

-Warren Buffett

It only makes sense.

Buffett previously emphasized that he tiptoes to the work everyday and this is only apparent as he keeps working at the age of 93.

He doesn’t just advise this, he also practiced this.

After he graduated from the Columbia Business School, he asked to work for his former teacher Ben Graham.

Graham said no.

Buffett didn’t give up and he offered to work for free. Even then Graham said no but Buffett didn’t give up and finally got a job in Graham’s firm.

This is what you should be looking for.

It’s not just Buffett who thinks this way. Remember Steve Jobs’ famous words in the Stanford Commencement speech he gave before his death: “Keep looking, don’t settle!”

7. On the Importance of Culture

Greg Abel and Ajit Jain are amazing managers and operators, they are truly exceptional in nearly all angels, we don’t have any concern about their ability to steer Berkshire in the post-Buffett era.

However, a shareholder brought up an important question: It was Buffett and Munger who attracted Greg and Ajit to Berkshire. Will the company be able to attract that kind of talent in the post-Buffett era?

Buffett said that in Berkshire culture shareholders are seen as partners and managers feel themselves as the owners of the businesses they manage. Greg Abel will keep the culture alive in the post-Buffett period and this will automatically attract top talent as managers will be attracted to a place where they are given full responsibility and trust.

As this culture stays alive, Berkshire will be able to attract top talent.

Greg Abel also emphasized on culture. He said that “nobody is replaceable” and gave Tim Cook as an example. He said Cook has done an amazing job in the post-Jobs era and turned Apple into the most valuable company in the world.

8. When to Sell Stocks?

This is a question on which I wrote a long issue on this newsletter. If you haven’t read that yet, you can find it here 👇

Buffett articulated that there may be many reasons to sell stocks and the first one is that if you need money. However, for Berkshire, it doesn’t happen anymore. Thus, he gave two more reasons to sell stocks:

Even a bigger opportunity comes up

Something drastically changes in the business

You can see these principles at play in Buffett’s investing history.

In 2018, Buffett fully exited from IBM in order to create a larger position in Apple.

This is an example of the first situation.

Further, in 2020, Berkshire sold all its 30 local newspapers, a branch of business once favored heavily by Buffett.

He sold these newspapers because he saw that the business economics of newspapers were changing, everything going online and print press weren’t much profitable anymore.

This is an example of the second situation.

Overall, you may sell stocks in three situations:

You need to raise money

There is even a bigger opportunity

Business economics deteriorate drastically

These are the fundamentals of selling stocks.

9. Effects of Consumer Behavior on Investment Decisions

Buffett thinks that two types of businesses have durable competitive advantage: 1) Lowest cost suppliers of products and services, 2) suppliers of unique products and services.

He wants to own these businesses and own them for a very long time.

Why?

Because those businesses are monopolies in what they sell.

If you want to drink Coca-Cola, you want to buy it from Coca-Cola. If you want to use an iPhone, you have to buy it from Apple. They are monopolies in what they sell.

If this kind of business achieves to create a high level of consumer loyalty, it will make so much money.

Buffett says that he decided to buy Apple stock when he notices Apple’s consumer loyalty:

“If people have both an iPhone and a car and you ask them which one they would choose: Not to have a second car in your life or a second iPhone, they would give up the second car.”

-Warren Buffett

When a business enjoys this level of consumer loyalty, it’s really hard for competition to erode its moat and eat away its profit margin.

Thus, such a company, at a fair price, most likely makes an exceptional investment.

10. How to Live a Good Life?

I think this was the most striking piece of advice from Buffett.

Years ago, Buffett asked for advice about how he should live his life.

Munger told him “You should write your obituary the way you want it written, and then live your life accordingly.”

Buffett cited this amazing piece of advice Munger gave him earlier and repeated it.

To be honest, this is the best piece of advice I have ever heard in life.

I will remember this as I live my days. I hope you will remember it too.

Conclusion

These were the top 10 lessons from Berkshire Hathaway’s 2024 Annual Shareholder Meeting.

I will try to remember these lessons in investing and in life, I hope you do too.

We are lucky to be able to hear those from arguably the greatest master of investing ever lived.

I will write an earnings review for the stocks I closely watch within this week.

Have a good Sunday!

Great post! I like the part that said that he will never bet against America…that means a lot! And his advice for how to live a good life too! Priceless!

Wonderful summary with integration of life advice, and Buffett’s investment advice is timeless for all.